Adding a driver to your car insurance usually comes up at a specific moment. A teen earns a license, a partner moves in, or an adult child comes back home. The rules for who has to go on your policy, who you can leave off, and what it does to your premium are not always obvious, so this guide covers all three, along with the practical ways a family can keep the cost in check.

Key Takeaways

- Licensed household members who drive your car generally must be listed on your policy, including a spouse, a parent who moves in, or an adult child back home.

- A teen driver can add 50 to 100 percent to a family’s auto premium, the single biggest reason costs jump when you add someone.

- It is usually cheaper to add a teen to your existing policy than to buy them a separate one.

- You can sometimes exclude a driver to lower the premium, but if an excluded driver crashes your car, the claim can be denied.

- The largest savings come from shopping multiple carriers, since insurers price young and new drivers very differently, and an independent agent can compare those prices for you.

- Tell your agent early, ideally at the learner’s permit stage, so coverage lines up with the license date.

Who You Have to Add, Who You Can Skip, and Who You Can Exclude

In general, any licensed person who lives in your household and has access to your car should be on your car insurance policy. Insurers assume household members might drive your vehicle, so leaving an eligible driver off can create a coverage gap. A few people can be skipped, and in some states one can be formally excluded.

Three terms come up often when you sort this out:

- Listed driver: a person named on your policy and rated for coverage.

- Permissive user: a licensed driver who uses your car occasionally with your permission, usually covered even without being listed.

- Named driver exclusion: a formal removal of a specific person from your coverage, available in some states.

Here is how the most common household situations usually break down:

| Household situation | On your policy? | Why or watch-out |

|---|---|---|

| Teen with a learner’s permit | List them | Tell your agent early. A permit usually has little premium impact until full licensure. |

| Teen with a full license | Yes, required | The biggest premium impact (50 to 100 percent, III). This is where the offset strategies below matter most. |

| Spouse or partner you live with | Yes | Most insurers require licensed household members to be on the policy. |

| Parent who moved in | Yes, if they will drive your car | Any licensed household member with access to the car should be listed. |

| Adult child back home | Yes, if licensed with access | Common when kids return home. List them if they will drive your car. |

| Roommate with their own car and insurance | Usually not required | Occasional use is covered as a permissive user. Confirm with your insurer. |

| Nanny or caregiver who drives regularly | Yes | Regular use by a non-household driver should be listed. |

| Household member who will not drive | Consider a named driver exclusion, where allowed | If an excluded driver drives and crashes, the claim can be denied. |

Rules vary by insurer and by state, so treat this as a starting point and confirm the specifics with your agent.

Why Adding a Driver Raises Your Premium

Adding a driver raises your premium because your policy now covers another person who could be behind the wheel, and the insurer prices that added risk. How much it rises depends on the driver’s age, experience, and record. A new or young driver moves the number the most.

The size of the increase tracks the driver you are adding:

- A teen or newly licensed driver: the largest jump, since limited experience means a higher chance of a claim.

- An experienced adult with a clean record, such as a spouse: often a modest change, and adding a second vehicle can unlock a multi-car discount.

- A driver with a serious violation: a bigger increase, and in some cases an SR-22 filing may be required before they can be added.

Adding a Teen Driver: The Cost and How to Offset It

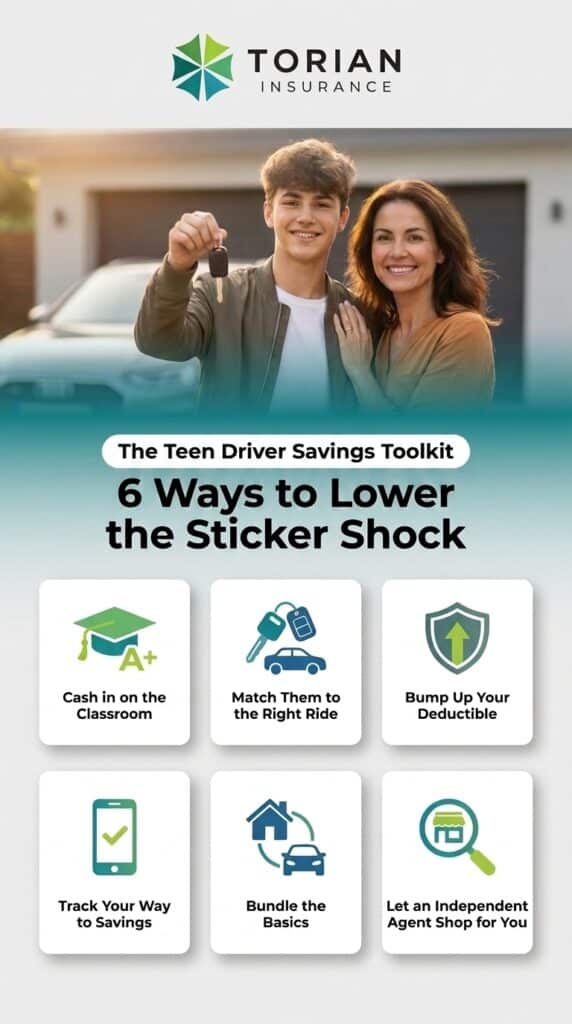

A newly licensed teen is the most expensive driver to add, but the increase is manageable. Teen drivers can add 50 to 100 percent to a family’s auto premium, and several proven strategies bring that down without cutting the coverage that actually protects you.

