If you own a condo or live in an HOA community, your association carries a master insurance policy on the building. But HOA master policy gaps are more common than most unit owners realize — and those gaps can leave you personally on the hook for thousands of dollars when a loss occurs. Understanding what the master policy doesn’t cover is just as important as knowing what it does.

Key Takeaways

- HOA master policies come in three types — bare walls, walls-in/single entity, and all-in — and the type determines how much coverage responsibility falls on individual unit owners.

- HO-6 condo insurance policies include only $1,000 in loss assessment coverage by default. Insurance professionals recommend increasing that limit to at least $50,000.

- HOA master policy deductibles can exceed $10,000, and some buildings carry deductibles of $50,000 to $100,000 — costs that are typically passed to unit owners through loss assessments.

- Betterments and improvements you’ve made to your unit — upgraded flooring, custom cabinetry, remodeled bathrooms — are your financial responsibility regardless of the master policy type.

- Personal property is always excluded from HOA master policies. Furniture, electronics, clothing, and personal belongings require coverage under your own policy.

- The fix is straightforward: request your HOA’s master policy, identify its type, and work with an independent agent to align your personal coverage with the gaps.

What an HOA Master Policy Actually Covers

The HOA master policy covers the building as a whole — the structure, shared systems, and common areas like the roof, exterior walls, hallways, and elevators. It’s the association’s policy, funded through HOA dues, and it protects the asset the association collectively owns.

What it is not designed to do is protect individual unit owners from every risk inside their own space. The coverage it provides — and the coverage it leaves out — depends almost entirely on which type of master policy your HOA carries. Most unit owners have no idea which type applies to them.

The Three Types of HOA Master Policies — And Why the Difference Matters

Knowing your HOA’s policy type is the single most important step in understanding your own coverage needs. Each type draws a different line between what the HOA covers and what falls on you as the unit owner:

Bare Walls Coverage

A bare walls policy covers only the building’s structure — the studs, concrete, insulation, and wiring inside the walls. Everything attached to the interior — fixtures, flooring, cabinetry, appliances — is your responsibility. This is common in large condo associations and creates the largest coverage burden for individual owners.

Walls-In / Single Entity Coverage

A walls-in (also called single entity) policy extends further. It covers the original standard fixtures and finishes that were in place when the unit was built — base-model appliances, standard flooring, original cabinetry. But it does not cover upgrades or improvements made since purchase. If you replaced laminate floors with hardwood, you own that exposure.

All-In Coverage

An all-in policy is the most comprehensive option. It covers original fixtures, standard finishes, and improvements made to the unit. Even so, all-in policies do not cover personal property — and the master policy deductible is still passed to unit owners when a covered loss occurs. The Colorado Division of Insurance HOA Insurance Toolkit provides a useful reference for understanding all three policy type definitions.

