What Does Workers’ Compensation Cover?

Workers’ compensation covers an employee for a large part of the normal costs of being injured or becoming ill at work. Generally, it pays fully for doctor’s bills and only partially for missed wages. This is because the law is a compromise between the employer’s and employee’s interests.

For a worker to be covered, you must have an active workers’ comp policy. The injured must be an employee of your business who is eligible for worker’s comp, and they must get injured at work or become ill because of conditions at work. Additionally, claims must be filed ahead of all state deadlines.

Workers’ Compensation Benefits

Workers’ compensation insurance covers a wide range of benefits for an injured or ill employee. The insurance company will examine the report you and the employee file to determine which benefits best fit the situation.

-

- Medical coverage includes both emergency and long-term medical costs of treatment.

-

- Wage benefits partially cover income lost when an employee cannot work because of illness or injury. Most insurance covers a percentage of the average weekly wage.

-

- Vocational rehabilitation includes physical and other therapies the injured person needs to get better, as well as general workplace training to avoid more injuries in the future.

-

- Death benefits are paid to an employee’s family if a worker dies on the job. These benefits may include funeral costs and other amounts as required by state law.

-

- Permanent partial impairment (or permanent loss of ability not resulting in death) is when an employee becomes disabled in the workplace and either cannot work or has their ability to work severely limited. Typically, a totally disabled employee will get around two-thirds of their weekly wage.

-

- Temporary disability happens when recovery from an injury or illness takes some time to resolve.

What Does Workers’ Comp NOT Cover

Workers’ compensation doesn’t cover injuries that happen away from the workspace. There are some exceptions, but they vary under state law. It may cover a person who has to travel as part of their job if a road accident happens. It would not cover someone driving to work.

Injuries are not covered when the employee was clearly at fault. This includes injuries resulting from:

-

- A fight that the employee started

-

- Intentional self-harm

-

- Intoxication while at the workplace

-

- Violating company policies

-

- Committing a crime

What About Mental Health?

Requirements for mental health coverage vary by state. Some don’t cover mental health claims that arise from work. Emotional injuries, pain, and suffering are not normally included.

However, as claims (especially for anxiety and depression) become more measurable, more states are including them. In these states, the claims have to be proven to arise from work incidents. But some, like a claim for PTSD after being in a gruesome accident, are more likely to be covered as part of making the employee whole.

How Does Workers’ Compensation Work?

As the employer, you pay a premium every agreed period (such as once a month). An employee raises a claim to you, and you file it with the insurance company. If the company approves the claim, it will pay the bills after you pay any deductible that is part of your policy. In other words, it works like most other insurance policies.

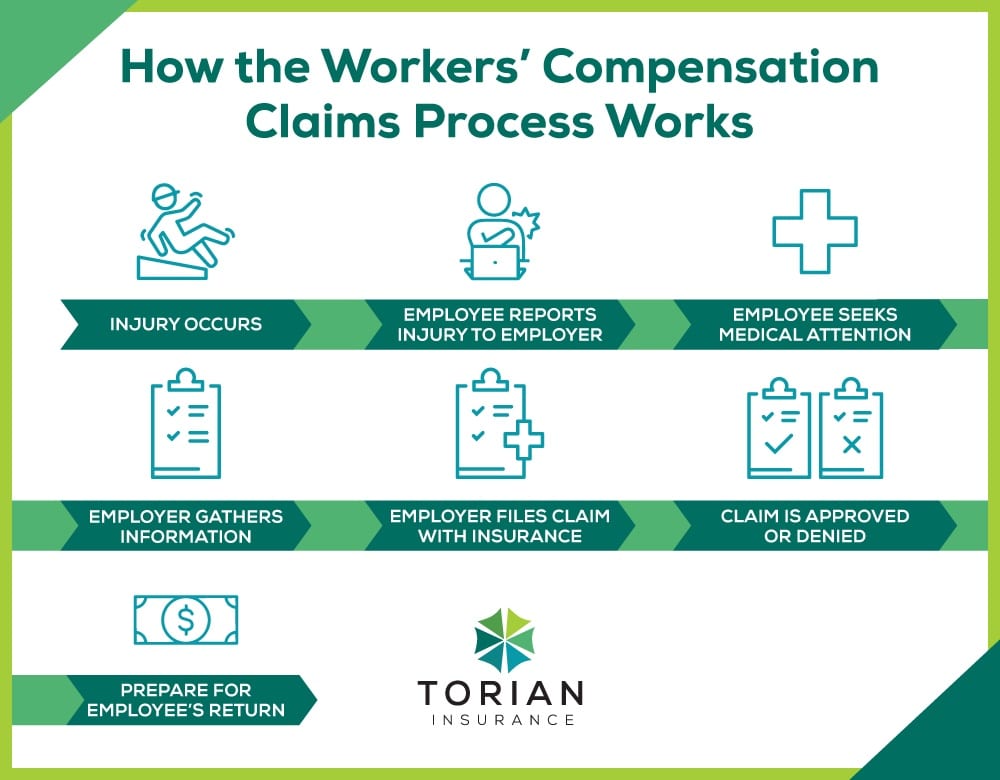

How Does the Workers’ Compensation Claims Process Work?

