A general contractor just emailed you the subcontract for a new project, and one line stops you cold: builders risk insurance is required before work starts. This guide explains what builders risk insurance Indiana contractors need, what it covers, what it doesn’t, when it starts and ends, and the contract traps worth catching before you sign.

Key Takeaways

- Builders risk insurance covers a structure during construction or renovation. Coverage typically ends at occupancy, when the building moves to a permanent commercial or homeowners property policy.

- The construction contract decides whether the owner, general contractor, or subcontractor carries the policy. The insurance company doesn’t make that call; the contract does.

- Standard builders risk policies do not cover faulty workmanship, employee theft, contractor-owned tools, or losses tied to project delay unless specific endorsements are added.

- Coverage often starts when materials first arrive on site and ends at the earliest of substantial completion, occupancy, or a stated post-completion window of often 90 days.

- Cost depends on project value, project type, location, length of construction, and which optional endorsements are added. There is no flat rate.

- A certificate of insurance does not prove the right coverage is in place. The construction contract language is what the policy actually has to match.

What Is Builders Risk Insurance?

Builders risk insurance is a property policy that covers a building or structure during construction or renovation. It pays for direct physical loss to the project, including the structure, materials on site, and materials in transit, from causes like fire, wind, hail, theft, vandalism, and water damage. The policy is sometimes called “course of construction” insurance, and the two terms refer to the same coverage.

Three parties typically have an insurable interest in a construction project: the property owner, the general contractor, and lenders or investors. The construction contract decides who buys the policy. On large commercial projects, the owner often carries it; on smaller commercial and residential jobs, the general contractor or a specialty subcontractor may be required to.

What Builders Risk Insurance Covers

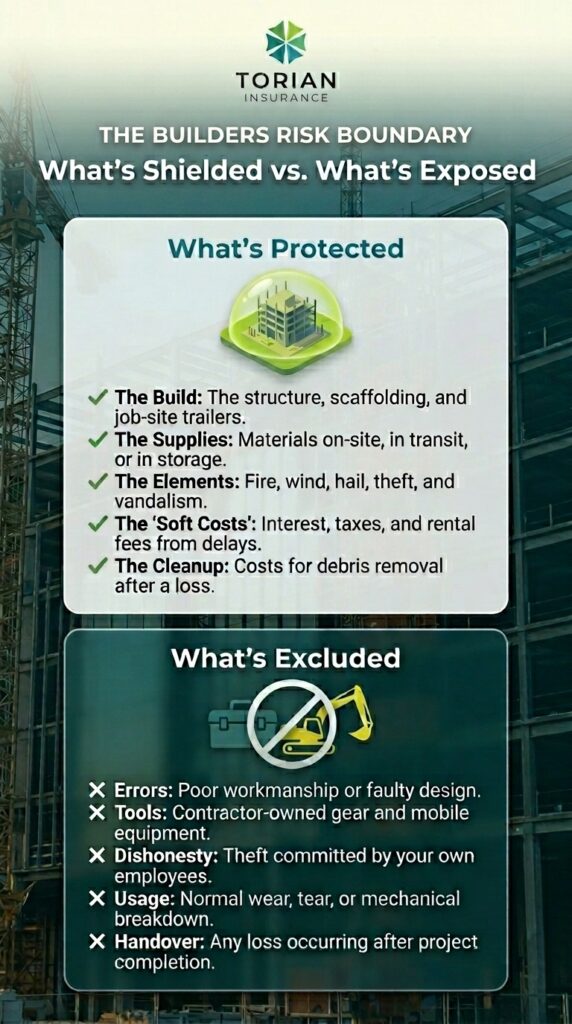

Builders risk insurance covers direct physical loss to the structure being built, including the building itself, materials and supplies stored on site, materials in transit, and temporary structures like scaffolding and job-site trailers. Coverage applies to losses from fire, lightning, wind, hail, theft, vandalism, and water damage, with both named-peril and all-risk versions available.

A few coverages contractors often miss:

- Soft costs: Economic losses tied to a covered project delay, including construction-loan interest, equipment rental, and real estate taxes. Standard property insurance typically excludes these losses, so they require a specific endorsement.

