In March 2025, a long-abandoned coal mine gave way beneath a Chandler, Indiana neighborhood, and homes on Monroe Avenue cracked, tilted, and sank. Most of the hardest-hit families learned too late that a standard homeowners policy pays nothing for this kind of damage. Mine subsidence insurance in Indiana is the separate coverage that fills that gap, and it matters for homeowners and business owners across the tri-state, where old underground mines still run beneath parts of Indiana, Kentucky, and Illinois.

Key Takeaways

- Standard homeowners and commercial property policies exclude mine subsidence, the collapse of an underground coal mine, so it has to be added to your policy as a separate coverage.

- In Indiana, the coverage is available in 26 southwestern counties and protects structures for up to $500,000, with a 2% deductible (minimum $250, maximum $500) and up to $15,000 in additional living expenses.

- It is inexpensive because the state sets the rates, and the Indiana Department of Insurance describes the premiums as structured to keep the coverage within reach; your exact premium depends on how much coverage you carry.

- You must have the coverage in place before any damage occurs; you cannot add it after the ground starts moving and still file a claim.

- You can check whether your address sits over or near a former mine using the free Indiana DNR Coal Mine Information System (CMIS) map.

- Neighboring programs differ: Illinois includes coverage automatically in 34 counties (up to $750,000) unless you waive it, and Kentucky covers 37 counties, up to $500,000 plus $50,000 in living expenses.

What Is Mine Subsidence, and Why Doesn’t Homeowners Insurance Cover It?

Mine subsidence is the collapse of an underground coal mine that causes the ground above it to sink, crack, or shift, damaging any structure built on top. Standard homeowners and commercial property policies exclude this kind of earth movement, which is why a separate coverage exists. Mine subsidence insurance is an endorsement, meaning an add-on to your existing policy, that pays for structural damage caused by a mine collapse.

Because mine subsidence involves the ground itself moving, it falls into a category of losses that standard policies routinely exclude:

- Earthquakes and aftershocks.

- Landslides and mudflows.

- Gradual settling of soil beneath a foundation.

- Mine subsidence, the sudden collapse of an abandoned underground coal mine, the focus of this guide.

That exclusion is written into the policy form, so it applies no matter how much dwelling coverage you carry. If a former mine gives way beneath your home, your regular homeowners policy will not pay for the cracked foundation or the structure tilting off its footing. Mine subsidence sits alongside flood and earthquake on the list of things a standard homeowners policy may not cover, and it has to be added deliberately. It is also different from a natural sinkhole: the damage comes from a human-made coal mine giving way, not general ground settling.

Which Indiana Counties Are Eligible for Mine Subsidence Insurance?

Mine subsidence insurance is available in 26 southwestern Indiana counties that sit along the Illinois Coal Basin. If you own a home, farm, or commercial building in one of them, you can add the coverage to your property policy. The program runs through the Indiana Mine Subsidence Insurance Fund, administered by the Indiana Department of Insurance.

For the Evansville area, that includes Vanderburgh and Warrick counties, where communities like Newburgh and Chandler sit on a long history of underground coal mining. Torian Insurance, based in Evansville at 3000 E Division St, works with property owners across these counties.

Here are all 26 Indiana counties currently eligible for mine subsidence coverage:

| County | County |

|---|---|

| Clay | Owen |

| Crawford | Parke |

| Daviess | Perry |

| Dubois | Pike |

| Fountain | Posey |

| Gibson | Putnam |

| Greene | Spencer |

| Knox | Sullivan |

| Lawrence | Vanderburgh |

| Martin | Vermillion |

| Monroe | Vigo |

| Montgomery | Warren |

| Orange | Warrick |

How Do I Know If My Home Is at Risk for Mine Subsidence?

