In the intricate world of construction and contracting, the margin for error is slim, and the consequences of mistakes can be costly.

Contractors Errors & Omissions (E&O) Insurance emerges as the unsung hero, safeguarding professionals from the financial devastation that may follow professional liability claims. This blog post delves into the essentials of E&O Insurance, demystifying what it is, its critical importance, and how it provides a safety net for those in the crosshairs of negligence allegations.

Understanding Contractors Errors & Omissions Insurance

Contractors Errors & Omissions (E&O) Insurance, also known as Professional Liability Insurance, is a specialized form of coverage that addresses the unique risks associated with the professional services provided by businesses, including contractors.

This insurance protects against claims of negligence, mistakes, or failures to perform that can lead to financial loss for a client. Unlike general liability insurance, which covers bodily injury and property damage, E&O insurance focuses on financial losses that may arise from professional advice or services.

There are common misconceptions about E&O coverage, such as the belief that general business liability insurance is sufficient or that small errors will not lead to significant claims. However, even minor oversights can result in costly lawsuits, emphasizing the need for dedicated E&O protection.

Understanding the distinct benefits of this coverage is crucial for contractors to safeguard their business against the financial repercussions of professional liability claims.

The Importance of E&O Insurance for Contractors

E&O Insurance is essential for contractors as it serves as a safeguard against negligence claims that can arise from errors or omissions in their work. Without this coverage, contractors may be financially responsible for costly legal defense fees and potential damages awarded in a lawsuit. The financial burden of such claims can be significant, potentially threatening the viability of a contractor’s business.

Beyond the direct financial impact, E&O insurance also plays a crucial role in building client trust and meeting contractual requirements. Clients are increasingly aware of the risks inherent in construction projects and may mandate that contractors carry adequate E&O coverage before entering into agreements.

Having this insurance not only demonstrates a contractor’s commitment to professional accountability but also ensures compliance with industry standards and client expectations.

Identifying Professional Liability Risks for Contractors

Running a business comes with its fair share of risks, but contractors face additional threats due to the nature of their work. The potential for professional liability claims is a significant risk that contractors must address to protect their business and reputation.

Real-world examples of professional liability claims in construction often highlight the costly consequences of oversight or professional negligence. For instance, a contractor might face a claim for the incorrect installation of a roofing system that leads to water damage, or an architect could be sued for a design flaw that compromises the structural integrity of a building. Likewise, a contractor may face a claim for failing to complete a project according to the specified timeline, resulting in financial losses for the client.

Torian Insurance has a history of assisting contractors through the complexities of E&O claims. An example includes a case where a subcontractor’s faulty installation led to property damage and significant delays in the overall project.

Risk factors unique to the construction industry, including the use of advanced technologies, adherence to tight schedules, and coordination among various trades, further compound the potential for errors and omissions, underscoring the importance of adequate E&O coverage.