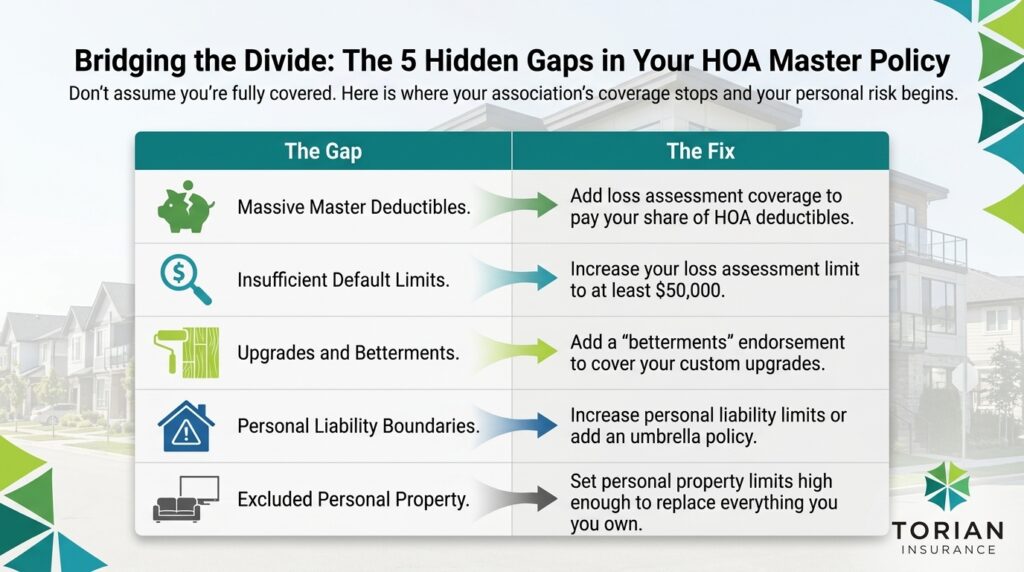

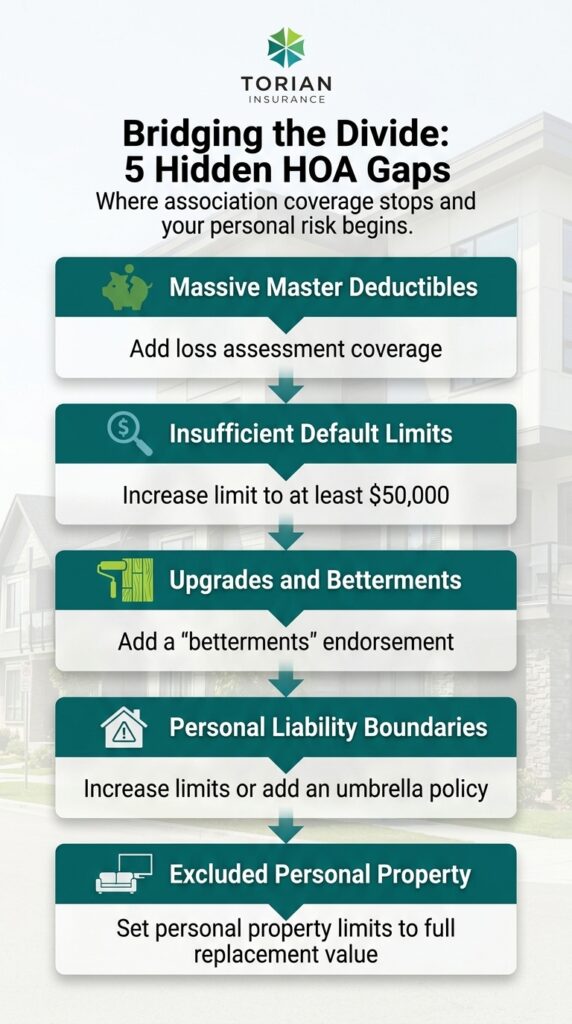

The Five Most Common HOA Master Policy Gaps

The most common HOA master policy gaps are: the deductible passed to unit owners through loss assessments, loss assessment coverage limits that are too low by default, betterments and improvements you’ve made to your unit, personal liability inside your own space, and personal property — which no master policy covers. Each one represents a scenario where you may believe you’re protected when you aren’t.

1. The Deductible Gap

When a covered loss occurs — a fire, a burst pipe, a severe storm — the HOA’s master policy pays after the deductible is met. That deductible isn’t absorbed by a central fund. It’s typically assessed to unit owners, either those directly involved in the loss or all owners in the building, depending on the HOA’s governing documents.

HOA master policy deductibles exceeding $10,000 are not uncommon, and some buildings carry deductibles as high as $50,000 to $100,000. In a 50-unit building with a $100,000 master policy deductible, each owner’s share of the assessment could reach $2,000 — before factoring in any gap between the actual loss amount and the policy limit.

2. Loss Assessment Coverage That’s Too Low by Default

Loss assessment coverage is an endorsement on your HO-6 or homeowners policy that reimburses you for your share of any loss assessment the HOA passes to unit owners. The problem: standard HO-6 policies include only $1,000 in loss assessment coverage by default. Insurance professionals recommend carrying at least $50,000.

A standard HO-6 policy is one of the more affordable personal insurance products available — and increasing the loss assessment limit typically adds only a modest amount to that premium. Increasing the loss assessment limit typically adds only a modest amount to that premium — a small cost compared to a five-figure out-of-pocket assessment.

It’s also worth knowing that HOA boards can assess current unit owners for losses that predate their ownership — meaning you could receive a bill for an incident that happened before you ever moved in. Given that assessments can easily reach five figures per unit, the standard $1,000 default limit leaves most owners significantly underprotected.

3. Betterments and Improvements You’ve Made to the Unit

If you’ve upgraded your unit — new flooring, a remodeled bathroom, custom built-ins — those improvements are considered betterments. Under a bare walls policy, they were always your responsibility. Under a walls-in policy, any upgrades beyond original standard finishes are excluded. Your HO-6 policy can include a betterments and improvements endorsement to protect that investment.

4. Liability Gaps When Coverage Runs Out

The HOA’s master policy includes liability coverage for incidents in common areas, but it doesn’t extend to personal liability inside your unit. If a guest is injured in your home, that’s your personal exposure — not the association’s.

If a significant incident exhausts the master policy’s liability limit, individual unit owners may face additional exposure beyond what the HOA policy covers. An umbrella insurance policy provides an extra layer of liability protection that works alongside your HO-6 or homeowners policy — often at a lower annual cost than most owners expect.

5. Personal Property — Always Excluded

No master policy type covers personal property inside individual units. Coverage for furniture, electronics, clothing, appliances, and personal belongings must come from your own HO-6 or homeowners policy, regardless of what the master policy covers structurally.

