If you’ve suffered a loss or incurred damages, it’s time to review your insurance coverage. You’ll have to file a claim to acquire a reimbursement from the insurance carrier.

The timing as to when you should submit the claim is largely dependent on the size, type and severity of the loss. Larger claims should be submitted immediately whereas a smaller claim is best to delay until you assess the dollar amount of the loss. This is because your insurance rates could rise if the insurer processes a claim and concludes that you’re now a riskier customer.

So how do you know when to file? If the claim involves any injuries or a third party, it should ALWAYS be turned in immediately. Smaller claims, like a first party property only claim, can be delayed a bit to determine the value in relation to the deductible. If the cost comes in under the deductible amount or if the covered portion is minor, you might be better off not filing a claim.

The insurance claim process can be confusing and frustrating, but knowing what to expect and when you should and should submit a claim can help make the process a little less daunting. Read on to learn the 4 main steps involved with the process and the important things to consider with these steps.

Types of Insurance and Insurance Claims

Insurance comes in many forms, some more specialized than others. For a comprehensive guide to the major types of insurance, see common insurance coverages for both individual and family and insurance for businesses on the Torian Insurance website. Below is a deeper dive into some of the most common insurance coverages for consumers—auto, homeowners, renters health and life insurance.

Auto Insurance

When auto accidents happen, sky-high repair and replacement costs ensue. Car insurance works to defray these expenses and covers medical expenses, property damage, damage to the vehicle itself, liability, loss of work, and other damages resulting from an accident.

Most states require car owners to have valid insurance as a condition of using the roads and having title to a car. Each auto policy carries dollar limits for liability, property damage, and bodily injury. They also carry limits for “comprehensive” coverage, meaning damage to or loss of a vehicle in a non-collision incident.

Insurance rates vary with several factors, including where you live, the value of your car, and your driving record. Past accidents and moving violations will push those rates up; older and more experienced drivers with clean records usually get a break on premiums.

Filing a claim may raise your insurance rates, and higher premiums can stick for several years. The risk of this is greater if the accident is judged to be your fault. For minor accidents, drivers also have to consider the policy’s deductible amount, often $500 or $1,000. If damages are less than the deductible, the driver pays the bill, and the risk of bumping up the cost of insurance could mean filing a claim is not advisable.

Homeowners Insurance

If your home is damaged in a storm, fire, or other incident, homeowners insurance covers repairs and loss of use. Homeowners will also pay liability claims filed by a third party for damages or injuries sustained while on the premises.

When you buy a home using a mortgage, the lender will usually require homeowners coverage to protect the collateral used to back the loan. Homeowners insurance arranged this way is usually rolled into the monthly payment for the house.

Premiums vary with the value of your house and by region since some areas are more costly for home repairs than others. One estimate by Forbes showed that the average premium for a $300,000 home reached $1,854 per year in 2022.

Filing a claim may raise that number, with the most important factor being the type of claim. Experian published that one fire claim will bump premiums by 29 percent, and filing a second claim will double that. In decreasing order, homeowners rates will also increase for theft, liability, water, medical, and weather claims.

Renters Insurance

If you rent your dwelling, there’s renters insurance, which covers loss or damage to personal items by fire, flood, storm, or theft. This insurance also covers your liability for injuries a guest or visitor sustains within your apartment or rented house.

Insurance purchased by the owner of the building won’t cover contents of rented spaces, so renters insurance provides some peace of mind for those wanting protection for their televisions, computers, jewelry, collectibles, and other valuable items.

Renters insurance is less costly than homeowners insurance since covered items are likely far less valuable than an entire building. One study found that the average premium for renters was $326 per year in 2022, with the average coverage at $40,000 for property and $100,000 for liability.

Rates will vary, however, depending on location and the policyowner’s credit score and claims history.

