If you’re like most people, you probably have some kind of insurance coverage. You might have health insurance, life insurance, auto and home insurance, etc. Maybe you have felt like you need a little extra protection and have considered umbrella insurance. But what exactly is it? Do you really need it and do the costs outweigh the benefits?

What Is Umbrella Insurance?

Umbrella insurance is an additional layer of protection beyond your standard policies that helps safeguard your finances in the event that you’re sued. An umbrella policy kicks in when the limits on your auto or homeowners insurance have been reached.

Also sometimes referred to as personal liability insurance, personal umbrella insurance is not a stand alone policy. It is a supplemental policy that you have in addition to your existing policies such as car, home, and renters insurance.

The main benefit of umbrella insurance is that it protects you from financial losses in the case of unforeseen events. For example, if you are in a car accident and are held liable, your umbrella insurance would cover you for any serious claims that exceed the limitations of your standard policy. To be clear— it is not going to cover things that a standard policy does not cover, it is there to provide additional limits for things that ARE covered in your primary policies when the limitations are exceeded.

Umbrella insurance plays a key part in protecting your assets; without this type of coverage your home equity, retirement savings, and more are at risk if a claim is filed against you. Even your future income can be considered an asset making it a target of potential lawsuits and it can usually extend to cover things like libel, slander, etc. When it comes to financial security and wealth management, having this type of insurance is a critical component.

How Exactly Does Umbrella Insurance Work?

Essentially, it works in two main ways.

- First, it can extend the coverage of your existing standard policies. In other words, if a claim is filed against you that exceeded your standard liability limits, umbrella insurance kicks in after your other policies are exhausted. It serves as that secondary layer of protection.