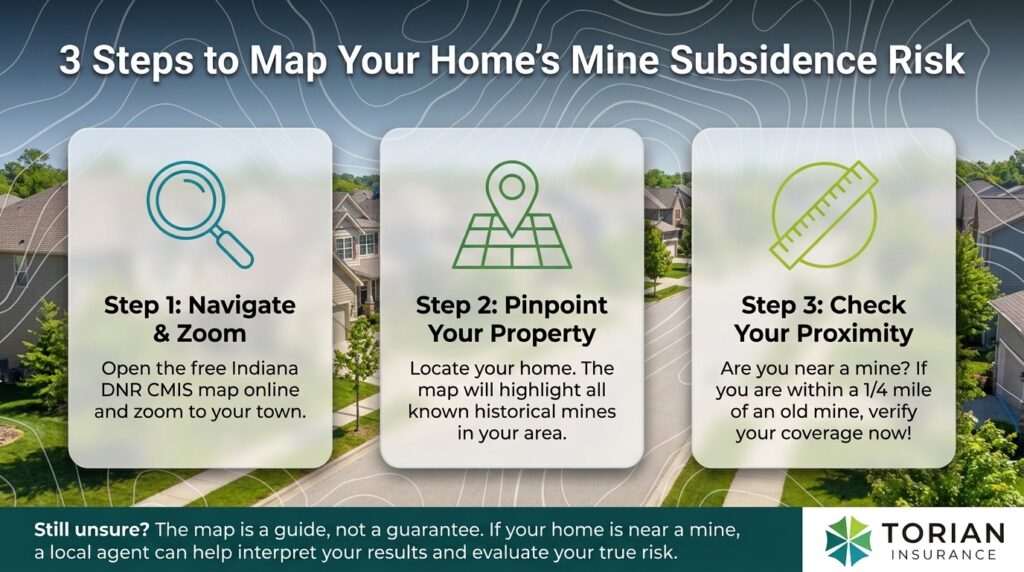

You can check your address against Indiana’s mapped coal mines using the Indiana DNR Coal Mine Information System, or CMIS, a free online map viewer. It shows documented underground and surface coal mines across the state, so you can see whether your home sits over or near a former mine.

To check your own risk, follow these steps:

- Open the CMIS map viewer and zoom to your town, for example Evansville, Newburgh, or Chandler.

- Find your street and home. The map marks documented underground and surface mine workings in the area.

- Note how close your structure is to a mapped mine. During the Chandler response, one local estimator advised that if your home is within about a quarter mile of a former mine, it is worth confirming your coverage right away.

The DNR notes the map is for informational and planning purposes, not a legal determination of risk. Being near a mine, not only directly over one, can still put a structure in play, so if the map leaves you unsure, a local agent can help you read it and weigh whether the coverage makes sense.

How Much Does Mine Subsidence Insurance Cost in Indiana?

Mine subsidence insurance in Indiana is inexpensive because the state sets the rates, not individual carriers, so the price is the same no matter which carrier writes your policy. The premiums are structured to keep the coverage affordable, and your exact cost depends mainly on how much coverage you carry.

A few things shape what you pay:

- The amount of coverage: your premium rises with the dwelling limit you insure, up to the $500,000 maximum.

- The type of structure: rates for commercial and non-dwelling structures run somewhat higher than for a home.

- Not the carrier: because the rate is state-set and reinsured through the Indiana Mine Subsidence Insurance Fund, it is the same whichever company writes your policy.

Because the coverage is state-rated and added as an endorsement, it is one of the more affordable protections you can put on a property. For an exact premium at the coverage amount you need, a local agent can give you a quote.

What Indiana’s Mine Subsidence Coverage Includes and Excludes

Indiana’s coverage pays up to $500,000 per structure for damage caused by a coal mine collapse, after a deductible (what you pay out of pocket before coverage applies) of 2% of the policy, with a minimum of $250 and a maximum of $500. Insurers must also offer up to $15,000 in additional living expenses, or ALE, which covers staying elsewhere while your home is repaired.

Here is how Indiana’s program works at a glance:

| Item | Detail |

|---|---|

| Maximum coverage | Up to $500,000 per structure |

| Deductible | 2% of the policy (minimum $250, maximum $500) |

| Additional living expense (ALE) | Up to $15,000 (insurers must offer it; effective January 1, 2017) |

| Who is eligible | Owners of a home, farm, or commercial property in a designated county, anyone with basic fire coverage on the structure |

| When to buy it | Any time, but the structure must be insured before any damage occurs |

| Cost | State-set and structured to be affordable; the premium rises with the coverage amount |

| Not covered | Earthquake, landslide, active mining, land, trees, crops, and contents; detached structures are insured separately |

What Mine Subsidence Coverage Does Not Cover

The coverage is specific to coal mine collapse. It does not pay for:

- Earthquakes, landslides, and volcanic eruptions.

- Storm-sewer-drain collapse and damage from active mining.

- Land, trees, crops, and the contents of your home.

- Detached structures like garages and silos, which are insured separately.

Like other homeowners policy exclusions, these gaps are easy to miss until a claim is filed, so it helps to read your policy and ask your agent what is included.

When You Must Buy It: The Timing Rule

The most important rule is timing. To be eligible for a claim, your structure has to be insured before any mine subsidence damage occurs. You can add it at any point before a loss, and it is available to anyone who carries basic fire coverage, but you cannot wait until the ground starts moving. Once subsidence has begun, it is too late for that event.