Health Insurance

In one form or another, health insurance represents vital financial protection in case of an illness or injury. Medical costs can easily bankrupt the uninsured, as providers will charge “self-paying” customers the full costs for consultations, tests, hospitalization, or emergency care.

Most workers have health insurance through group policies paid for, in part or in full, by their employers. The self-employed and those without group coverage can secure private health insurance or coverage through a public program such as Medicaid, which sets income limits for eligibility. Those 65 and older are eligible for Medicare, a federal insurance program.

Filing a medical claim does not affect the premiums you pay for health insurance. For group policies, those rates increase or decrease each year according to trends in costs and the claims experience of the prior year for the “risk pool.” For the privately insured, rates are set upon application and are re-set annually depending on your age, medical history, and other factors.

Under the Affordable Care Act, a federal health insurance law passed in 2010, rates for the elderly cannot exceed three times the rate for younger, presumably healthier people. Also, insurers cannot raise rates based on overall health, existing medical conditions, or gender.

Life Insurance

Life insurance comes in three forms: term, whole, and universal. A term policy guarantees a set payout — the face value of the policy — if you should pass away, with the benefit payable to beneficiaries named on the policy. Keep in mind this is only within the term of the policy which typically varies from 10 to 30 years. It’s like leasing a car—if you outlive the term, the policy is done.

Whole life is a life insurance policy with a savings or investment account attached. As premiums are paid in, the account gains value. Plus, you can borrow tax-free money against it if needed for unexpected expenses. A universal policy is active for the individuals lifetime, no matter how many changes are made and regular contributions can be made to build up additional savings.

Out of the more traditional types, term life is the more straightforward and less expensive alternative whereas whole life may offer a way to save cash, but so does a tax-exempt IRA, which generally charges less in the way of advisory fees.

Filing a claim won’t affect rates for beneficiaries (or otherwise cost them) since paying out on a policy means the contract has been fulfilled and effectively terminated.

