Choosing who handles your insurance can feel as confusing as the policies themselves. If you have been comparing your options, you have probably run into the term “independent insurance agency” and wondered what an independent insurance agency is, whether it costs more, and whether it actually works in your favor. This guide explains how independent agents work, how they get paid, how they differ from captive agents and brokers, and how to choose one in the Indiana, Kentucky, and Illinois tri-state area.

Key Takeaways

- An independent insurance agency represents multiple insurance carriers rather than one company, so it can shop your coverage across many insurers instead of selling a single company’s products.

- Independent agents are usually paid through commission from the carrier, not through a separate fee billed to you, so working with one generally does not cost more than buying directly.

- Independent agents wrote 87.2% of U.S. commercial lines premium and 39.0% of personal lines premium in 2024, according to the Big “I” 2025 Market Share Report, which makes the independent channel the standard for business insurance.

- The core difference between an independent and a captive agent is who they work for: an independent agent works for you across many carriers, while a captive agent represents one insurance company.

- A local independent agency adds regional knowledge of tri-state weather, property risks, and state rules that a national call center cannot match.

- When choosing an agency, weigh licensing, experience, range of coverage, and claims handling, because the cheapest quote is not always the best long-term fit.

What Is an Independent Insurance Agency?

An independent insurance agency is a licensed business that represents multiple insurance carriers and shops their policies on your behalf, rather than working for a single insurer. The agency is not the company that pays your claims. That company is the carrier (also called the insurer or underwriter), which underwrites the policy, sets the premium, and pays claims. The agency is the advisor that helps you find, buy, and manage the right coverage from among many carriers.

It helps to keep three terms straight, because they are easy to confuse:

- Insurance carrier: the company that underwrites the policy and pays claims (for example Acuity, Cincinnati Insurance, or Hanover).

- Insurance agency: the licensed business that represents one or more carriers and helps you choose and service coverage.

- Independent agency: an agency that is not tied to one carrier and can compare your options across many of them.

The model is widespread. There are roughly 39,000 independent insurance agencies across the U.S. as of 2024, a figure from the Big “I” and Future One 2024 Agency Universe Study, and they are the dominant way American businesses and a growing share of families buy property and casualty coverage.

Independent Agent vs Broker: What’s the Difference?

In everyday conversation the words overlap, but there is a technical distinction. An independent agent represents insurance carriers and can bind coverage (put a policy in force) on their behalf. A broker represents you, the buyer, shops the market, and usually cannot bind coverage directly. For most personal and small business insurance in the tri-state area, you will work with an independent agent who can place and service your policy directly.

Independent vs Captive Insurance Agent: What’s the Difference?

The difference comes down to who the agent works for. A captive agent represents a single insurance company and can only sell that company’s products. An independent agent represents many carriers and compares them for you, so if one carrier raises rates or stops writing a type of policy, the agent can move you to another without you having to start over with a new agent.

The table below lays out the practical differences.

| Factor | Independent Agent | Captive Agent |

| Who the agent works for | Works for you and represents many carriers | Works for one insurance company |

| Choice of carriers | Shops and compares multiple carriers | Sells one carrier’s products only |

| Who owns the book of business | The independent agency | The insurance carrier |

| Switching carriers | Can re-shop carriers without changing agents | Switching usually means leaving the agent |

| Claims support | Advocates for you across carriers | Represents the carrier’s position |

One row deserves a definition. A book of business is the collection of policies an agent or agency manages. With an independent agency, the agency owns the book, so if your needs change you can re-shop carriers and keep the same agent and the same point of contact.

How Do Independent Insurance Agents Make Money?

Independent insurance agents are paid primarily through commission, a percentage of your premium that the carrier pays the agency when a policy is placed or renewed. In most personal and small business cases, you do not pay a separate fee to work with an independent agent, and that commission is already built into the carrier’s premium whether you buy through an agent or directly from the company.

Here is how the money usually flows:

- Commission: the carrier pays the agency a percentage of the premium when a policy is placed or renewed. This is the standard arrangement for home, auto, and most small business policies.