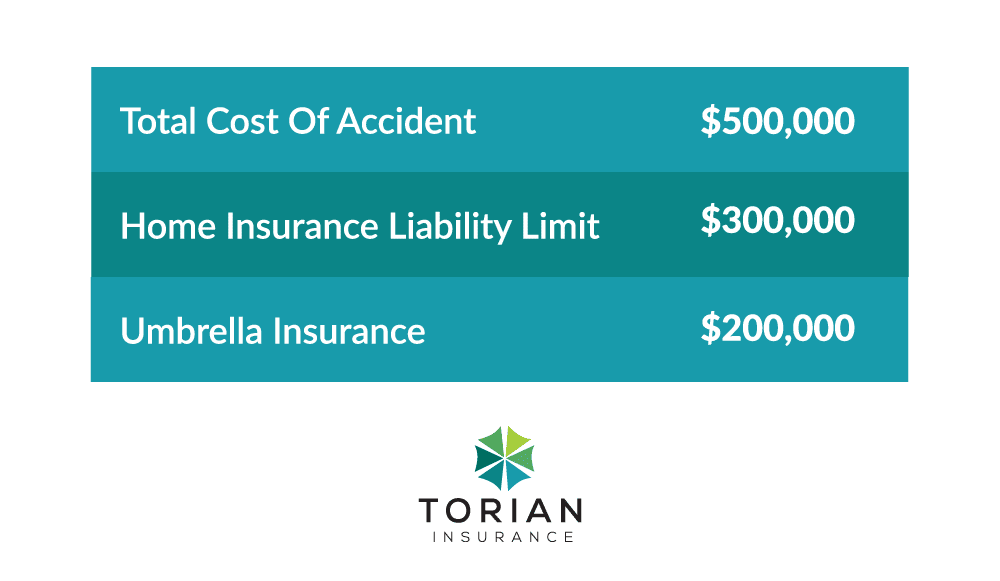

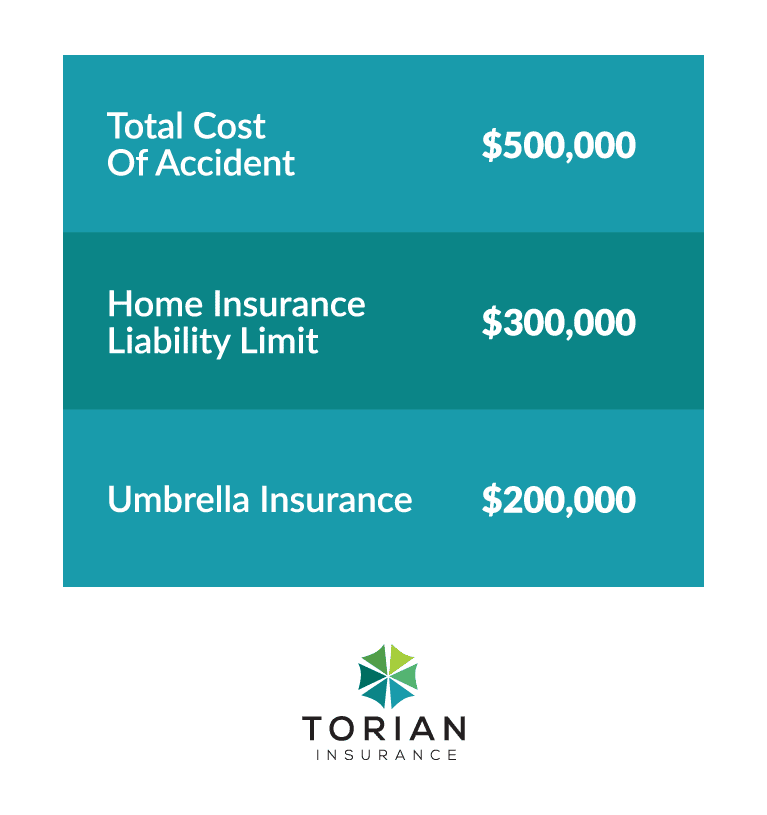

For example, imagine if your homeowner’s insurance has a personal liability limit of $300,000. You throw a big party and someone slips and falls down your stairs and is seriously injured. Their claim against you for their medical bills, pain and suffering, and lost wages comes out to a total of $500,000. That totals to $200,000 over your standard personal liability limit. That’s when your umbrella insurance would kick in.

Another scenario would be if your auto insurance has a liability limit of $200,000. Let’s say your teenage driver runs a red light and is involved in a multi-vehicle accident and is found liable. The property damages to the other vehicles adds up to $30,000 and the medical costs of the injured totals $250,000. Plus the other drivers sue you for $50,000 for their lost earnings because they are unable to work due to their injuries. Now you are on the hook for $330,000 but your standard policy only covers $200,000. Fortunately, your umbrella insurance would cover the remaining $130,000.

- Secondly, it can protect you against some claims that your standard policies exclude. This may vary depending on your policy and carrier. Think about this scenario: you are a well known figure in the community and you write a negative review about a restaurant and its owners on your Facebook page. The restaurant sues you for libel, but you are protected by umbrella insurance. Some policies may even cover legal/defense fees.

What Does Personal Umbrella Insurance Cover?

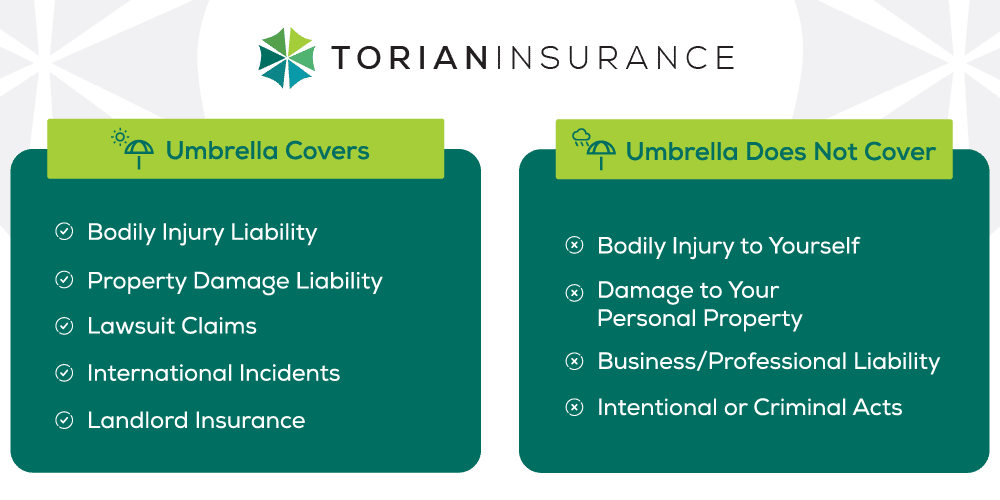

It extends the coverage that standard policies provide. Generally, it covers costs associated with:

- Bodily Injury Liability– injuries sustained by another person due to an accident. Examples of bodily injury liability claims that you may be held liable for include:

- If your dog escapes and bites someone

- If someone slips and falls on your property and is injured

- You accidentally injure someone else

- Your teenager is in a car accident in which several people are injured

- Property Damage Liability– damage or loss of someone else’s physical property. Examples include the costs of claims related to damages caused by:

- A car accident in which the other person’s vehicle is damaged

- Boating accident in which other watercrafts are seriously damaged

- You drive your car into a building and the building is damaged

- You’re house sitting and you accidentally flood the bathroom with a dripping sink

- Lawsuit claims like libel, slander, defamation of character & invasion of privacy

- Libel-a published false statement that is damaging to a person’s reputation; a written defamation.

- Slander-false spoken statement damaging to a person’s reputation.

- Defamation of Character- false statements made that hurt the reputation of one’s character

- Invasion of Privacy- intrusion on someone’s personal life without consent

- International Incidents-If you are held liable for something that happens overseas.

- Landlord Insurance– If you are sued by a tenant for more than your standard landlord insurance limit.

What Does Umbrella Insurance Not Cover?

It’s important to remember that your personal umbrella insurance doesn’t cover every single thing. It typically follows the same exclusions in your primary policies and does not cover anything outside of that. For example, with a personal umbrella insurance policy, damages to your own personal property or own injuries aren’t usually covered. It also will not cover intentional or criminal actions.

Losses/claims related to your business are also not covered by your personal umbrella insurance. A separate commercial umbrella insurance policy will need to be purchased for your business.

Other Types of Insurance to Consider

Having this additional coverage protects you from a lot, but it doesn’t cover everything as mentioned before. To cover yourself from other risks you might need to look into other types of insurance. Here are a few scenarios that you would need an additional type of insurance:

- You are driving home on your motorcycle and wreck it. You need Motorcycle Insurance.

- Your cat needs surgery. You need Pet Insurance.

- A tornado damages your business. You need Business Property Insurance.

How Do I Know If Umbrella Insurance Is Right For Me?

There are a few things that may indicate that you have a greater need for this coverage.

1. You Have Greater Risk Of Lawsuit

If any of the following apply to you, it might be time to talk to an insurance agent about adding umbrella insurance.

Some examples are you:

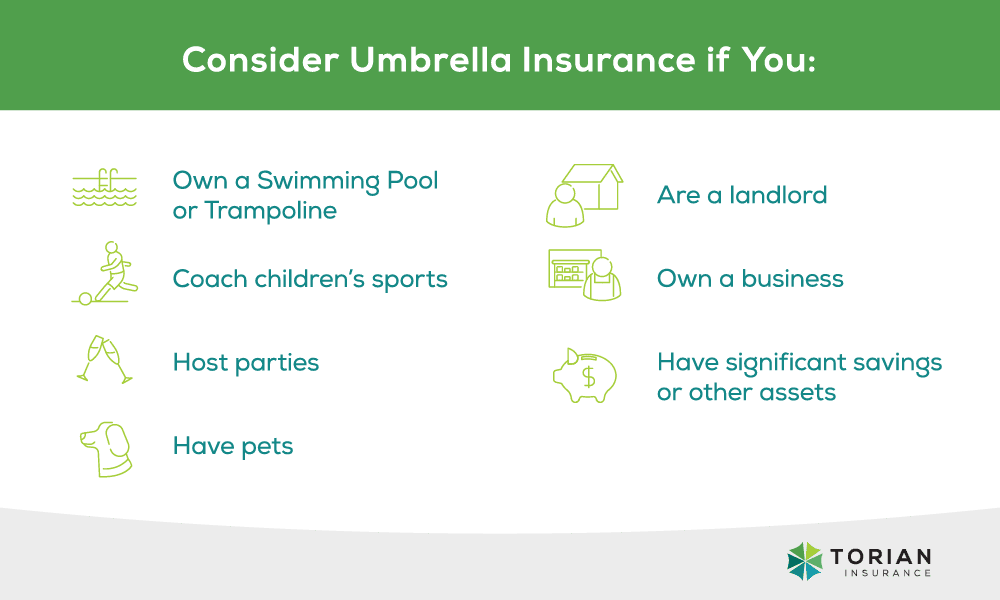

- Own a swimming pool

- Have a teenage driver

- Host parties

- Own a trampoline

- Coach a children’s sport team

- Serve on a nonprofit board

- Have pets (some breeds might put you more at risk)