If you own high-value items — jewelry, collectibles, musical instruments — a standard personal property limit may not be sufficient. Ask your agent whether a valuable items endorsement makes sense for your situation.

What About Renters and Single-Family HOA Homeowners?

HOA master policy gaps aren’t just a condo owner issue. Renters and single-family homeowners in HOA communities face their own version of the same problem: assuming the association’s policy covers more than it does.

Renters in HOA Communities

If you rent a condo or home within an HOA community, you don’t have an ownership stake in the building — but you still have personal property and personal liability exposure the master policy doesn’t touch. A renters insurance policy fills that gap at a cost most renters find surprisingly affordable.

Single-Family Homeowners in HOA Communities

If you own a single-family home in an HOA-governed neighborhood, the association’s master policy typically covers common areas only — not individual homes. Your home is your responsibility under your own homeowners policy. The most relevant gap for single-family HOA owners is loss assessment coverage. Your existing policy may include it, but verifying the limit is worth a quick review.

How to Find Out Where Your Coverage Stands

Taking action starts with three steps:

- Request your HOA’s master policy. Ask your board or property manager for the declarations page and full policy documents. The policy type — bare walls, walls-in, or all-in — will be stated in the language. HOA boards are required to provide this.

- Note the deductible. Find the master policy deductible and write it down. This is the number that drives your loss assessment exposure.

- Compare it to your own policy. Review your HO-6 or homeowners policy alongside the master policy. Check your loss assessment limit, betterments coverage, personal property limit, and personal liability coverage. An independent agent can review both policies side by side and identify where your coverage needs to close a gap.

How Torian Insurance Helps

As an independent insurance agency, Torian Insurance shops multiple carriers — including Acuity, Chubb, Cincinnati Insurance, Hanover, and others — to find a condo or homeowners policy that coordinates with your HOA’s master policy. That means reviewing both policies together, identifying the specific gaps, and recommending coverage options that actually close them.

If you’re not sure what type of master policy your HOA carries, or you’ve never compared your personal policy against it, that’s exactly the kind of review Torian’s agents do. Founded in 1923 and Evansville’s largest locally owned independent insurance agency, Torian brings more than 100 years of experience serving homeowners, condo owners, and renters across Indiana, Kentucky, and Illinois.

Most people don’t find their coverage gaps until after a claim. A coverage review before a loss costs nothing — and can prevent a very expensive surprise.

“Torian provides a fantastic service for their customers. They help us find the perfect fit for our family’s needs, even as our family has grown and our needs have changed over the last 10+ years.”

— Torian Client, 10+ Year Customer

Frequently Asked Questions About HOA Master Policy Gaps

Does my HOA’s master policy cover my personal belongings?

No. HOA master policies cover the building structure and common areas — not personal property inside individual units. Regardless of whether your HOA carries a bare walls, walls-in, or all-in policy, furniture, electronics, clothing, and personal belongings must be covered under your own HO-6 or homeowners policy.

Who pays the HOA master policy deductible when there’s a claim?

The deductible is typically assessed to unit owners through a loss assessment — either to those directly involved in the loss or to all owners in the building, depending on the HOA’s governing documents. With HOA deductibles that can range from a few thousand dollars to $50,000 or more, the loss assessment limit on your personal policy matters significantly.

What is loss assessment coverage and how much do I need?

Loss assessment coverage is an endorsement on your HO-6 or homeowners policy that reimburses you for your share of an HOA-issued assessment. Standard policies include only $1,000 by default — well below what insurance professionals recommend. Given how high HOA deductibles have risen, carrying at least $50,000 in loss assessment coverage is the standard guidance.

Do I need condo insurance if my HOA already has a master policy?

Yes. Even with an all-in master policy, you still need your own HO-6 condo policy to cover personal property, personal liability, betterments, loss assessment exposure, and additional living expenses if a covered event makes your unit temporarily uninhabitable. Lenders originating Fannie Mae-backed mortgages also require evidence of an individual unit insurance policy in many condo situations.

How do I find out what type of master policy my HOA has?

Request the declarations page and policy documents from your HOA board or property management company. Look for language identifying the policy as bare walls, walls-in (or single entity), or all-in. If the language isn’t clear, bring the policy to an independent insurance agent who can interpret it and identify where your personal coverage needs to pick up.

Don’t Wait for a Loss Assessment to Find Out What You’re Missing

Most unit owners discover coverage gaps after a claim — not before. The good news is that coordinating your HO-6 or homeowners policy with your HOA’s master policy is a straightforward process with the right agent guiding the way. Contact Torian Insurance to talk with a local agent and make sure your coverage actually protects what the master policy leaves behind.