Embarking on a plumbing project often involves more than just wrenches and pipes; it’s a complex operation fraught with potential risks that can spring a leak in your business’s financial stability.

For plumbing professionals in the tri-state area of Indiana, Illinois, and Kentucky, understanding these risks and securing the right plumbing insurance coverage is as crucial as fitting the last piece of a pipeline. This blog post will dive into the depths of insurance for plumbers, highlighting how Torian Insurance offers personalized protection plans to shield your business from the unexpected. We will navigate through the essential insurance policies that every plumbing business should consider and the benefits of tailoring coverage to meet specific industry demands. So, whether you’re laying down new pipes or repairing old ones, let’s ensure your business foundation is as secure as the services you provide.

What Is Plumbing Insurance?

Plumbers’ insurance encompasses a range of insurance coverages tailored to address the unique risks faced by professionals in the plumbing industry.

This specialized insurance package provides protection against potential issues such as lawsuits, theft or damage to tools, business interruptions, and workplace injuries or illnesses. For instance, if a plumber inadvertently damages a customer’s property during a service call, the general liability component of their plumbing insurance can cover the costs of repairs, helping to mitigate financial liabilities and ensure continued business operations.

While all plumbing insurance policies vary they typically cover: Accidental injuries

- Property damage

- Employee wages after a work-related injury

- Vehicles and equipment

- Unintentional faulty workmanship

- Legal fees

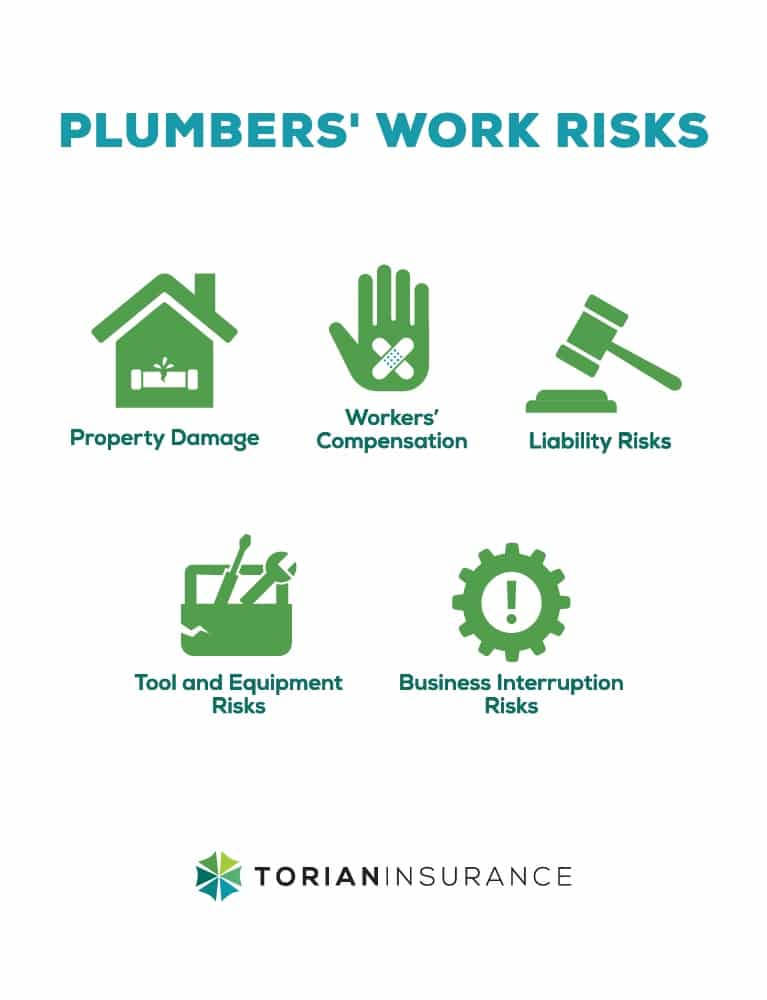

Understanding the Risks Involved in Plumbing Work

Plumbers confront a myriad of risks daily, and having the right insurance plays a pivotal role in mitigating these risks and safeguarding their financial stability. Crucial categories of risks that plumbers regularly face include:

1.) Property Damage: Plumbers work in diverse environments and can inadvertently cause property damage. A minor oversight like a loose pipe fitting causing water leakage can escalate into significant water damage for the property holder. If determined to be the fault of the plumber, such mishaps can lead to sizable financial liabilities.

