Planning your wedding is one of life’s most joyful experiences—but it can also be a source of worry when it comes to navigating complex requirements like Certificates of Insurance (COI). Imagine focusing on your dream celebration, only to be sidetracked by insurance jargon and strict venue demands. What if securing the right Certificate of Insurance (COI) could remove that looming worry, letting you enjoy your day to the fullest? This guide makes wedding venue insurance simple. You’ll learn what COI requirements mean in plain English, walk through a compliance checklist, and see exactly what 12 popular Evansville venues expect—from specific liability limits to submission deadlines. Whether your venue is a grand hall or an intimate outdoor setting in Evansville, understanding these details can make all the difference.

Why Do Wedding Venues Require a COI: What Are They Protecting Against?

Venues request a Certificate of Insurance to help manage potential financial and legal risks. Even if the venue already holds its own coverage, a COI from you provides an extra layer of security, ensuring that liability issues are managed promptly should an incident occur during your celebration.

The Three Main Risks Covered by a COI

- Guest Injuries: Accidents like slips or falls can happen unexpectedly. Adequate insurance covers medical expenses and legal claims related to these mishaps.

- Property Damage: Weddings involve decorations, lighting, and heavy foot traffic, any of which might accidentally damage the venue’s property. Insurance can help cover repair or replacement costs.

- Alcohol-Related Incidents: When alcohol is served, incidents related to intoxication may occur. Specific coverages—such as host liquor liability—help protect you if claims arise from alcohol-related issues.

Venues typically require that they be listed as an “Additional Insured” on your COI. This extension of coverage helps ensure that both you and your venue share in any protection needed if a claim is made.

Key Insurance Terms in Venue Contracts: What They Mean in Plain English

Understanding insurance terminology doesn’t have to be complicated. Here are some key concepts explained in everyday language. And an Insurance Agency Evansville can help clarify these terms.

Certificate of Insurance (COI) vs. Proof of Insurance

A Certificate of Insurance is a formal, regulated document verifying your insurance coverage, including limits, dates, and other critical details. Unlike a simple proof of insurance, a COI meets the specific contractual requirements that many venues demand.

Additional Insured: Extra Coverage for the Venue

By naming the venue as an Additional Insured, you extend your coverage to include the venue. This means that if an incident occurs, your policy can help protect the venue from related financial losses.

Primary & Noncontributory: Your Policy Pays First

This term means your policy serves as the primary source of coverage, addressing any claims before any other insurance (like the venue’s) is involved. This ensures that your policy is the first to pay in case of a loss.

Waiver of Subrogation: Avoiding Reimbursement Disputes

A waiver of subrogation prevents your insurer from seeking reimbursement from the venue if they pay out a claim. This helps avoid potential disputes between you, your venue, and the insurance companies.

Host Liquor Liability vs. Liquor Liability

- Host Liquor Liability: Covers incidents when alcohol is provided at your event, though not sold.

- Liquor Liability: Generally applies when alcohol is sold or provided by a third-party vendor. Be sure to check your venue’s contract to see which type is required.

Policy Limits

Many wedding venues require a minimum amount of liability coverage per occurrence—often $1 million. Some venues may have higher requirements or request additional endorsements for comprehensive protection.

The COI Checklist—Ensuring a Hassle-Free, Compliant Wedding

Meeting your venue’s COI requirements ahead of time can prevent last-minute delays and compliance issues. Use this checklist as a practical guide.

Event Liability Coverage

- Ensure your policy covers bodily injury and property damage, typically with liability limits that meet your venue’s standards.

- Check if extra umbrella coverage is suggested for additional protection.

- If you are also looking to protect your personal property while hosting events, you may want to explore Personal Insurance options.

Host Liquor Liability

- If alcohol will be served, verify that your policy includes appropriate host liquor liability coverage.

- Confirm whether the venue requires any additional endorsements or separate insurance provisions.

- For business-related weddings or corporate events, Commercial Insurance coverage might also be pertinent.

Accurate Names, Addresses, and Additional Insureds

- Double-check that the COI accurately lists the venue’s legal name and address.

- Errors in these details can lead to a rejected COI and delay your event setup.

