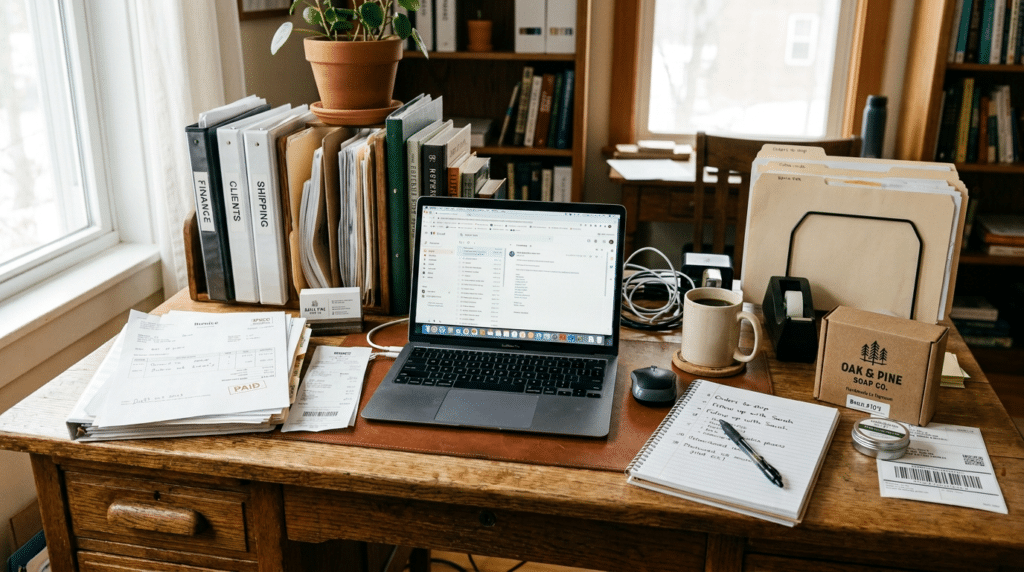

Millions of Americans are running businesses and side hustles from home — and most assume their homeowners insurance has them covered. It doesn’t. Home-based business insurance fills a critical coverage gap that standard homeowners policies were never designed to address, and knowing your options is the first step toward real protection for what you’ve built.

Key Takeaways

- A standard homeowners policy covers only $2,500 in business property on-premises — far less than most home businesses carry in computers, tools, or inventory.

- Homeowners liability coverage does not extend to business-related activities, including client injuries during a business visit to your home.

- In some cases, operating a business from home without notifying your insurer can give the carrier grounds to deny claims or void your coverage entirely.

- Three coverage options exist: a homeowners policy endorsement, an in-home business policy, and a Business Owner’s Policy (BOP) — each suited to a different scale of business activity and risk.

- Side hustlers and part-time operators need coverage too. The exposure exists whether your business is your full-time job or something you do on weekends.

- An independent agent can compare multiple carriers to find coverage that fits your specific business type, revenue level, and risk — not just the nearest available product.

Your Homeowners Policy Was Never Built for Business

Your homeowners policy is designed to protect your home and your personal belongings. It was not designed to cover a business, and most people don’t realize how narrow that coverage actually is until they try to file a claim.

- The property coverage limit: A standard homeowners policy typically caps business property coverage at $2,500 on-premises and as little as $250 to $500 for equipment you take off-site. For most home-based businesses — photographers, contractors, consultants, e-commerce sellers — that limit is gone before you account for a single laptop and camera bag. Business use is one of the most costly homeowners policy exclusions — and one of the least discussed.

- The business liability exclusion: Homeowners liability coverage doesn’t extend to business activities. If a client visits your home for a meeting and slips on your front steps, the claim will likely be denied because the visit was business-related. That’s not a technicality — it’s how the policy was written.

- The policy invalidation risk: In some cases, operating a business from home without telling your insurer can give the carrier grounds to deny unrelated claims or, in more serious situations, invalidate your homeowners coverage entirely. If you’ve started a business from home and haven’t had that conversation with your agent, that’s the first call to make.

About 78.4 million Americans freelanced in 2024 — roughly 36% of the U.S. workforce — and the number of home-based businesses continues to grow. Yet nearly 60% of in-home business owners were not properly insured, according to a widely cited Insurance Information Institute survey. The coverage gap is real, and it’s far more common than it should be.

Three Ways to Fill the Home-Based Business Insurance Gap

You don’t have to choose between running a home business and being properly protected. Three coverage options exist for home-based businesses, and the right one depends on the scale and nature of what you’re doing.

Option 1: A Homeowners Policy Endorsement

A homeowners endorsement — sometimes called a rider — is the simplest option. It extends your existing homeowners policy to include a modest amount of additional business property coverage, typically doubling the standard limit from $2,500 to $5,000. The annual cost is minimal, often between $25 and $100.

An endorsement works well if you’re running a low-revenue side hustle with limited equipment, no clients visiting your home, and no employees. It doesn’t provide meaningful liability protection for business activities, so if you have any client contact or provide professional services, you’ll likely need more.

Option 2: An In-Home Business Policy

An in-home business policy is a standalone policy designed specifically for home-based businesses. It typically covers business property at replacement value (without the tight $2,500 cap), general liability for business-related injuries or property damage, and basic loss-of-income coverage. It’s generally available for businesses with up to three employees and under $250,000 in annual revenue.

This is often the right fit for tutors, hair stylists, photographers, virtual assistants, online sellers, and other sole proprietors who work primarily from home with occasional client contact.

