With the introduction of tools like Airbnb and Vrbo, it’s become commonplace for people to rent their homes out when they don’t use them. For example, you may have a vacation home that collects dust nine months out of the year, or you may be planning a three-week vacation in which your primary home will be empty.

You can choose to rent your home out as a vacation property when you’re not using it.

Although this opens the door to a stream of income, it also opens the door to liability. Before you dive into the short-term rental insurance scene, it’s important that you consider opening a short-term rental insurance policy.

What Is Short-Term Rental Insurance?

Short-term rental insurance, also commonly called vacation rental insurance, is a unique type of insurance that’s specifically designed for short-term rentals. These are properties that you plan on renting out for a series of days, rather than months. Short-term rentals may be single-family homes, condos, townhomes, or any other type of property.

This is a crucial type of insurance to carry if you rent out your home because, in the vast majority of cases, your homeowners insurance policy won’t cover damage caused by short-term guests.

What Does Short-Term Rental Insurance Cover?

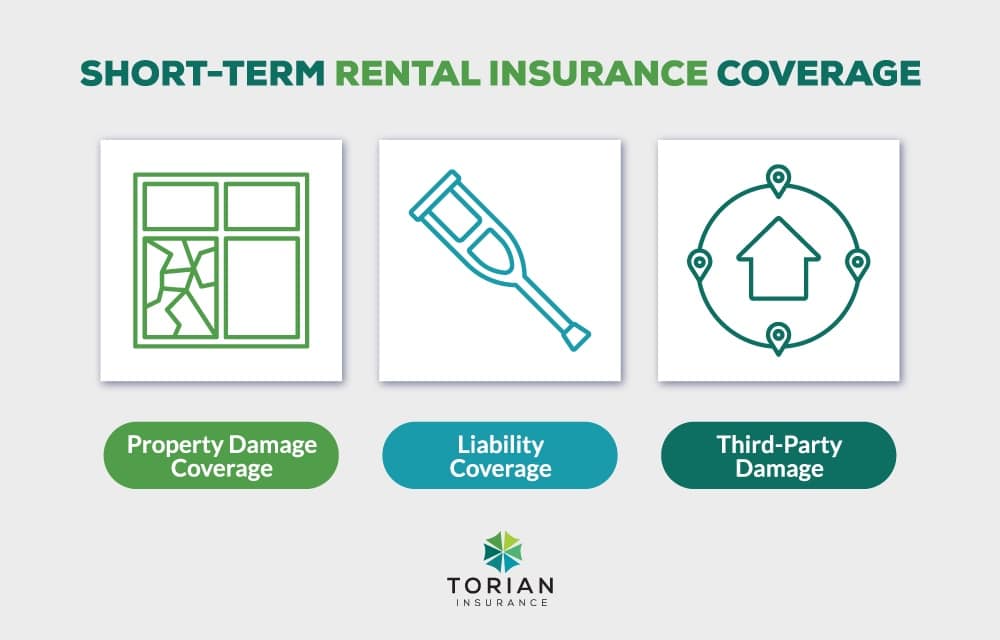

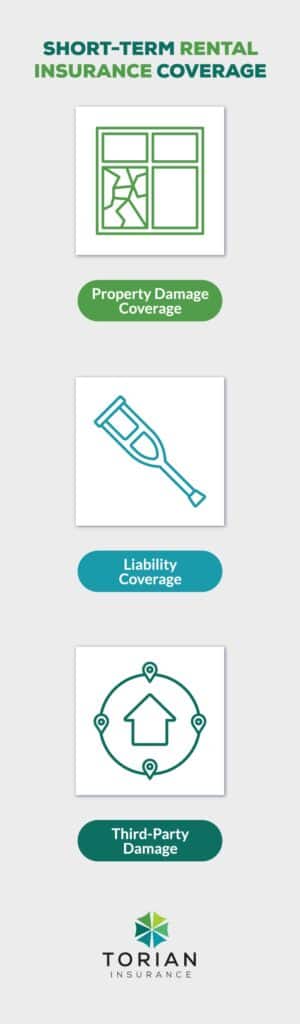

Short-term rental insurance policies offer a wide range of coverages. Most importantly, these policies provide:

- Property Damage Coverage: What happens if your guest throws a party, resulting in significant damage to walls, furniture, doors, and more? It may be nearly impossible to collect monetary compensation from your guests, but if you have insurance coverage, you won’t have to.

- Liability Coverage: Accidents happen. Sometimes, those accidents lead to injuries, and those injuries can become your liability. If a guest is hurt on your property, you may be forced to foot the bill. However, a short-term rental insurance policy can alleviate this risk.

- Third-Party Damage: What if something your short-term guest does causes damage to your neighbor’s home? You guessed it… you’re on the hook. The good news is that a quality short-term rental insurance policy will cover these costs.

How Much Does Short-Term Rental Insurance Cost?