Comprehensive Date Coverage

- Make sure your policy covers all event dates—not just the wedding day. This can include setup, rehearsal, the main event, and teardown.

- Verify the dates with your venue to avoid any gaps in coverage.

Submission Deadlines

- Venues may require that your COI be submitted well in advance—often a few weeks before the event. Plan ahead to accommodate any needed adjustments.

Recipient Details

- Identify who at the venue should receive the COI—commonly an event coordinator or property manager.

- If multiple venues are involved, prepare separate COI copies for each location.

Evansville Wedding Venue Insurance Requirements: What Each Venue Expects

Every wedding venue in Evansville handles insurance differently. Some publish detailed COI specifications upfront; others share requirements only after you sign a contract. Below is a quick breakdown of what’s publicly known for 12 of the most popular local venues—so you can plan ahead, avoid surprises, and secure the right coverage before your deadline.

Important: Venue requirements can change at any time. Before purchasing a policy, confirm exact COI specs directly with your venue or contact Torian Insurance for a free compliance check.

Venues That Require Your Own Insurance

- Main Street Wedding and Event Venue — Requires a $1,000,000 liability policy plus host liquor liability if alcohol is served. Uniquely, two separate entities must be named as Additional Insured: Main Street Wedding and Event Venue, LLC and Near More Holdings, LLC. Multi-day bookings require coverage for both rehearsal and wedding day. Budget roughly $125/day for a policy.

- Old Post Office Event Center — Event insurance is required for all bookings, no exceptions. A security officer is also required when alcohol is served. Specific liability limits and endorsements are provided during contracting—ask for these details early.

- Venue 812 — Insurance is required for all weddings. Specific limits and endorsements are shared during the contract process. The venue offers in-house catering and bar service through Acropolis Catering.

- Vanderburgh 4-H Center — Insurance is mandatory, and this is the only Evansville venue to publish a specific deadline: COI must be submitted 14 days before your event. A copy of your alcohol permit is also due at the same time. Specific liability limits are provided in the lease packet.

Venues Where Coverage May Be Included

- The Bauerhaus — Liability insurance is listed as an included amenity on wedding platforms. This all-inclusive venue handles catering, bar, coordinator, entertainment, and logistics in-house. Confirm whether you still need a separate policy for your specific booking.

- Evansville Country Club — Liability insurance is listed as an included amenity on WeddingWire. All alcohol must be provided by the club. Confirm whether the club’s coverage extends to your event or if a separate COI is expected.

- CityView at Sterling Square — The only Evansville venue that publicly states insurance is recommended but not required. All beverages must go through CityView, and security is required for events with alcohol. Even so, carrying your own policy is strongly advised—a single guest injury can far exceed the $125–$300 cost of coverage.

- COMFORT by the Cross-Eyed Cricket — No insurance requirements are published online. This fully all-inclusive venue handles catering, bar, security, DJ, décor, and coordination in-house, which may mean their own commercial policy covers most scenarios. Contact Events@comfortevv.com to confirm.

Government & Public Venues

- O’Day Discovery Lodge at Burdette Park — County-operated; insurance requirements are provided in the rental agreement. Key detail: a Vanderburgh County Sheriff’s Deputy is required whenever alcohol is served. No open flames permitted, and the park closes at midnight. Expect the county or Board of Commissioners to be named as Additional Insured.

- Old Vanderburgh County Courthouse — County-operated historic landmark; insurance is listed as a feature on The Knot but specifics come during the rental process. A paid security guard is required for all events. Open vendor policy. Expect Vanderburgh County to be named as Additional Insured.

- Bally’s Evansville Casino & Hotel — No COI requirements published. As a regulated gaming facility with full-service wedding packages, 24-hour security, and comprehensive commercial coverage, Bally’s may handle event liability differently than independent venues. Contact Convention Services at (812) 433-4611.

- Sweetwater Event Center — No insurance requirements published online. The venue allows outside vendors, which typically signals that event insurance is required. Contact the venue at (812) 402-3435 to confirm before booking.

What If Your Venue Isn’t Listed?

Based on Indiana wedding industry standards, most venues that require a COI will expect $1,000,000 in general liability per occurrence, the venue named as Additional Insured, host liquor liability when alcohol is served, and submission 14–30 days before your event.