2.) Bodily Injury: Bodily injury liability insurance is crucial for plumbers and plumbing companies, as accidents can happen in this line of work. This type of insurance protects the business in case a customer or third party is injured on the premises or as a result of the plumbing services. Without bodily injury liability coverage, the business could face significant financial consequences from legal fees, medical bills, and potential lawsuits.

3.) Liability Risks: Legally, plumbers are accountable for the work they do. Any faults or insufficient work can result in legal liabilities. Potential lawsuits from disgruntled clients alleging damages or negligence can lead to expensive legal processes. Without the appropriate liability insurance, the resulting legal and compensation costs could jeopardize a plumbing business’s financial stability.

4.) Tool and Equipment Risks: As heavily tool-reliant professionals, plumbers face the risk of tool and equipment damage, theft, or loss. A specialized insurance coverage protection can help cover the costs of replacing these essential items.

5.) Business Interruption Risks: Unforeseen circumstances like natural disasters or a sudden loss of key staff can disrupt business operations, leading to loss of income. Business interruption insurance is vital to offset these financial impacts.

These potential risks highlight the importance of comprehensive insurance coverage, providing an essential safety net to protect plumbers and their businesses from unexpected financial losses.

Plumbing Insurance Claim Examples

While nobody likes to think of themselves being victim to a lawsuit, claims happen more frequently than some like to think. These are some real-life examples of scenarios a plumber may face.

- A plumbing contractor was hired to fix a leaking shower head in a two-storey family home. After completing the repair, everything seemed in order. Several days passed, and the owner noticed a large water stain on the living room ceiling right under the bathroom. Investigating, it turned out the plumber had accidentally punctured a tiny hole in a pipe behind the shower wall. Repair costs for the pipe and extensive water damage rose to over $50,000.

- A plumber was installing a new water heater in a home and didn’t follow the manufacturer’s ventilation instructions. This led to a slow, undetected carbon monoxide leak. The family experienced symptoms of carbon monoxide poisoning and had to be hospitalized. The homeowner sued the plumber for hospital bills, pain, and suffering due to negligence, with costs going beyond $100,000.

- Once, a plumbing business hired subcontractors to assist in a large-scale remodeling project. One subcontractor neglected to sufficiently tighten a pipe connection, leading to a gas leak. The subsequent explosion resulted in severe injuries and significant property damage. The claim against the plumbing business totaled almost a million dollars.

- A plumber was called in to perform routine maintenance on a commercial building’s sewage system. During the procedure, the plumber mistakenly damaged a water main, causing significant flooding to the commercial space and damaging various tenants’ properties. The ensuing property damage and business interruption claims amounted to substantial expense settlements.

- During a residential plumbing installation, an apprentice failed to properly install a sump pump. During a major storm, the pump malfunctioned causing the basement to flood. Along with structural damage, the incident led to the loss of a substantial amount of valuable personal property stored in the basement, resulting in a hefty claim against the plumbing contractor.

These examples underline the importance of comprehensive insurance to safeguard plumbing professionals against possible setbacks and financial risks.

Who Needs Plumbing Insurance?

Plumbers’ insurance is essential for a wide range of professionals and businesses within the plumbing industry. Individuals and companies that may benefit from plumbing insurance include:

- Drainage system installers

- Piping and plumbing contractors and owners

- Septic system construction workers

- Sewer hookup contractors

- Sump pump installation and servicing contractors

- Water pump installation and servicing contractors

- Water system balancing and testing contractors

- Sprinkler installers

- Handypersons

In summary, any professional involved in the plumbing sector should prioritize securing plumbing insurance to protect themselves, their business and their clients.

Types of Insurance Coverage Essential for Plumbers

Plumbers face a unique set of challenges and potential liabilities that require specific types of insurance to safeguard their business.

General Liability

General liability insurance is an essential safeguard for plumbers, offering coverage against third-party claims of bodily injury and property damage. Plumbing work frequently involves a range of risks, from accidental water damage to injuries caused by tools or equipment. Without adequate protection, plumbers could face significant legal expenses in the event of a claim. General liability insurance steps in to cover defense costs and any settlements or judgments that may arise from such incidents. By investing in this insurance, plumbers can focus on their work with peace of mind, knowing that they are financially protected in case of unforeseen accidents or mistakes.