- Own ATVs/ Golf Carts

- Are a landlord

2. You Have A High Networth

Generally, the more assets you have, the more protection you need. If people generally are aware of your high net worth, it also makes you and your wealth a target for lawsuits. Some indicators that you should consider umbrella insurance are if you:

- Own property/especially investment property

- Own a business

- Have significant savings or other assets

- Are a well known public figure

The general rule of thumb is if your net worth exceeds your liability coverage limits then you need umbrella insurance. Net worth is calculated simply by the total of assets you own minus all of your liabilities. For example if your net worth was $800,000 but all of your liability limits totaled $600,000, you should look into purchasing umbrella insurance.

Remember, while anyone can purchase umbrella insurance you do have to have underlying policies first as umbrella insurance can’t stand alone. Typically you have to carry the maximum coverage with your standard policies before you add umbrella insurance.

What Are The Benefits Of Umbrella Insurance?

Umbrella insurance can provide important financial protection in a number of situations. You can’t control the future or prevent accidents from happening but you can guarantee that your wealth is protected. Lawsuits are common and costly and can happen to anyone, even if you haven’t done anything wrong. That’s why umbrella insurance is so important.

Umbrella insurance is so beneficial because you can:

- Protect your assets and minimize your liability

- Have peace of mind knowing you are covered

- Meet your unique needs with customizable policies

- Save time & energy when you work with experienced insurance agents

Watch the informative video below to learn more about the benefits of umbrella insurance:

How Much Does Umbrella Insurance Cost?

Typically umbrella insurance policies are very affordable, especially compared to other types of insurance. Considering the devastating costs that can be caused by unforeseen accidents, most would argue that umbrella insurance is always worth the small cost.

According to an ACE Private Risk Services report, the average cost of umbrella insurance is only $383 a year for $1 million of coverage. Here in the Southern Indiana area a personal umbrella policy is more frequently less than $200 for $1 million of coverage. Premiums are usually lower for umbrella insurance because the risk of a claim being filed against your umbrella policy is lower than your base home or auto policy. For example if a claim is filed your standard policies are exhausted first. Keep in mind that it is also often cheaper to purchase multiple policies from the same insurance agency.

What Affects The Cost of Umbrella Insurance?

The cost of umbrella insurance varies based on how much coverage you choose to buy. Generally, policies can range from $1 million of coverage to $10 million of coverage. Other factors that play a part in the cost of umbrella insurance are:

- Your location/where you live

- Your credit history

- Your driving record

- Number of vehicles and ages of the drivers

- Number of “toys” you have such as ATV’s, watercraft, etc.

- Having rental properties

- Your level of risk

Considerations When Purchasing Umbrella Insurance

- How much liability insurance do I have with my current insurance policies?

Umbrella insurance provides additional coverage above and beyond your existing liability limits. If you don’t have enough liability coverage already, you may want to consider purchasing a policy with higher limits. - How much risk am I willing to take?

Umbrella insurance can provide peace of mind in the event that you are sued for a large amount of money. However, it is important to remember that umbrella policies do not cover every type of risk. Make sure you understand the risks covered by your policy before purchasing it. - What is the total of all my assets?

Your assets include things such as your home, other properties you own, vehicles, retirement accounts, savings, etc. Make sure you have enough coverage to protect these assets in the case of a lawsuit. - What are the potential losses of future income?

Your future income can be at risk in a lawsuit. When you are considering if umbrella insurance is right for you, don’t just think about your current income but also your future potential income. For example, if you are in law school currently, you need to protect your future earnings potential.

How Do I Get Umbrella Insurance?

If you do not have existing home and auto policies then you need to start there. Finding a trustworthy and experienced insurance agency to help you find the best coverage is important.

Once you have the minimum liability coverage required in your regular base policies, then you can talk to your insurance provider about adding umbrella insurance. People who have renters insurance are also usually eligible for umbrella insurance.

Since your financial situation is always changing, it is important to continuously review your policies and ensure you have enough coverage. For example, as your net worth grows, your coverage should also increase to protect your assets and wealth.

Anyone who is looking for extra peace of mind and protection can benefit from umbrella insurance. Torian Insurance offers customizable policies for every type of lifestyle and will help you identify your needs and how much coverage you need. Contact Torian Insurance today to get a quote to protect your commercial property from damages or liabilities now.