Don’t Navigate This Alone

Every venue on this list has its own nuances—from Main Street’s dual-entity naming requirement to Burdette Park’s mandatory sheriff’s deputy. Torian Insurance specializes in wedding and event insurance for Evansville-area couples. Our independent agents will review your venue contract, confirm exact COI requirements, and deliver a compliant certificate—typically within one to two business days.

Special Cases—Parks, Public Buildings, and Historic Venues

Public parks, municipal buildings, and historic sites typically carry stricter insurance requirements than privately owned venues. You may encounter higher liability limits, additional documentation such as special permits, mandatory security when alcohol is served, and restrictions on decorations, open flames, or setup methods to protect the property. Government-operated venues will almost always require the governmental entity — such as a county board of commissioners — to be named as Additional Insured on your COI. If you’re planning an event at one of these locations, check the venue profiles above for Evansville-specific examples including O’Day Discovery Lodge at Burdette Park and the Old Vanderburgh County Courthouse, and contact the venue early to confirm their full requirements. For public park permits and regulations, visit the Evansville Parks Department website.

Some unique venues require additional precautions beyond standard COI coverage. In Evansville, public parks, municipal buildings, and historic sites may have more rigorous or specific requirements.

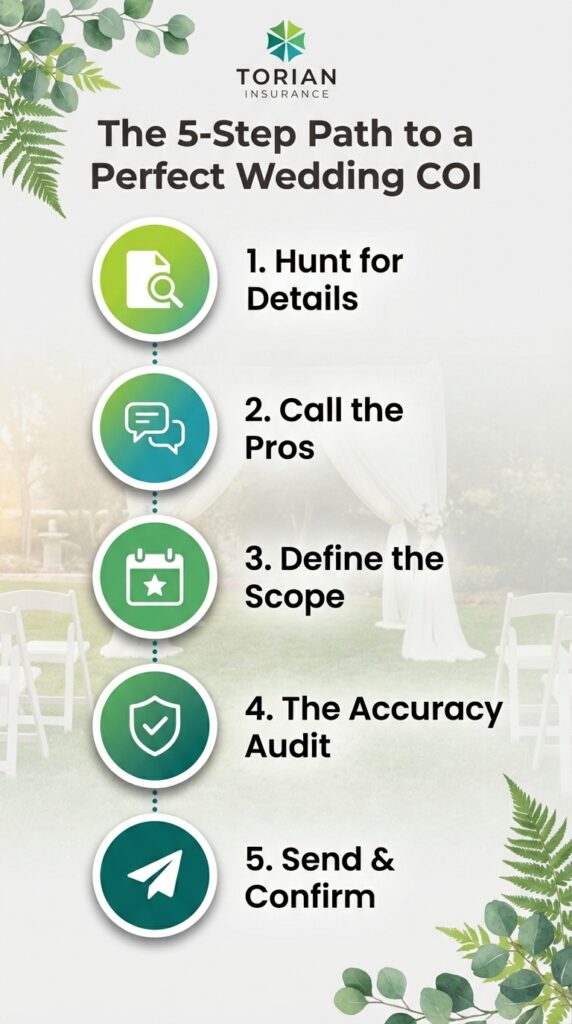

How to Get Your Wedding Venue COI Quickly

Securing a valid COI need not be stressful. Follow these streamlined steps to enjoy peace of mind as your big day approaches.

Step-by-Step Process

- Review Your Venue Contract: Read through your insurance requirements carefully. Note down critical details including coverage limits, required endorsements, and submission deadlines.

- Consult an Insurance Agent: Share your contract specifications with an independent insurance agent who is experienced in event insurance. This professional can help tailor a policy that meets your venue’s requirements.

- Provide Detailed Event Information: Clearly communicate specifics such as event dates, expected guest count, alcohol service arrangements, and any special conditions at the venue. This ensures the policy aligns accurately with your event details.

- Verify the Issued COI: Once you receive it, review the COI for accuracy:

- Confirm the venue’s name and address.

- Check coverage dates.

- Ensure required endorsements are included.