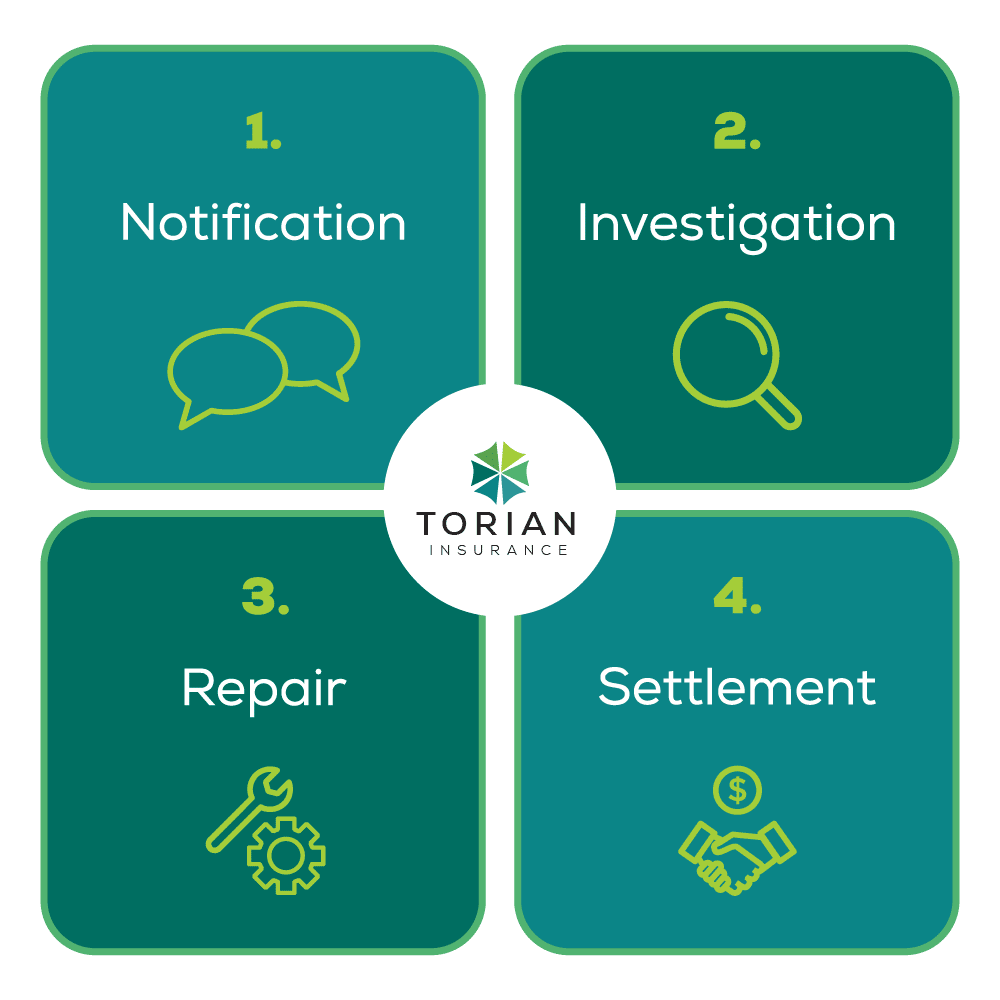

The 4 Main Steps of an Insurance Claim Process

Filing a claim can seem complicated. But with these four essential insurance claim process steps, you’ll go from confused to confident in the event of an accident.

1. Notification

The first step is to notify: advising your insurance company that you want to file a claim. It’s important to gather evidence, such as photos and/or videos, and to file police reports in the case of a theft.

The insurance policy should detail the period of time you have to make a notification; if you miss this window, the insurer can deny the claim.

Notification usually means calling the insurance company or going to the insurance company’s website where a “File a Claim” or similar tab or banner should be available. If a third party is filing a liability or damages claim against you, the insurance company or agent will notify you with a letter. If you use an agent for notification, make sure the agent provides written confirmation of when the claim was submitted. However, if you are working with an insurance agency, they will do the hard work for you and take care of notifying the company on your behalf.

The insurance company will ask for details, such as the time and location of the accident, as well as the damages suffered, such as windows broken or roof damage in a heavy storm. You can also provide an estimate of the damages.

The notification process is for gathering basic information surrounding the claim and brings the following stage — investigation.

2. Investigation

During the investigation process, the insurance company will gather information about the incident to determine coverage and liability. You will have to provide repair bills or estimates. In some cases, the insurance company will provide an authorized business to do the estimating.

Insurers assign adjusters in cases where the damage amount and/or fault needs to be determined. The adjuster may call, e-mail, or write to request bills and other paperwork. They will explain any coverage limits or deductibles and may also ask for accident or police reports, witness statements, photographs, and/or medical bills. This would also be the stage to explain any time lost from work.

Health insurance claims are handled between the medical provider and the insurance company. The insurance company will adjust the cost for its own payment and bill you for any deductible or non-covered expenses. For a life insurance claim, the beneficiaries must provide details surrounding the insured’s passing and a death certificate.

3. Repair

Repairing damages in cooperation with the insurance company is the next step in the claims process. The insurance company works with you and/or your contractor to get the damage repaired as quickly as possible.

The insurance company will sometimes assign an authorized shop or contractor to handle repairs. This is often the case when a big storm affects many households in a given area or a hailstorm damages thousands of its insured cars.

For some claims, a contractor or repair shop will deal directly with the insurance company, but any paperwork you sign allowing this may turn the claim over entirely to a third party. Read the document carefully before signing it.

In some cases, the insurance company will offer a lump sum payment to cover any repairs and/or replacements. When you accept this payment, the claim is closed, and the insurance company will have no further obligation.

4. Settlement

Auto, homeowners, and renters insurance claims end with a settlement when the insurer pays out funds to you for the damages or repairs. If the amount of the settlement offer is insufficient, you can negotiate for a higher amount. This can be done through an attorney who’s skilled and experienced in handling insurance claims.