- Materials in transit and at temporary storage: Coverage is usually included; the limit is worth confirming.

- Debris removal: Most policies include a sublimit. Larger projects may need a higher one.

- Flood and earthquake: Often excluded or sublimited rather than included by default. Indiana sees flood exposure along the Ohio and Wabash rivers and severe storm damage statewide. Verify what’s actually scheduled on the policy.

What Builders Risk Insurance Does Not Cover

Standard builders risk policies exclude five common loss types: faulty workmanship or design, employee theft, contractor-owned tools and equipment, post-occupancy losses, and ordinary wear and tear.

- Faulty workmanship, design, or materials: Builders risk generally won’t pay if the project fails because of bad design or workmanship. Some policies offer a “resulting damage” carve-out for downstream damage, but the faulty work itself is excluded.

- Employee theft: Excluded under builders risk. Fidelity or commercial crime coverage handles this exposure.

- Tools and equipment in the contractor’s possession: Hand tools, power tools, mobile equipment, and vehicles fall under inland marine contractors insurance, the standard companion coverage on a working job site.

- Post-occupancy losses: Once the building is occupied or substantially complete, builders risk ends. Continuing coverage requires a permanent property policy.

- Ordinary wear and tear, mechanical breakdown, and intentional damage: Standard exclusions on virtually all property policies.

When Coverage Starts and When It Ends

Builders risk coverage typically starts when materials first arrive on site or construction first begins, and ends at the earliest of substantial completion, occupancy, or a stated post-completion period of often 90 days. The policy or contract specifies which start and end triggers apply.

The three end triggers, in order of how often they apply:

- Substantial completion: The project is finished enough to be used for its intended purpose.

- Occupancy: The owner or tenant takes possession, even if punch-list items remain.

- A stated post-completion period: Often 90 days, designed to bridge the gap to a permanent property policy.

The endings cause most disputes. A house may be substantially complete when the certificate of occupancy is issued, but punch-list items can take weeks. If a fire breaks out during that period, who pays depends on which trigger ended the policy. Most policies allow extension if a project runs long, but the request must be made before the original term expires.

Builders Risk vs. Commercial Property and General Liability Insurance

Builders risk insurance is often confused with two other coverages contractors carry. Each covers a different exposure, and an active project typically needs all three:

| Coverage | What It Protects | When It Applies |

| Builders risk | The structure during construction, plus materials on site and in transit | From construction start through substantial completion |

| Commercial property | A finished building owned or leased by the business (see commercial property insurance) | After occupancy and on an ongoing basis |

| General liability | Third-party bodily injury or property damage caused by the contractor’s work (see general liability insurance) | Continuously, across all projects |

A contractor on an active job typically carries builders risk, general liability, inland marine, and workers’ compensation. Our overview of essential contractor insurance policies walks through the full coverage stack.

What Affects Builders Risk Insurance Cost in Indiana

Builders risk insurance cost depends on several project-specific factors, and there is no flat rate. Policies come in two structural forms: a reporting form, where premium adjusts periodically based on actual project value, and a completed-value form, where premium is set up front based on projected final value. Most residential and smaller commercial projects use the completed-value form.

The biggest cost drivers:

- Project value: Total insured value of the completed structure is the foundation of the premium calculation.

- Project type: Wood-frame residential typically costs less than steel-frame commercial. Renovation often costs more than new construction because of existing-structure exposure.

- Project location: Distance to fire protection and exposure to weather hazards both affect rate. Indiana’s tornado and severe storm exposure factors into most carriers’ rating.

- Project duration: A six-month project costs less than an eighteen-month one.

- Endorsements: Soft costs, flood, earthquake, ordinance and law, and higher debris removal limits each add premium.

- Deductible: Higher deductible, lower premium. Set it at a level the contractor can absorb without delaying the project.

Construction site theft is also a recurring exposure. In September 2025, Florida law enforcement dismantled a $2 million construction equipment theft ring, an example of the scale at which organized theft from construction sites operates. Materials staged for installation, including copper, HVAC units, lumber, and appliances, are common targets across the country, Indiana included. Adequate theft limits and basic site security both matter.

