The Ohio River runs nearly 1,000 miles from Pittsburgh to Cairo, Illinois, forming the entire border between Indiana and Kentucky. For Evansville-area boaters, that geography brings real complexity to choosing boat insurance in Indiana. Lock and dam navigation, barge wake hazards, debris from upstream storms, and marina contracts that don’t always match state law all factor in.

Key Takeaways

- Indiana does not legally require boat insurance for recreational vessels, but most marinas and lenders require liability and physical damage coverage as a condition of slip rental or financing.

- The Ohio River is one of the busiest commercial inland waterways in the United States, creating wake, debris, and lock-traffic exposures that generic state-level boat insurance pages overlook.

- The closest navigation chokepoints for Evansville-area boaters are the Newburgh Lock and Dam at Mile 776.1 and the McAlpine Locks and Dam at Mile 606.8 in Louisville, both operated by the US Army Corps of Engineers.

- Agreed value coverage pays the pre-agreed amount on a total loss with no depreciation deduction, while actual cash value pays depreciated market value, which can leave older Ohio River boats significantly underinsured.

- Homeowners insurance generally provides only limited coverage for small, low-horsepower craft, so most powered vessels need a standalone watercraft policy.

Boat Insurance Requirements in Indiana, Kentucky, and Illinois

Indiana law does not require boat insurance for recreational watercraft. Neither do Kentucky or Illinois. State law does require registration of motorboats and most other watercraft through the Indiana Bureau of Motor Vehicles, but stops short of mandating insurance coverage. The practical reality is different: marinas, slip rental contracts, and boat lenders almost always require liability and physical damage coverage.

Registration and insurance are separate requirements, and that distinction trips up new boat owners. Indiana issues a registration number and decals for motor-powered boats and most other watercraft, but it does not ask for proof of insurance during registration. The contractual layer is what fills the gap:

- Public and private marinas across Evansville, Newburgh, Henderson, and Louisville typically require slip renters to carry liability coverage, often at minimums of $300,000 or higher, and to name the marina as an additional insured (a party listed on the policy as also protected from a covered loss).

- Boat lenders require both liability and physical damage coverage for the full term of the loan, and they will force-place more expensive coverage if a policy lapses.

A certificate of insurance (COI) is the standard document marinas request. It’s a one-page summary from your insurer proving coverage is in force and listing any additional insureds, and most marinas want it on file before you take a slip.

Why the Ohio River Changes the Coverage Conversation

Ohio River boating involves exposures that don’t show up on generic state-level insurance pages. The river carries some of the heaviest commercial barge traffic of any inland waterway in the country, channels narrow at active lock chambers, and pool levels can shift sharply after storms hundreds of miles upstream. Recreational coverage on the river needs to anticipate all three.

Recreational boating in the United States produced 3,887 reported incidents and 556 fatalities in 2024, with operator inattention, improper lookout, inexperience, and machinery failure leading the contributing factors. The Ohio River layers regional conditions on top of those general risks.