How to Add Mine Subsidence Coverage to Your Policy

Because it is an endorsement, you add mine subsidence insurance through the same agent who handles your property policy. There is no separate application; your agent adds it to your homeowners, farm, or commercial property coverage. Buying or refinancing a home in an eligible county is a natural moment to confirm the coverage is on your policy.

The 2025 Chandler Mine Collapse and What It Showed Tri-State Homeowners

On March 1, 2025, an abandoned coal mine collapsed beneath a neighborhood in Chandler, Indiana, in Warrick County. Over the following days the ground dropped by up to 18 inches in places along Monroe Avenue, and homes cracked and tilted off their foundations. Local estimates put the damage at roughly 15 to 17 homes, with about five considered likely total losses.

The detail that stood out afterward was insurance. Most of the hardest-hit families did not carry mine subsidence coverage. One homeowner, Terra Norman, was the only owner among the likely total losses who had bought it.

The Indiana Department of Natural Resources responded by advising residents near former mines to buy mine subsidence insurance. The collapse is a plain illustration of the coverage’s core rule: it only helps if it is already on your policy when the ground moves.

How Mine Subsidence Coverage Compares in Kentucky and Illinois

All three states run mine subsidence programs, but they differ in how you get the coverage and how much you can carry. Torian Insurance is licensed in Indiana, Kentucky, and Illinois, and the same Illinois Coal Basin under southwestern Indiana extends into western Kentucky and southern Illinois.

Here is how the three programs compare:

| State | Counties | How you get coverage | Maximum per structure |

|---|---|---|---|

| Indiana | 26 | You opt in and add it to your policy, any time | $500,000 |

| Illinois | 34 | Included automatically unless you reject it in writing | $750,000 |

| Kentucky | 37 | Included at a separate premium unless you waive it in writing | $500,000 plus $50,000 for living expenses |

Mine Subsidence Insurance in Kentucky

In Kentucky, mine subsidence coverage is available to residents of 37 eligible counties. Under state law (KRS 304.44-030), policies in those counties include it at a separately stated premium unless the owner waives it in writing. As of January 1, 2025, the maximum is $500,000 per structure plus up to $50,000 in additional living expenses. For tri-state homeowners near Henderson and the Kentucky side of the Ohio River, this is the program that applies.

Mine Subsidence Insurance in Illinois

Illinois works differently. In 34 designated counties, insurers include mine subsidence coverage automatically unless you reject it in writing. The Illinois Mine Subsidence Insurance Fund reinsures the coverage up to $750,000 per structure, the highest limit of the three states. If you own property in a southern Illinois county, check your policy, because the coverage may already be on it.

How Torian Insurance Helps

At Torian Insurance, we have helped homeowners, farm owners, and business owners across the Evansville area and the tri-state protect their property since 1923. Because we are an independent, locally owned agency, we shop multiple carriers to find the right fit, and we can add mine subsidence coverage to the property policy you already carry.

We can also help you make sense of the CMIS map, confirm whether your county and address put you at risk, and weigh the small annual cost against a potential loss. If you already carry the coverage, we can review your limits to make sure they keep pace with what it would cost to rebuild. That guidance is what our clients tell us they value most.

Frequently Asked Questions About Mine Subsidence Insurance

Is mine subsidence insurance mandatory in Indiana?

No. In Indiana, mine subsidence insurance is optional and you have to opt in. It is not included automatically the way it is in Illinois and Kentucky, so you or your agent has to add it, and it has to be in place before any damage occurs.

Does mine subsidence insurance cover my detached garage or the contents of my home?

No. The coverage applies to the specific structure it is written on, so a detached garage, silo, or other separate building must be insured separately. It also does not cover your home’s contents, land, trees, or crops, which fall outside the program.

Can I buy mine subsidence insurance after I notice damage?

No. To be eligible for a claim, your structure must be insured before any mine subsidence damage occurs. Once the ground has started moving, it is too late to add coverage for that event. This is the single most important thing to understand, and it is why checking your risk early matters.

Does mine subsidence insurance cover sinkholes or earthquakes?

No. Mine subsidence insurance covers damage specifically from the collapse of an underground coal mine. Natural sinkholes, earthquakes, and landslides are different perils and are not covered under this endorsement, even though they also involve the earth moving.

Protect Your Home Before the Ground Moves

Mine subsidence is a narrow risk, but for homes and businesses sitting over old coal mines in the tri-state, it is a real one, and it is inexpensive to cover. The rule that matters most is timing: the coverage only works if it is already in place when the ground shifts.

If you are not sure whether your property is at risk or whether your policy includes this coverage, contact Torian Insurance to talk with a local agent who can review your situation and help you find the right fit.