- Confirm compliance with the venue’s standards before submission.

- Submit the COI Early: To avoid last-minute issues, deliver the COI well in advance of the deadline. Follow up with your venue to confirm receipt.

Instant COI Services: Pros and Cons

While some online platforms allow for rapid issuance of a COI, they might not always address the detailed requirements—such as specific endorsements or ensuring the correct Additional Insured designation—that certain venues demand. For complex cases or unique contractual terms, consulting a specialized insurance agent, like Torian Insurance, remains the best approach.

Common COI Requirement Traps and How to Avoid Them

Even with careful planning, some challenges may arise when arranging your wedding insurance. Recognizing these pitfalls early can save you time and stress.

Liquor Liability Gaps

- Ensure that your policy clearly addresses alcohol-related incidents.

- Verify that it includes the right type of liquor liability—whether for host-provided alcohol or vendor-supplied drinks.

- Refer to the Indiana Alcohol & Tobacco Commission guidelines for more details on legal alcohol service requirements.

Incorrect Additional Insured Naming

- Confirm that you have the venue’s exact legal name as stated in your contract.

- Discrepancies in naming or other details can result in the rejection of your COI.

Inadequate Coverage for Extended Event Dates

- Do not assume your policy automatically covers related event days such as rehearsal, setup, or teardown—confirm explicitly.

- Make sure every phase of your event is covered to prevent any gaps in protection.

Overreliance on Vendor Coverage

- While vendors may have their own insurance, ensure that your COI provides sufficient direct protection.

- Double-check that vendor policies do not leave critical aspects of your event underinsured.

Hidden Exclusions in Your Policy

- Carefully review the fine print, as some exclusions might leave you unprotected in certain scenarios.

- Discuss any ambiguities with your insurance agent before finalizing your policy.

Wedding Venue Insurance & COI FAQs

What is a Certificate of Insurance (COI) for a wedding venue?

A COI is an official document that verifies your liability insurance meets your venue’s requirements, including coverage limits, specific policy dates, and any necessary endorsements.

How much liability insurance do wedding venues typically require?

Many venues require liability limits of around $1 million per occurrence, though some may request higher limits or additional endorsements depending on the venue and event details.

Do I need to name my venue as an Additional Insured on my COI?

Yes. Listing the venue as an Additional Insured extends protection to the venue if a claim arises from your event. Your COI should also match the venue contract exactly—using the correct legal name and address—and some venues may require more than one entity (such as a property owner or management company) to be listed as an Additional Insured.

If the venue provides bartenders, do I still need host liquor liability coverage?

Often, yes. Even if the venue supplies bartenders, host liquor liability coverage can still be required to protect you against alcohol-related incidents during your event, depending on your venue contract and how alcohol is being provided.

Should my insurance cover rehearsal and setup days?

Absolutely. Your policy should ideally cover all event-related activities—from setup and rehearsals to the main event and teardown—to prevent any gaps in coverage.

How quickly can I obtain a COI?

Working with an independent insurance agent, such as those at Torian Insurance, can often secure your COI within one to two business days, assuming all details are confirmed and accurate.

What happens if I don’t meet the COI requirements?

Failure to provide a compliant COI might lead to delays, additional fees, or even cancellation of the event. It’s vital to confirm your venue’s requirements well in advance.

Ensuring Peace of Mind on Your Wedding Day

Securing the appropriate wedding venue insurance is not only about fulfilling contractual obligations—it’s also about ensuring peace of mind on your big day. As you finalize your plans, carefully review your venue’s specific COI requirements and make sure you understand key insurance terms such as Additional Insured, Waiver of Subrogation, and Primary & Noncontributory. Use your COI checklist to confirm your coverage is complete, including any extended dates and that every detail is accurate, and stay alert for common pitfalls like inadequate liquor liability or errors in the insured information. If you’re working with a unique venue—such as a public park, historic site, or hosting a multi-day event—confirm any added conditions or higher coverage limits directly with the venue so there are no surprises.

Torian Insurance is ready to simplify the process. With customized insurance solutions and dedicated COI support, you can remove a major source of stress from your wedding planning. Get the peace of mind you deserve for your big day—request a quote and COI support today!