Professional Liability

Professional liability insurance, also known as errors and omissions insurance, is a vital component of a comprehensive insurance portfolio for plumbers. This coverage specifically addresses the financial repercussions of errors, omissions, or negligence that may occur during plumbing services. Given the technical nature of plumbing work, even the most skilled professionals can make mistakes that result in costly damage or malfunctions for their clients. Professional liability insurance steps in to cover the financial fallout from such situations, including legal expenses, settlements, or judgments. With this insurance in place, plumbers can safeguard their financial stability and reputation, ensuring that they can continue to deliver high-quality services without the fear of a single mistake jeopardizing their livelihood.

Workers' Compensation

Workers’ Compensation Insurance is a crucial component of a plumber’s insurance coverage, typically required by law in most states. This insurance provides vital protection for employees who may suffer injuries or illnesses while performing their duties. Plumbers face various risks in their line of work, from slips and falls to exposure to hazardous materials. In the unfortunate event of an employee getting injured on the job, workers’ compensation insurance ensures that their medical expenses are covered, including hospital bills, rehabilitation costs, and lost wages during recovery. By prioritizing the well-being of their team, plumbers can demonstrate their commitment to a safe and secure work environment while fulfilling their legal obligations as responsible employers.

Commercial Auto

Commercial auto insurance is a critical investment for plumbers who rely on vehicles to carry out their job responsibilities. Whether it’s driving to a client’s location for a service call or transporting equipment and materials to worksites, having the right insurance coverage is crucial. Commercial auto insurance goes beyond personal auto policies by providing specific protection for business-related activities. In addition to covering accidents, theft, and vehicle damage, this insurance can also protect against liabilities arising from accidents caused by the insured plumber while driving for work purposes.

Commercial Property Insurance

Commercial Property Insurance is essential for plumbing businesses to protect their physical assets, including buildings, furniture, fixtures and inventory from potential losses due to damage. Given the reliance on various assets to conduct daily operations, the risk of incidents such as fire, theft, vandalism, and natural disasters can have a substantial impact on business continuity and financial stability. By securing Commercial Property Insurance, plumbing businesses can ensure coverage for repair or replacement costs, alleviating the burden of bearing these expenses out-of-pocket and safeguarding their financial well-being.

Tools & Equipment

Tools and equipment insurance is a vital component of risk management for plumbers, protecting their specialized gear essential for daily operations. Plumbers rely heavily on a range of tools and equipment, such as pipe wrenches, drain snakes, soldering irons, and diagnostic devices, to efficiently perform their services. Given the portable nature and high value of these items, they are prone to theft, damage, or loss on job sites or while in transit. Tools and equipment insurance provides coverage for the repair, replacement, or reimbursement of these essential assets in the event of unforeseen incidents, ensuring that plumbers can continue their work smoothly without the financial burden of replacing costly tools out-of-pocket.

Business Interruption Insurance

Another form of protection for plumbers is Business Interruption Insurance, essential since even a single prolonged outage due to unforeseen events can severely impact cash flow and the overall profitability of a plumbing business. To avoid potential implications like bankruptcy or loss of reputation as an independent plumber, this type of insurance covers lost income during downtimes caused by damages that aren’t typically covered under standard commercial property policies.

Surety Bonds

Surety bonds, while not technically insurance, play a significant role in the plumbing industry, offering a level of financial and professional security. They function as an agreement between three parties: the plumber (the principal), the client (the obligee), and the insurance company (the surety). The bond ensures that the plumber will perform their work according to certain stipulations, providing a guarantee to the client of their work’s completion to the agreed-upon standards. If the plumber fails to meet these terms, the client can make a claim against the bond to recover any losses. For clients, a surety bond offers assurance of quality work; for plumbers, they bolster their credibility and trustworthiness in the industry.