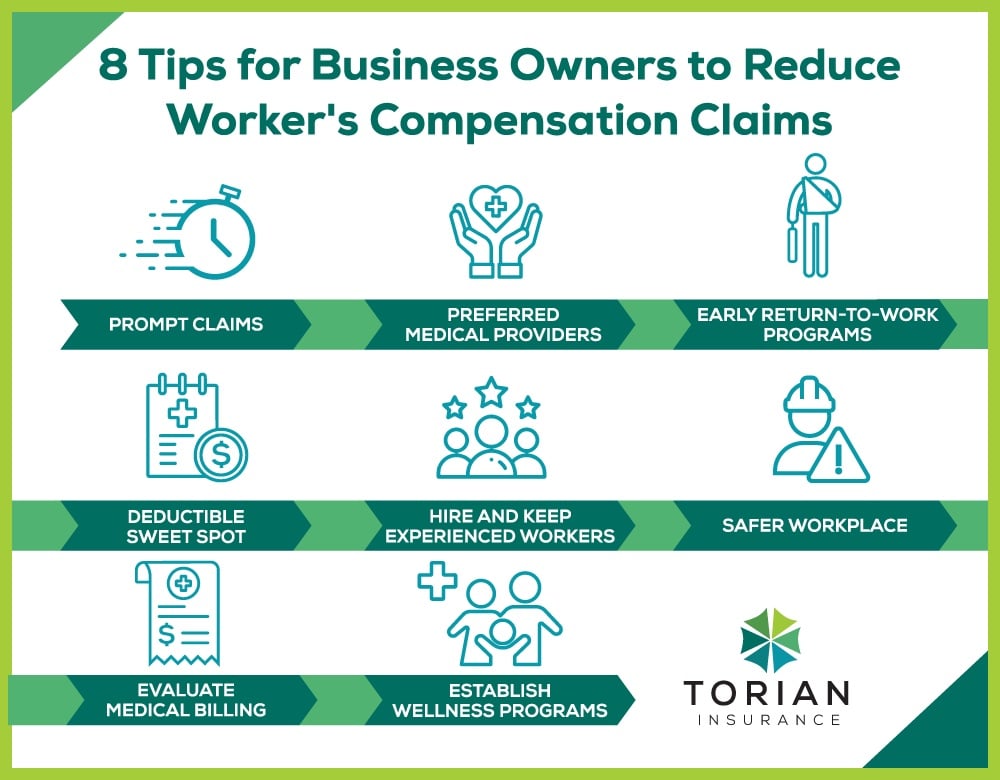

1. Report Claims Promptly

Set up a system where employees report all accidents immediately, even if they do not require medical care. Train all employees on how this works. That way, you can be certain that workers’ comp will cover all insurable injuries and illnesses. You will know where the problem spots in the workplace are.

2. Direct Injured Employee To Specific Medical Care Rather Than Letting Them Choose Where To Go

Most insurance plans have preferred medical providers, from doctors to prescriptions. They have negotiated for the lowest prices, which benefits everyone. These are also providers who know how to file claims with your insurer.

3. Implement Early Return-to-Work Programs

Returning to work as soon as possible, even to a lessened or restricted job, helps everyone out. Most employees will be happy to return to full wages. This also keeps you in touch with your employees and able to track changes in their conditions or care. This may mean bringing back workers part time or in different job roles.

4. Agree to a Deductible

Setting a higher deductible is one of the best ways to lower your insurance premiums. However, you don’t want the deductible to be higher than you or your employees can pay. If you set the deductible too low, your premiums will be too high. Talk to your insurer about finding the sweet spot for your business’ deductible.

5. Hire and Keep Experienced Workers

Employees with more experience working safely in the field will lower your costs. These workers are less risky than newer ones.

6. Solve Health and Safety Problems

Strive to make your workplace safer. A safety audit is a great thing to do. Include asking your workers what aspects of the job they consider to be most dangerous. Increasing training, whether as a group or one-on-one, is another great way to boost safety and so is making sure that your signage is clear and up-to-date.

7. Evaluate Your Medical Billing

Going over the bills your employees send in is the best way to catch potential fraud. You can also spot trends in workplace injuries and develop procedures to deal with them.

8. Establish Wellness Programs

Offering wellness programs at the workplace will help lower your claims rate. You can provide workshops, for example, on major diseases like depression or diabetes. You can also offer exercise or cooking classes before or after work. Stressing the importance of continuing with treatment and making sure your workers get the time off of work they need to go to appointments is important, too.