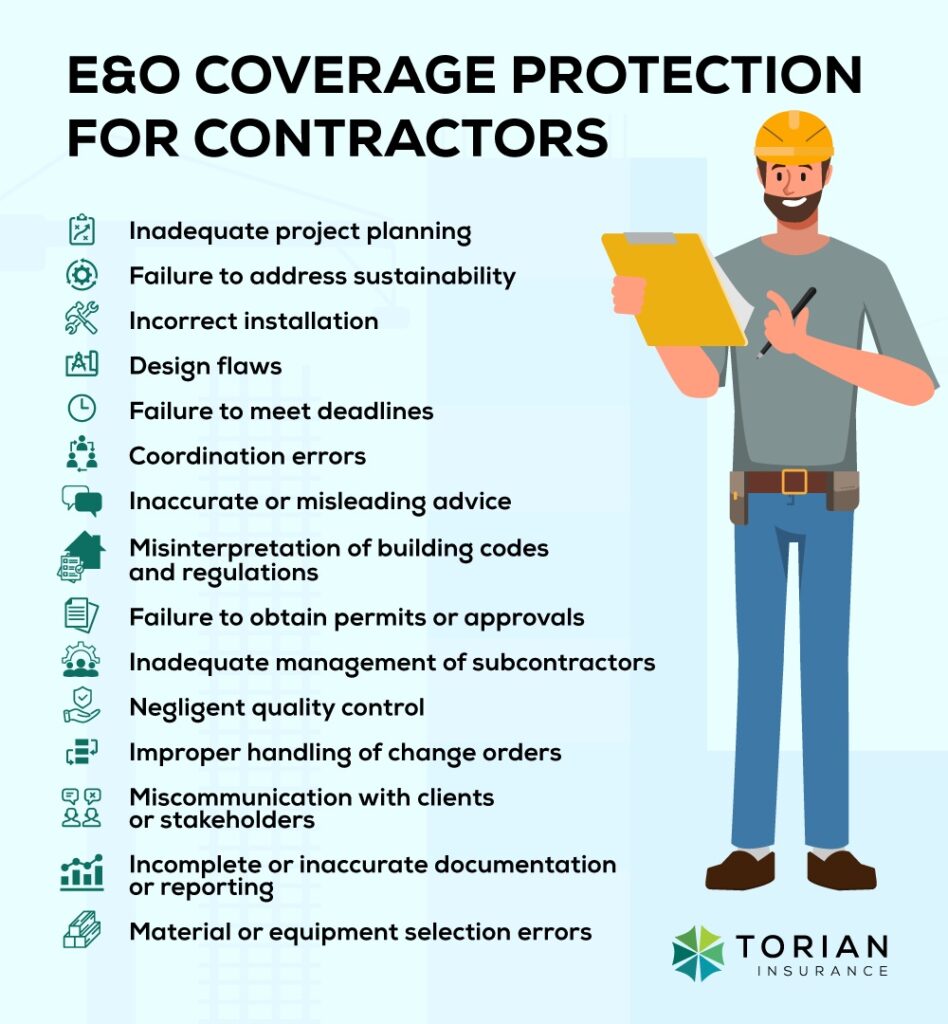

Here are some examples of the types of claims that E&O coverage is built to protect contractors from:

- Inadequate project planning or oversight leading to cost overruns and financial disputes with clients

- Failure to address environmental or sustainability considerations resulting in potential legal and reputational risks

- Incorrect installation of building systems leading to damage

- Design flaws compromising structural integrity

- Failure to meet construction deadlines resulting in financial loss for clients

- Coordination errors among various trades causing project delays or defects

- Inaccurate or misleading professional advice leading to client dissatisfaction or financial losses

- Misinterpretation of building codes and regulations leading to non-compliance issues

- Failure to obtain necessary permits or approvals leading to project delays or legal issues

- Inadequate supervision or management of subcontractors leading to errors or safety hazards

- Negligent oversight of quality control leading to subpar workmanship and potential defects in the finished project

- Improper handling of change orders leading to disputes and financial losses

- Miscommunication with clients or other stakeholders resulting in misunderstandings or disputes

- Incomplete or inaccurate documentation or reporting leading to disputes or legal claims

- Material or equipment selection errors leading to project delays or defects

By understanding the array of professional liability claims that can arise, contractors can better understand the types of situations that may lead to legal action and the financial consequences that can ensue. These examples further underscore the importance of a comprehensive E&O insurance policy to protect against potential professional liability risks.

4 Important Components of Professional Liability Insurance Policy

Professional liability insurance policies for contractors may vary in their specifics, but there are common components that are crucial to understand. These include coverage limits, policy exclusions, and maintaining coverage. Each of these components plays a key role in ensuring that contractors have robust coverage that aligns with their unique business risks.

1. Coverage Limits

Coverage limits within a professional liability policy dictate the maximum amount an insurance company will pay out on claims. For contractors, understanding these limits is crucial; they should align with the size and scope of their projects to ensure adequate protection. A policy with insufficient coverage can leave a contractor financially vulnerable, while excessive coverage may lead to unnecessary premiums.

2. Policy Exclusions

Policy exclusions are equally important for contractors to comprehend. These detail specific scenarios and circumstances that the policy does not cover, requiring contractors to carefully review their policies to avoid potential surprise claims.