BOP

A Business Owners Policy (BOP) is a comprehensive insurance solution for plumbers, combining various protections into a single package. It generally includes property insurance, general liability insurance, and business interruption insurance. Property insurance safeguards against damage to owned or rented buildings, as well as equipment and tools used for the business. General liability insurance provides coverage for claims arising from bodily injuries, property damage, or reputational harm. On the other hand, business interruption insurance offers financial assistance to counter revenue losses during unexpected business discontinuity caused by events like fire or natural disasters. A BOP offers plumbers a streamlined, convenient way to manage multiple insurance needs, mitigating risks associated with their trade effectively and efficiently.

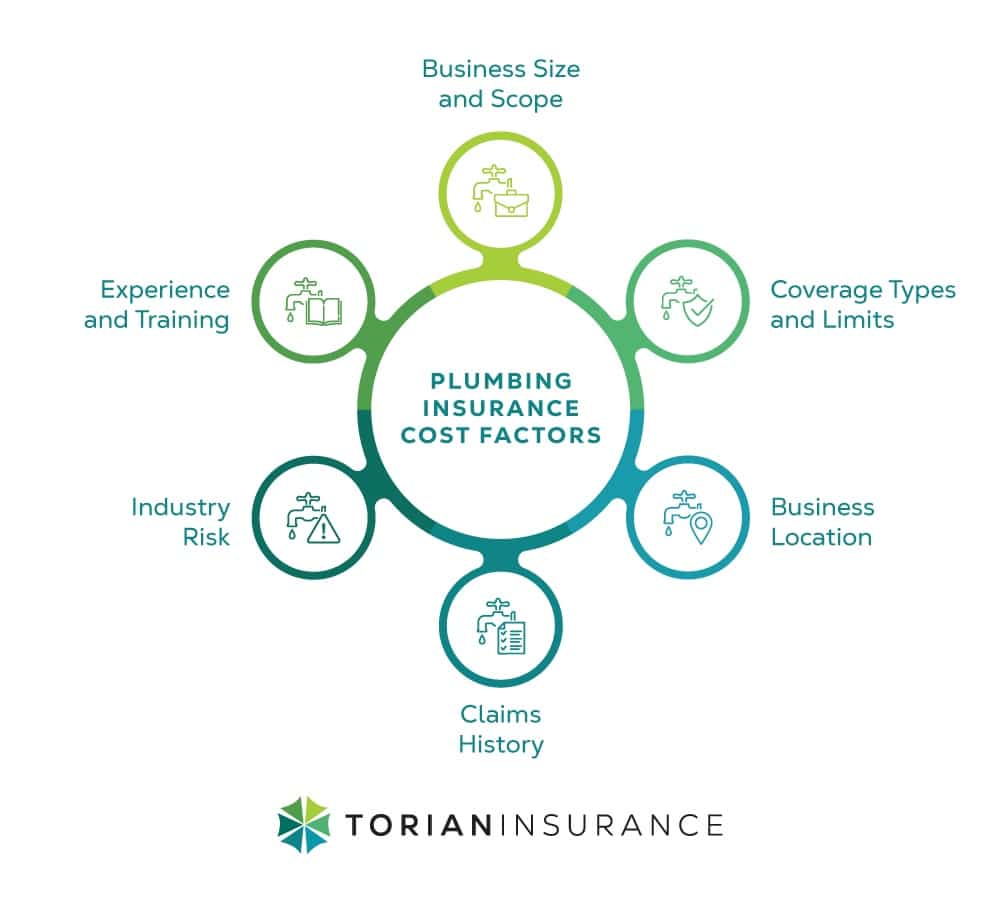

What does Plumbing Insurance Cost?

The cost of plumber’s insurance can vary greatly depending on several factors. Here are some of the key elements that insurance providers commonly consider when setting premiums:

- Business Size and Scope: Larger businesses with more employees, bigger project sizes, and more equipment are usually more expensive to insure due to the increased risk. Smaller, local operations can generally expect lower premiums due to fewer risk exposures.

- Coverage Types and Limits: The cost of your premium will also depend on the specific coverage types and limits you choose. More comprehensive policies that provide a higher level of financial protection will come at a higher cost.

- Business Location: Insurance rates can differ depending on the geographic location of the business. If your operation is located in an area prone to natural disasters, high crime rates or other potential risks your premium might be higher.

- Claims History: Businesses with a clean claims history are often rewarded with lower premiums, while a history of many claims can result in higher costs.