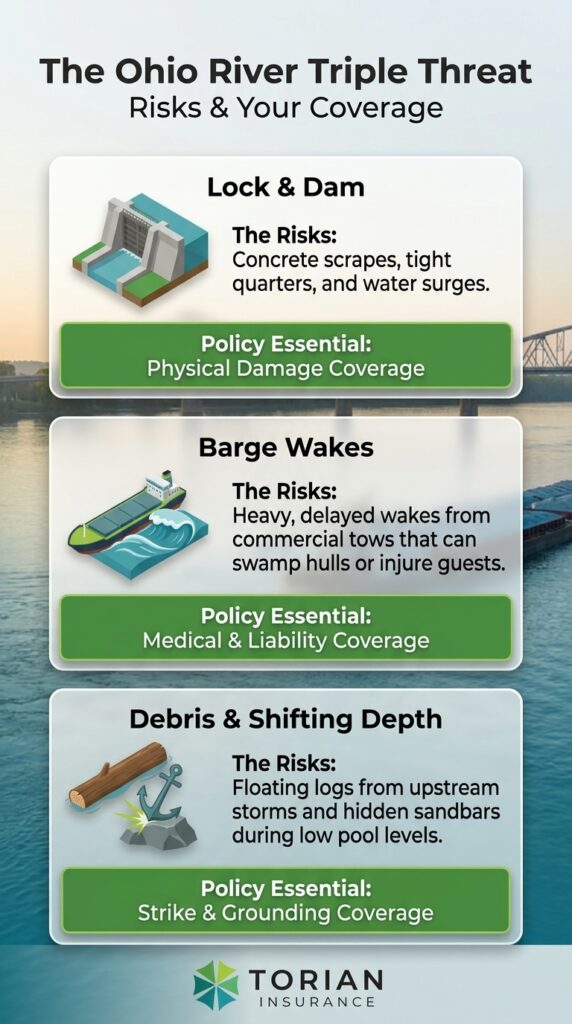

Lock and Dam Navigation Between Newburgh and McAlpine

The two locks tri-state boaters encounter most often are the Newburgh Lock and Dam at Ohio River Mile 776.1 and the McAlpine Locks and Dam at Mile 606.8 in Louisville. Both are operated by the US Army Corps of Engineers, Louisville District.

Lock chambers are tight quarters, especially when commercial tows have priority. Sudden water releases, fender slips, and other vessels’ mistakes can scrape gel coat, dent rubrails, damage lower units, or break props. Physical damage coverage on a watercraft policy pays for those repairs, and a single bad locking can run thousands of dollars without it.

Commercial Barge Traffic and Wake Hazards

Even on calm days, the Ohio River channel produces large, unexpected wakes. Towboats push long multi-barge formations, and the displacement wake from a passing tow can keep rolling well after the towboat itself has cleared the area. For recreational boats crossing behind a tow at the wrong angle, the result can be hull damage, swamped passenger compartments, or thrown passengers.

Liability and medical payments coverage become especially relevant when guests are aboard. If a wake throws a passenger and they hit a console, the on-water medical bills are typically covered by the boat policy, not your homeowners or auto policies.

Debris and Fluctuating Water Levels

Storms across the upper Ohio Valley send logs, branches, propane tanks, and other debris hundreds of miles downstream. High water exposes new submerged hazards as the channel shifts; low water reveals stumps and rock formations that don’t appear on older charts. Debris strikes, prop damage, and grounding from sudden pool changes are common claims drivers across river-county marinas.

What a Standalone Boat Insurance Policy Typically Covers

A standalone watercraft policy typically combines liability for bodily injury and property damage to others, physical damage for the boat, motor, and trailer, medical payments for onboard injuries, uninsured boater coverage, and protection for personal property carried aboard. For a deeper breakdown of what each coverage type does, our explainer on what boat and watercraft insurance does for you walks through the foundational components.

The watercraft insurance options Torian places through the carriers it shops typically include:

- Liability limits at multiple tier levels, often paired with personal umbrella coverage for boats that pull skiers or tubes at speed.

- Physical damage coverage with agreed value or actual cash value structure, plus optional consequential damage and freshwater corrosion endorsements.

- Towing and on-water assistance after a breakdown.

- Coverage for fishing equipment, electronics, and other personal property aboard, with scheduled endorsements available for higher-value items.

- Fuel spill liability, which covers the cleanup costs that follow a sunken or damaged boat releasing fuel into a waterway.

Water-sports activity adds liability exposure that’s easy to underestimate. As BoatUS Foundation President Chris Edmonston told TODAY about tubing: “When you’re tubing, you’re going about 18 to 25 miles per hour. And when you fall off, it can almost be like hitting concrete.” Boats that regularly tow tubes, water skis, or wakeboards generally need higher liability limits than a casual cruiser.

Agreed Value vs. Actual Cash Value: A Critical Choice for River Boats

On older fishing rigs, pontoons, and runabouts common on Ohio River waters, the difference between agreed value and actual cash value coverage can run into thousands of dollars at claim time. The two settlement methods work differently:

- Agreed value: Pays the amount stated on the policy if the boat is a total loss, with no depreciation deduction.

- Actual cash value (ACV): Pays the depreciated market value at the time of the loss.