How To Get Worker’s Compensation Insurance

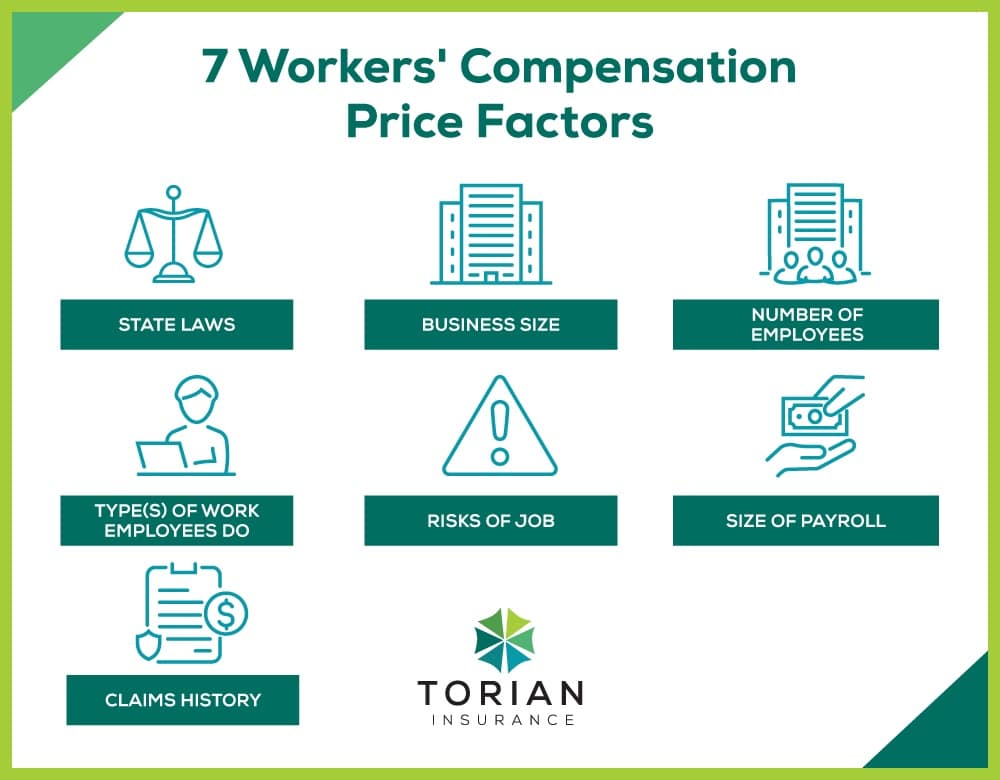

To get workers’ comp, start by calling your state’s workers’ compensation board or your insurance company to determine which laws apply to you. If your business operates in multiple states, you will need to find the laws of each one so you can buy coverage for the employees at these locations.

Torian can help guide you through the maze of workers’ compensation laws in different states. It offers a wide range of workers’ comp insurance policies to fit your business’s needs. The first step is to give us a call at (812) 424-5503 or visit our website.

Worker’s Compensation FAQs

Can I Buy Workers’ Comp Insurance From the State?

Maybe. Businesses in North Dakota, Ohio, Washington, and Wyoming have to buy workers’ comp from the state.

In other states, employers can choose to buy it from either a state or private insurer. These states are Arizona, California, Colorado, Idaho, Kentucky, Louisiana, Maine, Maryland, Minnesota, Missouri, Montana, New Mexico, New York, Oklahoma, Oregon, Pennsylvania, Rhode Island, Texas, and Utah. In some places, only businesses that cannot get insurance through a private insurer use the state option.

In most states, private insurers are the only option. Check out your state laws for coverage choices.

How Long Does Workers’ Compensation Last?

It varies. Workers’ comp generally covers more serious injuries for longer times. An employee who foresees the need for health care over a longer period, for example, should talk to a lawyer about their situation. One who receives a small cut at work may find the doctor’s visit paid for along with a tube of antibiotic ointment. An employee with a leg injury may have a couple of months’ worth of physical therapy before they can return.

Do Some Workers Cost More Than Others?

Yes. Costs are the highest for those workers in the most dangerous jobs. These jobs include lumberjacks, electrical contractors, telecommunications repair workers, construction equipment operators, police, firefighters, and fishers.

Why Can’t You Give Me Any Numbers on Costs?

There is no central clearinghouse of workers’ compensation information. The states keep all information, and different states release different types and amounts of information. Some organizations are working to standardize data collection, but as yet, there is no good way to compare states.

What About Gig Workers (Freelancers or Independent Contractors)?

A gig worker is a freelancer or independent contractor who typically do short-term work for several clients. They often work on a project-based basis or as an hourly or part-time worker. They can work temporarily or ongoing. States continue to refine who is a worker and who is an independent contractor. Some states are considering rules that make it more likely to consider a gig worker an employee. Others are doing the opposite. This is an issue to keep a close eye on.

I’m Ready To Find Out More About Workers’ Compensation Insurance, What Do I Do Next?

Workers’ comp is an important part of providing quality protection for your employees, in case of injury or illness sustained while on the job. It is essential that you are well-informed and have all the information you need to make sure your business is properly protected with a workers’ compensation plan.

There are many cost effective options available these days and more employers are taking advantage of them by shopping around for the best coverage for their businesses insurance needs.

Torian Insurance is here to help you decide which type of worker’s compensation policy is right for your business. Give us a call today if you have any questions or need assistance setting up a policy.