What Your Construction Contract Is Actually Requiring

Construction contracts often include specific insurance language that goes beyond “carry builders risk.” Common requirements cover policy form, minimum coverage limits, named insured language, additional insured endorsements, and waiver of subrogation.

Two terms worth knowing on first read:

- Additional insured: Adding another party (often the owner or general contractor) to the policy gives them coverage rights for losses arising from the named insured’s work.

- Waiver of subrogation: A clause where the insurer agrees not to pursue recovery against another party after paying a claim. Common on commercial projects.

Treating a certificate of insurance, or COI, as proof of coverage is the trap most contractors fall into. IRMI is direct on this point: the COI is informational only and doesn’t verify the policy actually matches what the contract requires. The right way to confirm coverage is to read the policy itself, not the COI.

For Indiana contractors, contract review matters at scale. Construction contributed approximately $27 billion to Indiana’s economy in 2023, about 5% of state GDP. Across an industry that size, the specific contract language is what determines whether a builders risk policy actually responds when a claim hits.

A few specific items worth reading carefully:

- Whose policy it is: Confirm the named insured matches who is actually buying the policy.

- Coverage limit: Compare the policy limit to projected completed value plus any required soft costs.

- Additional insureds: Confirm the policy adds the parties the contract requires.

- Waiver of subrogation: Confirm the endorsement is on the policy, not just promised.

- Cancellation notice: Many contracts require advance notice of cancellation. Confirm the policy supports it.

How Torian Insurance Helps

At Torian Insurance, we’ve worked with Indiana contractors and homebuilders since 1923. We’re an independent agency, which means we shop multiple carriers, including Acuity, Cincinnati Insurance, Hanover, Philadelphia, Markel, and Hiscox, to match the right builders risk coverage to each project.

Builders risk is rarely a stand-alone purchase. Most contractors we work with carry general liability, contractor insurance, commercial auto, and inland marine alongside their project builders risk policies. We’re licensed in Indiana, Kentucky, and Illinois, and we work with general contractors, HVAC contractors, plumbers, landscapers, and remodelers. We can review a construction contract, identify what coverage it actually requires, and bring quotes from the right carriers.

Frequently Asked Questions About Builders Risk Insurance

Who buys builders risk insurance, the owner or the contractor?

The construction contract decides. On large commercial projects, the property owner often carries builders risk. On residential and smaller commercial projects, the general contractor frequently carries it, and on some subcontracts a specialty trade subcontractor can be required to. The contract is the source of truth, not industry convention.

What is the duration of a builders risk insurance policy?

Most builders risk policies last the duration of the construction project, typically six to eighteen months. Coverage starts at construction start or first material delivery and ends at the earliest of substantial completion, occupancy, or a stated post-completion window of often 90 days. Extensions can usually be requested before the original term expires.

Does builders risk insurance cover renovation projects?

Yes. Builders risk policies are routinely written for renovation in addition to new construction, and the key consideration is how the policy treats existing structures. IRMI notes that many policies cover existing structures at actual cash value rather than replacement cost, which can create a significant funding shortfall if older portions of the building are damaged during the project. On older Indiana homes and historic commercial buildings, read the existing-structure clause carefully and ask about replacement-cost endorsements.

How do I choose a builders risk insurance policy?

Match the policy to the project. Read the contract first and note the required coverage limits, named insured language, additional insureds, waiver of subrogation, and any specific endorsements. Then compare policies that meet those requirements. Pay particular attention to the existing-structure clause on renovations, the soft costs endorsement on financed projects, and the post-completion extension on projects that may run long.

Talk With a Local Agent

Builders risk requirements show up at the worst time, usually right when a project is supposed to start. The right policy depends on the project, the contract, and which carriers’ forms fit. An independent agent who knows Indiana construction can save the time of figuring it out alone.

Have a project that needs builders risk coverage, or a contract you’d like reviewed before you sign? Contact Torian Insurance to talk with a local agent.