By being aware of these exclusions, contractors can identify potential gaps in their coverage and take steps to mitigate those risks, possibly through additional insurance products or practices.

3. Deductibles

Deductibles are an essential aspect of professional liability insurance policies for contractors. A deductible represents the portion of a claim that the insured party must pay before the insurance coverage kicks in. For example, if a contractor has a $5,000 deductible and a covered claim amounts to $20,000, the contractor would be responsible for paying the first $5,000, and the insurance would cover the remaining $15,000.

Understanding deductibles is crucial for contractors as they directly impact the cost of insurance and the financial burden in the event of a claim. Higher deductibles typically result in lower insurance premiums, but they also mean that the contractor would bear a greater share of the initial costs in the event of a claim.

Contractors should carefully evaluate their financial situation and risk tolerance when selecting a deductible amount. It’s important to strike a balance between managing insurance costs and ensuring that the deductible amount is manageable in the event of a claim. Additionally, contractors should review their deductible amounts periodically to ensure that they align with their evolving business needs and financial capabilities.

4. Continuous Coverage

Professional liability insurance for contractors operates on a claims-made basis, which means the policy must be active both when the alleged incident occurs and when the claim is filed. This aspect of E&O policies underlines the importance of maintaining continuous coverage and understanding the policy’s retroactive date, if applicable, as claims related to services performed before this date are typically not covered.

Before purchasing Errors & Omissions (E&O) Insurance, contractors should engage in thorough questioning to ensure they understand exactly what their policy will cover. It is crucial to ask about the specific scenarios and risks that the policy addresses. Working with the right insurance provider will help to ensure the policy’s terms align with the business operations and history.

Seeking a Trusted Insurance Partner for Your Business? Click Here

Torian Insurance has a commitment to personalized service and tailored coverage. Learn more about our insurance offerings for contractors.

Tailoring Errors & Omissions Insurance Coverage to Your Specific Needs

Customizing policies for different contractor specialties is essential because each trade comes with its own set of risks and potential liabilities.

An electrician might need coverage for damages arising from improper wiring, while a plumber might require protection against claims of water damage due to faulty piping. By identifying the unique aspects of their work, contractors can ensure they have the appropriate protection.

Evaluating additional endorsements or riders is another step towards comprehensive coverage. These can provide protection for scenarios that might not be covered under a standard policy. For instance, a design-build contractor may benefit from an endorsement covering design errors, while a general contractor might need a rider for subcontractor acts.

The role of a professional insurance advisor is crucial in assessing coverage needs. An experienced advisor will review a contractor’s specific services, project types, and client agreements to recommend tailored coverage options. This personalized approach helps in mitigating risks specific to a contractor’s business and ensures that they are neither underinsured nor paying for unnecessary coverage.

With Torian Insurance, contractors receive more than a policy—they gain a partner committed to their long-term success and risk management.

Why Evansville, Indiana Tri-State Area Contractors Should Consider Torian Insurance for E&O Coverage

Gain Peace of Mind with Secure Coverage Today

As we’ve navigated the complexities of errors & omissions insurance together, it’s clear that the right protection is not just a safety net—it’s a cornerstone of a trustworthy and sustainable contracting business.

Whether you’re mitigating risks or seeking peace of mind in your professional endeavors, customizing your E&O coverage to fit your unique needs is crucial. Understanding these policy components helps in determining the suitability of the insurance for the contractor’s unique business risks.

At Torian Insurance, we understand the intricacies of the construction industry and are dedicated to equipping you with a tailored insurance portfolio. Our team is committed to guiding you through each step, from initial consultation to policy customization, ensuring that you are protected against the unforeseen.

Now is the time to take the next step. Secure your legacy and fortify your business with Contractors E&O Insurance that’s as precise and reliable as the work you do. Let’s start this important conversation, because your peace of mind is our priority.

Reach out to Torian Insurance today and let us help you build a foundation of protection that stands as strong as your own craftsmanship.