A 1996 pontoon insured at $18,000 of actual cash value might settle for closer to $7,000 to $9,000 after depreciation if it sinks during a flood event. The same boat insured at an agreed value of $18,000 settles at $18,000, less the deductible, regardless of depreciation.

Agreed value usually costs more in premium and isn’t available on every vessel. Many carriers cap it to boats under a certain age or require a recent survey, and ACV is the default on many older policies. For owners who would replace a totaled boat with another similar one, the agreed value premium difference is usually worth it.

Does Homeowners Insurance Cover Your Boat?

Homeowners insurance typically covers only small, low-horsepower watercraft like canoes, kayaks, and small sailboats, with limited coverage for boating, and liability for operating a boat is generally not included unless added by endorsement. Most powered vessels, including bass boats, pontoons, ski boats, and cruisers, need a standalone watercraft policy.

Common limits in standard homeowners policies cap watercraft property damage at modest amounts and provide minimal bodily injury protection. Larger motors, fishing rigs, runabouts, ski boats, and pontoons typically fall outside that envelope. If a boat is stored in a covered structure attached to your home insurance policy, the structure may be covered, but the watercraft and its operation generally are not.

A separate watercraft policy fills that gap. For boats that travel between Indiana, Kentucky, and Illinois waters, having dedicated coverage also avoids ambiguity about which state’s loss adjustment standards apply if a claim happens away from home.

How Torian Insurance Helps Ohio River Boaters

At Torian Insurance, we have spent more than a century insuring families and businesses across the tri-state. We know the boats, the marinas, and the river. As Evansville’s largest locally owned independent insurance agency, we shop multiple carriers to match each client to the policy structure that fits their boat, their navigation patterns, and their slip and lender requirements.

That work starts with a conversation about how and where you boat. A bass fisherman who launches at Newburgh and runs upriver to Owensboro has different exposure than a family that keeps a pontoon at a private marina. Agreed value versus actual cash value, liability layering through a personal umbrella policy, and the right additional insureds on a marina contract are decisions we walk through together. If you already carry a watercraft policy, we can review it against your slip contract and lender’s terms before a claim happens.

Frequently Asked Questions About Boat Insurance in Indiana

Is boat insurance required in Indiana?

No. Indiana law does not require insurance for recreational boats. State law does require boat registration through the Indiana BMV, and most marinas and lenders require proof of liability and physical damage coverage even though the state itself does not.

How much does boat insurance cost in Indiana?

Premiums vary based on boat type, value, age, motor size, intended use, and the operator’s experience and claims history. Newer boats with high replacement values, high horsepower, or aggressive water-sports use generally cost more than older, smaller boats. Comparing quotes from multiple carriers through an independent agency is the most reliable way to see realistic numbers for a specific boat.

Do I need boat insurance for the Ohio River?

No state in the tri-state region legally requires insurance to operate a recreational boat on the Ohio River. However, most public marinas near Evansville, Newburgh, Henderson, and Louisville require proof of liability and physical damage coverage as a condition of slip rental, and lenders require coverage for the full term of the loan.

Does my Indiana boat insurance cover me on the Kentucky or Illinois side of the river?

Most watercraft policies cover boating across nearby state lines without modification, but the navigation territory of your specific policy should be confirmed before you cross into Kentucky or Illinois waters. Some policies limit coverage to inland lakes or exclude commercial waterways like the Ohio River, so verifying your policy’s navigation language with your agent prevents a denied claim later.

Should I insure jet skis and smaller watercraft separately?

Yes, in most cases. Jet skis and personal watercraft are typically excluded from homeowners coverage and need a dedicated watercraft policy with appropriate liability limits. Some homeowners policies do cover small sailboats or canoes under specific horsepower or length thresholds, but those limits rarely match the speed and exposure of modern jet skis.

Talk to a Local Agent About Your Coverage

Ohio River boating is a way of life across the tri-state. Choosing coverage that matches locks, debris, barge traffic, and the patchwork of marina and lender requirements takes more than filling out a national carrier’s online form. If you have questions about your current watercraft policy or want to compare quotes from multiple carriers, contact Torian Insurance to talk with a local agent who knows the river.