For homeowners and renters, insurance companies will work from the evidence you provide, including a home inventory for replacement. The insurance company will offer cash value (or depreciated value) for lost or damaged items. Once you’ve replaced the item, you can submit the invoice or receipt to claim the full replacement cost.

For vehicles totaled in an accident where repair costs exceed the value of the vehicle, the insurance company will offer depreciated value of the vehicle, which takes into account mileage, model, and age.

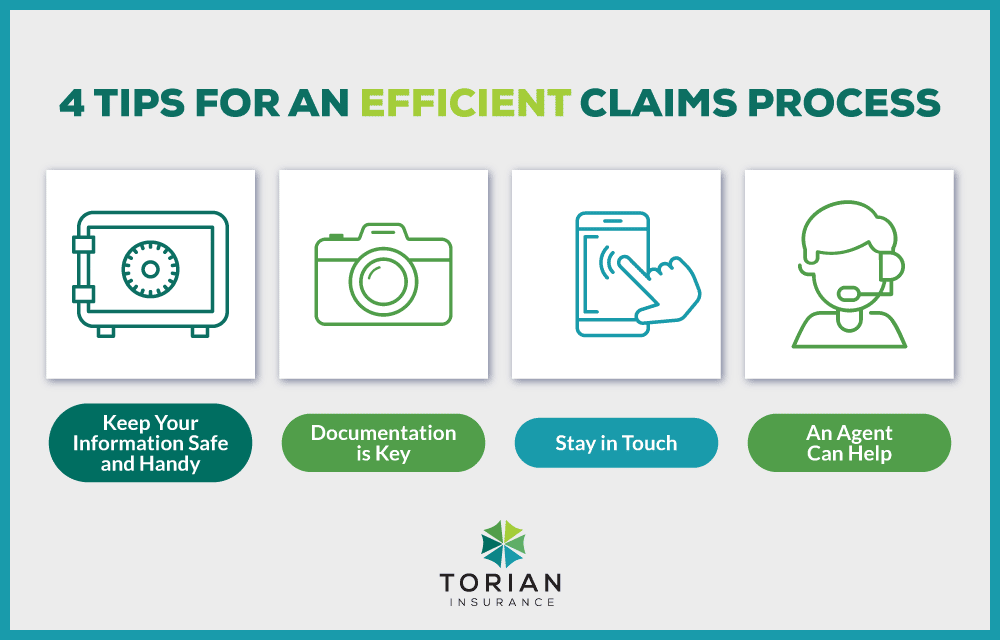

Tips for Making the Claims Process Easier

Keep Your Information Safe and Handy – It’s vital to keep your insurance documents in a safe place and review them from time to time so that you know what’s covered. The policies will also detail how to submit an insurance claim and how much time you have to file a claim after the loss.

Documentation is Key – If you suffer a loss or accident, document the damages with receipts, photographs, videos, and reports. Gather any witness information, and get a copy of the police report in the case of a theft.

Stay in Touch – Once a claim is filed, stay in touch with the adjuster. They may be handling many cases at once, and chances are good that the reasons for a routine glitch or holdup won’t be communicated promptly. Asking questions won’t cost anything, and the adjuster should know that you’re on top of the process.

An Agent Can Help – The same goes for your insurance agent. Although it’s the agent’s responsibility to help you through a claim, communication is the key to managing your own expectations and running the process smoothly.

Finding the Right Insurance Agent

An insurance agency can help you select the right coverage from the start and advise you on the costs of a policy across several providers.

Torian Insurance provides an easy, straightforward guide to the insurance claim process to help you make an informed decision. Torian offers a wide variety of specialized insurance, including business continuation life, condo insurance, and Medicare supplemental insurance, among many others.

For details on these or any insurance-related questions, contact Torian at 812-625-3127 or try our convenient online chat feature, available from any page on the Torian website.