- Industry Risk: The inherent risks associated with the plumbing profession—such as potential property damage, bodily harm, or tool theft—can influence the cost of your policy.

- Experience and Training: Experienced plumbers with extensive training may tend to make fewer claims, leading to lower premiums. High-risk, inexperienced, or untrained plumbers may increase the cost of insurance.

Remember that while cost is an important factor, it’s equally important to ensure you have the right amount of coverage to fully protect your plumbing business. It is always recommended to consult with a trusted insurance agent who can provide a detailed breakdown of costs based on your specific needs and circumstances.

What is Not Covered by Plumbing Insurance?

While plumbing insurance provides comprehensive coverage for a variety of risks that plumbers typically face, it’s important to note that not everything is covered. Here are some exclusions that are generally not covered by standard plumbing insurance:

- Intentional Damage or Misconduct: Any damage or incidents that are intentionally caused or stem from deliberate misconduct typically are not covered by plumbing insurance.

- Wear and Tear: Regular usage and natural deterioration of tools, equipment, and buildings over time—referred to as “wear and tear”—are generally not covered under a standard policy.

- Earthquakes and Floods: Most plumbing insurance policies specifically exclude coverage for damage resulting from natural disasters like earthquakes or floods. Separate, specialized insurance policies are usually needed for these types of coverage.

- War: Damage or losses occurring due to war activities, including insurrections, are usually excluded from coverage.

- Infectious Disease: Standard policies might not cover liability claims related to the spread of infectious diseases. However, some insurers offer add-on coverages or special insurance for these risks due to the COVID-19 pandemic.

- Wrongful Termination: Insurance policies for plumbers typically do not cover claims related to wrongful termination or other employment-related disputes. Such coverage is typically provided under employment practices liability insurance.

Always review your policy documents thoroughly to understand exactly what is and is not covered. The exclusions will be clearly outlined in your policy, so it is crucial to discuss any concerns or questions with your insurance provider or agent.

The Benefits of Customized Insurance Solutions for Plumbing Professionals

The flexibility offered by personalized insurance plans is a significant benefit for plumbing businesses, which may experience changes in scope, scale, or services offered. As a business evolves, its insurance coverage can be adjusted to match its current needs, ensuring that there are no gaps in protection. Moreover, plumbers can often realize cost savings by working with an insurance agency that can bundle various types of coverage, such as general liability, professional liability, and commercial auto insurance, into a single, comprehensive package, streamlining the process and potentially reducing overall insurance costs.

Why Choose an Independent Insurance Agency Like Torian Insurance

Choosing an independent insurance agency like Torian Insurance offers numerous advantages for plumbing professionals. With deep roots in the tri-state area of Indiana, Illinois, and Kentucky, Torian Insurance boasts a profound understanding of the local business landscape, ensuring that coverage recommendations are not only comprehensive but also relevant to the geographical and regulatory nuances of the region.

Opting for an independent agency means gaining access to a wide array of insurance options. Torian Insurance can meticulously compare coverage and rates from multiple insurance carriers. This broad market access is instrumental in finding the best possible protection for plumbing businesses at competitive prices. Additionally, the agency’s independent status allows for a more personalized customer experience. By building long-term relationships with clients, Torian Insurance is committed to providing continuous assessment and adjustment of coverage needs, ensuring that plumbers and their businesses remain safeguarded as they evolve.

Getting Started with the Right Insurance for Your Plumbing Business

As a plumbing professional in the tri-state area, safeguarding your livelihood with the right insurance is not just a smart choice—it’s essential. The unique risks inherent in your line of work demand a coverage strategy that’s as precise and reliable as the services you offer. With Torian Insurance by your side, you’ll have access to personalized insurance solutions crafted to cover the specific vulnerabilities of your plumbing business. Our team’s expertise and commitment to service mean we’re here to support you as your business evolves, ensuring you’re always protected.

Don’t wait for a mishap to reveal a gap in your coverage. To initiate a personalized consultation with Torian Insurance, plumbing business owners and independent plumbers can easily get in touch through phone or by contacting us online. Plumbing professionals are encouraged to request a quote or further information, ensuring that they receive tailored advice and solutions designed to fully protect their plumbing business against the unique risks it faces.