- Disclosed fees: in some commercial or specialty placements, an agency may charge a service fee for added work, which should be disclosed to you up front before you agree to it.

So do independent agents cost more than buying directly from a carrier? Generally, no. Because the commission is built into the premium either way, going through an independent agent does not add a markup in most personal and small business situations. What you gain is someone who compares carriers, explains the differences, and handles claims on your behalf, at no extra cost in the typical case.

Benefits of Working With an Independent Insurance Agency

The main benefit of an independent insurance agency is that the agent works as your advisor and advocate rather than as a salesperson for one company. Instead of fitting you into a single insurer’s products, an independent agent matches your needs to the carrier that fits them best, then stays in your corner when something changes or a claim is filed.

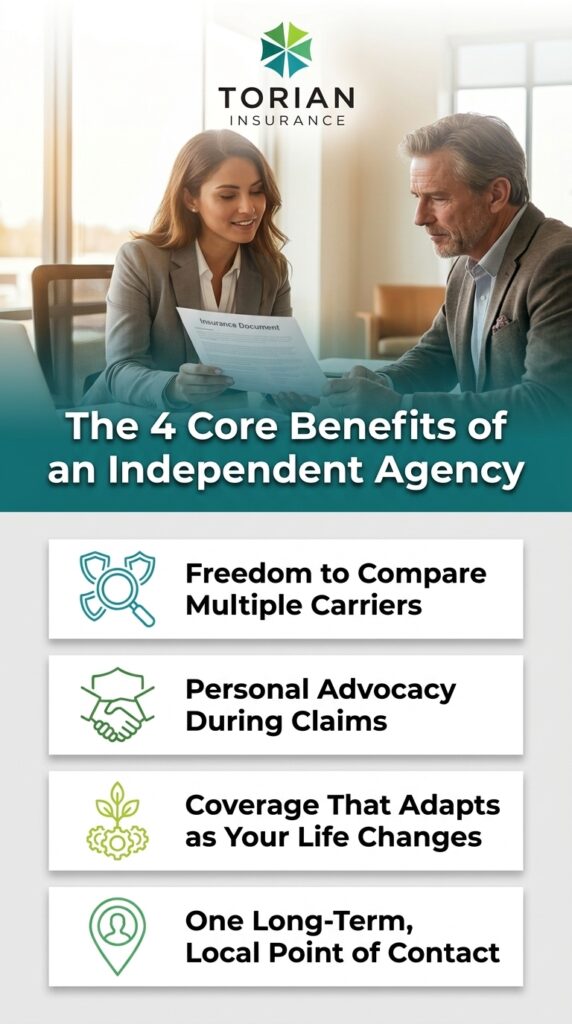

The practical advantages tend to fall into four areas:

- Choice across carriers: the agent compares coverage and pricing from many insurers, so you are not limited to one company’s appetite or rates.

- Claims advocacy: when you file a claim, your agent can help you navigate the process and advocate on your behalf with the carrier.

- Lifecycle adaptability: as your life or business changes (a new home, a new vehicle, a growing payroll), the agent can adjust coverage and re-shop carriers without you switching agents.

- One relationship over time: you build a long-term relationship with a person who knows your history, instead of starting over with a call center each renewal.

This is not a niche channel, and the Big “I” market-share data shows why. Independent agents wrote 87.2% of U.S. commercial lines premium in 2024, and their personal lines share grew from 35.7% in 2020 to 39.0% in 2024. In other words, the independent model is the standard for business insurance and a steadily growing choice for home insurance and other personal lines.

Why a Local Insurance Agency Matters in the Tri-State Area

A local independent agency brings regional knowledge that a national direct seller cannot. They understand tri-state weather patterns, local property and liability risks, and the insurance rules that differ across Indiana, Kentucky, and Illinois. That context shapes the coverage they recommend and the gaps they help you avoid.

Local value tends to show up in a few specific ways:

- Regional knowledge: familiarity with Ohio River flood exposure, severe storm risk, and the coverage questions that come up across the IN, KY, and IL markets.