Option 3: A Business Owner’s Policy (BOP)

A business owner’s policy bundles commercial property insurance, general liability coverage, and typically business interruption coverage into a single package. A BOP is designed for businesses that have outgrown an in-home policy — more revenue, more equipment, greater client interaction, or employees.

If you’re running a meaningful home-based operation with consistent client work, valuable inventory or equipment, or any hired help, a BOP is worth a serious conversation. It provides broader protection and typically costs less than purchasing those coverages separately.

Which Coverage Option Is Right for Your Home-Based Business?

The right coverage depends on four things: how much revenue your business generates, what equipment or inventory you keep at home, whether clients visit your property, and whether you have any employees. Here’s a simplified framework:

- Side hustles with no client visits and minimal equipment: A homeowners endorsement is a reasonable starting point, though it won’t address business liability.

- Part-time or full-time home businesses with client contact or up to three employees: An in-home business policy typically provides the right level of protection.

- Established home businesses with significant revenue, employees, or high-value equipment: A BOP provides the broadest coverage and the flexibility to grow into it.

When in doubt, work with an independent agent who can assess your actual exposure. Annual policy reviews matter — and starting or growing a home business is exactly the kind of change that warrants one.

Coverage Most Home-Based Business Owners Overlook

Property and business liability coverage are the core of any home-based business insurance plan, but several other gaps trip up home-based operators on a regular basis.

- Commercial auto: Personal auto insurance doesn’t cover accidents that happen while driving for business purposes — that includes client visits, deliveries, and supply runs. If you use your vehicle for any business-related travel, a commercial auto insurance endorsement or separate policy is worth discussing.

- Professional liability (E&O): Consultants, coaches, designers, accountants, and anyone else who gives professional advice or performs services for clients needs professional liability insurance — also called errors and omissions (E&O) coverage. General liability policies typically don’t cover professional errors, and homeowners policies certainly don’t.

- Workers’ compensation: If you have any help — a part-time assistant, an occasional contractor — workers’ compensation coverage may be required under Indiana law. Don’t assume informal arrangements are exempt.

- Cyber liability: Freelancers, virtual assistants, online sellers, and anyone who handles client data or payment information carries real data breach exposure. Cyber liability insurance is increasingly important even for small operations, and it’s more affordable than most people expect.

How Torian Insurance Helps

At Torian Insurance, we work with home-based business owners and side hustlers across Southern Indiana, Western Kentucky, and Southeastern Illinois to figure out what they’re actually exposed to — and what coverage makes sense given how they operate. We’ve been doing this work for more than 100 years from our home in Evansville, and we know that a home-based business looks very different from a corporate account in a downtown office building.

We’re an independent agency, which means we shop multiple carriers — including Acuity, West Bend, Cincinnati Insurance, and others — rather than selling one company’s products. That gives us the flexibility to find coverage that actually fits your business: the nature of your work, your revenue level, your risk, and your budget.

We also look at the whole picture. A home-based business often has coverage needs that span home insurance, commercial property, professional liability, and commercial auto — coverage that’s easy to miss when you’re working with a single-line carrier. We can review what you have, identify what’s missing, and help you build a plan that holds together.

| “I have used Torian Insurance for personal and business insurance for over 13 years. Their responsiveness and attention to detail each time I’ve needed them shows how much they genuinely care.”— Torian Insurance client, 13-year business customer |

Frequently Asked Questions About Home-Based Business Insurance

Does homeowners insurance cover a home-based business?

No, not in any meaningful way. A standard homeowners policy caps business property coverage at $2,500 on-premises and $250 to $500 off-site, and it excludes liability for business-related activities entirely. If a client is injured at your home during a business visit, or a fire destroys your business equipment, a standard homeowners policy is unlikely to cover the full loss — and may deny the claim on business-use grounds.

What is an in-home business policy?

An in-home business policy is a standalone insurance product designed for businesses operated from a home. It typically covers business property at replacement value, general liability for business-related injuries or property damage, and some degree of business income protection. It’s generally available for businesses with up to three employees and annual revenue under $250,000 — a practical middle ground between a homeowners endorsement and a full Business Owner’s Policy.

Can running a business from home void my homeowners insurance?

In some cases, yes. Some insurers include policy provisions that allow them to deny claims or cancel coverage if the homeowner has materially changed the use of the property without disclosure. If you’ve started a business from home and haven’t told your insurer, that’s a conversation worth having before a claim gives you reason to regret it.

Is forming an LLC enough to protect my home business?

No. An LLC can provide some personal liability protection for the business owner, but it doesn’t replace insurance. An LLC won’t cover physical damage to your business equipment, injuries that occur at your home during business activity, or lost income if your business is disrupted. Business structure and insurance serve different purposes — you need both, not one or the other.

How much does home-based business insurance cost?

Costs vary by coverage type. A homeowners endorsement can run as little as $25 to $100 per year. An in-home business policy typically ranges from a few hundred dollars annually for low-risk operations. A BOP varies more widely based on industry, revenue, and coverage limits. An independent agent can pull comparative quotes from multiple carriers so you’re getting the best fit for what you actually need.

Ready to Close the Coverage Gap?

If you’re running a business or side hustle from home, the right time to review your coverage is before a claim — not after. The team at Torian Insurance can walk you through your options, compare carriers, and help you build a coverage plan that fits what you’ve built.

Have questions about your home-based business coverage? Contact Torian Insurance to talk with a local agent.