Why Teen Premiums Are Higher

Insurers price teens higher because limited driving experience means a greater chance of a claim. The encouraging part is that rates typically fall as a teen builds a clean driving record over the next few years.

Ways to Offset a Teen Driver’s Premium

Consumer Reports’ programs director for advocacy, Chuck Bell, points families toward four levers: comparing rates across insurers, combining home and auto coverage, taking a higher deductible (the amount you pay out of pocket before coverage applies), and putting the teen in a safe, budget-friendly vehicle. Here is how to act on that, plus a few common discounts:

- Good-student and driver-education discounts: many insurers reduce the premium for a teen who keeps at least a B average or completes a recognized driver-training course.

- Assign the teen to the least valuable car: insurers often rate the most expensive driver on the most expensive vehicle, so pairing your teen with the lower-value car can lower the cost (III).

- Raise your deductible: a higher deductible lowers your premium, as long as you can comfortably cover that amount after a claim.

- Enroll in a telematics program: usage-based programs that monitor how a car is driven can earn a discount. Consumer Reports’ 2024 survey found telematics users saved a median of $120 on their annual premium.

- Bundle home and auto: insuring your home and auto together typically earns a multi-policy discount.

- Shop multiple carriers: insurers price young drivers very differently, so comparing carriers is where the real savings live, and an independent agent can run that comparison for you.

One Coverage Not to Cut: Liability

While you look for savings, keep your liability protection strong. The III recommends carrying higher liability limits, and considering a personal umbrella policy, when a teen is on your policy, because a serious at-fault crash can exceed standard limits and leave you responsible for the difference.

Can You Exclude a Driver to Lower Your Premium?

Yes. In states that allow it, you can formally exclude a specific driver through a named driver exclusion, which can lower your premium. The tradeoff is real: if an excluded driver ever drives your car and has an accident, the claim can be denied, and you could be left paying out of pocket.

- When an exclusion can make sense: a licensed household member who genuinely will not drive your car, for example someone away at college with no access to it.

- The risk to weigh: if the excluded person drives and crashes, insurers can deny the claim, and some situations can even lead to policy cancellation.

How to Add a Driver to Your Car Insurance

Adding a driver is usually a quick call or message to your agent. Have the new driver’s details ready, and time the change to their license date so coverage is in place the moment they start driving on their own.

The process generally looks like this:

- Gather the driver’s information: full legal name, date of birth, and driver’s license number.

- Note their driving history: tickets, accidents, or coverage lapses, since these affect the rate.

- Contact your agent early: for a teen, reach out at the learner’s permit stage. A permit usually has little premium impact until full licensure, and starting early keeps coverage from lapsing.

- Confirm the primary vehicle: tell your agent which car the new driver will mostly use, since that affects how the policy is rated.

- Ask about discounts: good-student, driver-education, telematics, and bundling can all apply.

In Indiana, new drivers move through a graduated licensing process, from a learner’s permit through the Indiana BMV to a full license. Letting your agent know at the permit stage keeps your coverage aligned as your teen moves through each step.

How Torian Insurance Helps

At Torian Insurance, we are an independent agency, not a single carrier. When you add a driver, especially a teen, we can shop your situation across multiple carriers and compare how each one prices that driver. Because insurers weigh age, experience, and vehicle differently, the same teen can cost very different amounts from one company to the next.

We also help you keep the right protection in place while you look for savings. That means reviewing your liability limits, talking through whether a named driver exclusion or a telematics program fits your family, and confirming that every discount you qualify for is actually applied. Our team of local agents does this every day for families across Evansville, Southern Indiana, and the tri-state area.

Many clients stay with us as their families change, which is exactly when coverage needs shift. Here is what one longtime client shared:

Frequently Asked Questions About Adding a Driver to Your Car Insurance

Do I have to add my teen if they only drive occasionally?

In most cases, yes. Insurers generally expect any licensed household member with access to your car to be listed, even for occasional use. Requirements vary by insurer, so confirm how yours defines a household driver.

Is it cheaper to add a teen to my policy or get them their own?

It is usually cheaper to add a teen to your existing policy than to buy a separate one for them. A driver under 18 typically cannot purchase their own policy anyway, so adding them to a parent’s policy is often the only practical option.

What information do I need to add a driver?

You will need the driver’s full name, date of birth, and driver’s license number, plus their driving history. Knowing which vehicle they will primarily drive helps your agent rate the policy accurately.

Can I remove or exclude a driver to lower my premium?

In states that allow it, you can exclude a specific driver through a named driver exclusion, which can lower the cost. Be careful, though: if that excluded driver uses your car and crashes, the claim can be denied, so weigh the savings against the risk.

Does adding a driver always increase my premium?

Not always. Adding an experienced driver with a clean record can have a small effect, and adding a second vehicle may qualify you for a multi-car discount. A new or teen driver is what usually drives the biggest increase.

Talk With a Local Agent Before You Add a Driver

Adding a driver is a good moment to confirm your coverage still fits your household and that you are not leaving savings on the table. Whether you are adding a teen, a spouse, or a family member who recently moved in, we can review your policy and compare carriers to find the right fit. Contact Torian Insurance to talk it through with a local agent.