- Community engagement: a locally owned agency is part of the same community it serves, which keeps it accountable to its neighbors.

- Accessibility: you can reach a real person who knows your account, rather than a rotating queue of representatives.

- Long-term relationships: coverage that adapts as your family or business grows, guided by someone who already knows your history.

Heritage is part of this. Torian Insurance is Evansville’s largest locally owned independent agency, founded in 1923 with more than 100 years of service to the tri-state. The agency is locally owned, not a franchise or a bank-owned office, and it is a Trusted Choice member agency. You can read more about its local roots and team on the About page.

How to Choose an Independent Insurance Agency

Choosing an independent insurance agency comes down to fit, expertise, and how they handle you when something goes wrong. The goal is to leave a conversation feeling consulted, not sold. Use these criteria to compare your options:

- Confirm licensing: make sure the agency is licensed in your state. A tri-state buyer should confirm coverage in Indiana, Kentucky, or Illinois as needed.

- Ask about experience and specialization: years in business and familiarity with your situation (contractor, homeowner, nonprofit, small business) matter more than a flashy quote.

- Check the range of coverage offered: an agency that handles both personal and business lines can grow with you instead of sending you elsewhere later.

- Ask how claims are handled: find out who you call when you have a claim and how the agency advocates for you with the carrier. This is where the relationship earns its value.

- Look at community involvement and references: local roots and real client recommendations are reliable signals of how an agency treats people over time.

- Remember that the cheapest quote is not always the best fit: a slightly higher premium with the right coverage and a responsive agent often costs less than a bargain policy with a gap you discover at claim time.

How Torian Insurance Helps

At Torian Insurance, we work the way this guide describes. We are an independent agency, founded in 1923 and based in Evansville, and we shop multiple carriers (including Acuity, Chubb, Cincinnati Insurance, Hanover, and Philadelphia, among others) to match your coverage to the right insurer instead of fitting you into one company’s products. We are licensed in Indiana, Kentucky, and Illinois, and we are a Trusted Choice member agency.

Our team brings more than 600 years of combined experience across personal and business insurance, and we stay with you as your needs change. Whether you are a small business owner sorting out liability coverage or a family adjusting a home and auto policy, you work with people who know your account. You can meet the people behind the agency on our team page and read what clients say on our client testimonials page.

We see our role as advisor and advocate. That means explaining your options in plain language, helping you weigh coverage against cost, and standing with you when a claim is filed.

Frequently Asked Questions About Independent Insurance Agencies

What is the difference between an independent insurance agent and a broker?

An independent agent represents insurance carriers and can bind coverage on their behalf, while a broker represents the buyer and shops the market but usually cannot bind coverage directly. In practice, most people buying personal or small business insurance work with an independent agent who can place and service the policy from start to finish.

Do independent insurance agents charge fees?

In most personal and small business cases, no. Independent agents are typically paid by commission from the carrier, which is already built into your premium. Some commercial or specialty placements may involve a disclosed service fee, but that should be explained to you up front before you agree to it.

Are independent agents better than captive agents?

Neither is universally better, but they serve different needs. A captive agent can be a fit if you want one specific company’s products. An independent agent gives you choice across many carriers and can re-shop your coverage without you changing agents, which is why the independent channel handles the large majority of commercial insurance.

Is an independent insurance agency a franchise?

Not necessarily. Some agencies are part of national franchises, but many are locally owned, independent businesses. Torian Insurance, for example, is locally owned and not a franchise or bank-owned office, which keeps decisions and accountability in the community it serves.

How often should I review my insurance policy with my agent?

A good rule is once a year at renewal, and any time something significant changes, such as buying a home, adding a vehicle, hiring employees, or starting a business. Regular reviews help catch coverage gaps before they turn into uncovered claims.

Working With a Local Independent Agency in the Tri-State

An independent insurance agency gives you choice, advocacy, and a relationship that adapts as your life and business change, usually at no extra cost compared with buying direct. If you want to understand your coverage or compare your options with a local agent, contact Torian Insurance to talk through your situation and find the right fit.