As is the case with all forms of insurance, the cost of short-term rental insurance will vary wildly depending on a wide range of factors. Some of the most important factors that play a role in pricing include:

- Location: You might pay less for properties located in rural areas than you will for properties in bustling cities. However, rural areas have fewer fire hydrants and few fire departments which can drive up property rates since they are more likely to burn longer if a fire starts.

- Property Value: As with any other insurance policy, the amount of coverage you need will play a major role in your premiums.

- Deductible: You’ll pay lower premiums when you agree to a higher deductible, and vice versa.

Most of the factors that play into the cost of short-term rental insurance are out of your control. However, speak with your insurance agent about adjusting coverage caps and deductibles to meet your financial needs.

Who’s Liable if a Renter Is Injured?

If you rent your home out and a guest gets injured, liability becomes a major cause for concern. In some cases, you’ll be liable, while the guest will be in others.

When you rent your home to a short-term guest, you’re attesting that your home is in a safe living condition. That means that nothing in the home should risk bodily injury to your guest. So, if you have a loose railing next to the stairs that results in someone falling and getting injured, the liability associated with that injury falls on your shoulders.

On the other hand, if a guest spills a drink on a hard surface and later slips on it, the guest is liable for the injury. After all, there is nothing you could have done as the property owner to stop the injury from happening.

The key here is maintenance. However, you may not always know exactly when a leak starts, a screw loosens, or a battery dies. That’s why it’s so important to have quality short-term rental coverage.

Who’s Liable for Property Damage?

Liability is always a question of causation. If your guest caused property damages while on your property, that guest is liable for the damages. If neglected maintenance results in damage, that damage is on your shoulders.

On the other hand, your guests may not always be responsible. What happens if a guest causes damages and you’re unable to collect monetary compensation? If you have insurance, you can file a claim and have the damage taken care of. If not, your home may be out of commission for a while as you work toward repairing the damage.

Is My Short-Term Rental Already Covered?

Oftentimes, property owners believe their short-term rental is already covered by another form of insurance they have on the property — homeowners insurance, landlord insurance, or insurance provided by their vacation rental hosting platform.

Unfortunately, that’s not always the case. If you’re not absolutely sure that you’re covered, it’s always better to re-read the fine print of your insurance policy before you take the leap and rent out your home.

Homeowners Insurance

Homeowners insurance policies are designed to cover homes that are occupied by the homeowner and their family. These policies typically don’t cover properties that are used for commercial purposes like short-term rentals. That’s because the use of the property as a short-term rental opens the insurance company up to more risk associated with their coverage.

As a result, there’s a strong chance that your homeowners insurance policy won’t cover anything that happens to your property while a short-term renter occupies it. There are some exceptions to the rule.

Some insurance companies offer additional coverage to homeowners’ policies for short-term rentals. However, you’ll know it if you have additional coverage, as it comes with additional fees.

Landlord Insurance

Landlord insurance is a specific type of insurance designed to cover landlords when they rent their homes out as primary residences to tenants. This type of insurance is similar to homeowners insurance in that it protects the property but typically doesn’t protect the contents of the property.

Moreover, landlord insurance doesn’t offer any protection when it comes to the use of the property as a short-term rental for the same reasons homeowners insurance doesn’t cover these activities. Ultimately, short-term rentals pose more risk to insurance companies than homes that are used by a single occupant or single family.

Hosting Platform Insurance

Most popular hosting platforms like Airbnb and Vrbo offer at least a limited form of insurance to protect you from financial damages. However, this insurance may provide little more than a false sense of security, depending on the platform you choose to use when you rent your home out.

Airbnb

If you use Airbnb to rent your home out, you’re in luck. The company offers a program called Airbnb Host Protection Insurance. The program offers the following coverage:

- Liability: This covers you if a guest is injured on your property or if a guest causes damage to a neighboring property.

- Property Damage: This includes any damage to your property or a guest’s property as the result of a covered event.

Airbnb caps this coverage at $1 million per instance per location. The good news is that property owners don’t pay a dime for this coverage as it’s already included in Airbnb’s fees.

Unfortunately, there are many areas where you’re not covered under Airbnb’s insurance policy. In particular, they won’t cover damage or injury that was done on purpose, which could open you up to a significant financial burden if you host a bad guest.

Vrbo

Vrbo (Previously called HomeAway) also offers an insurance program. Under their program, property owners have access to $1 million in liability coverage. This coverage protects you if a guest is injured on your property or if a guest causes damages to a third-party property.

Unfortunately, Vrbo doesn’t provide coverage for your property. So, if a guest damages your property, you’ll be on the hook for those damages.

Get Short-Term Rental Coverage With Torian Insurance

The decision whether or not to purchase a short-term rental insurance policy is one that should be made with the help of an expert. After all, your property is just as unique as you are and a valuable asset to protect.

Torian Insurance has been helping customers protect their assets since 1923. In that time, they’ve created relationships with leading underwriters and mastered the art of pitting insurance companies against each other to compete for your business. In the end, you get the best possible coverage at the best possible price. Contact Torian Insurance to find out how short-term rental insurance can protect you.