Homeowners insurance is a necessary evil for most of us. One of the decisions you’ll need to make when buying homeowners insurance is what deductible to choose. The problem is, most people don’t understand how home insurance deductibles work and as a result, they often end up with a policy that doesn’t offer the best protection for their needs.

By educating yourself on this topic, you can be sure that you are getting the best possible protection for your family and your home.

This guide will help you get a better understanding of home insurance deductibles so that you are better equipped to make an informed decision on what is right for you.

What Is a Deductible for Homeowners Insurance?

Homeowners insurance deductibles are the amount of money that a policyholder must pay out-of-pocket before their insurance coverage kicks in.

What Is the Standard Homeowners Insurance Deductible?

Deductibles for home insurance policies typically range from $500 to $5,000, but some home insurance companies offer deductibles as high as $10,000. The higher your home insurance deductible is, the lower your home insurance premium (monthly or annual payment) will be.

For example, let’s say you have a home insurance policy with a $500 deductible. If your home sustains $1,500 worth of damage in a covered event, you’ll pay the first $500 and your home insurance will cover the remaining $1,000.

How Does My Home Insurance Deductible Affect My Premium?

Your insurance deductible amount will have a direct impact on your premiums. In general, the lower your deductible, the higher your premium will be. That’s because there’s a greater chance that the insurance company will have to pay out on a claim, and they need to cover their costs. However, if you choose a high deductible, you could end up paying more out of pocket if something happens to your home.

Low Deductible vs. High Deductible

A low deductible may be preferable if you want to avoid any surprises in the event of a claim, but it will also cost more each month. If you’re comfortable with taking on more risk and are willing to pay more in case of an incident, go with a lower deductible.

On the other hand, you’ll want to consider a higher deductible if you want to save on premiums but it also means that you will have to pay more out of pocket if you need to file a claim.

No matter what deductible you choose, be sure to have enough saved up to cover it in case of an emergency. Talking to an agent at a reputable insurance agency can help you learn more about the different options available to you.

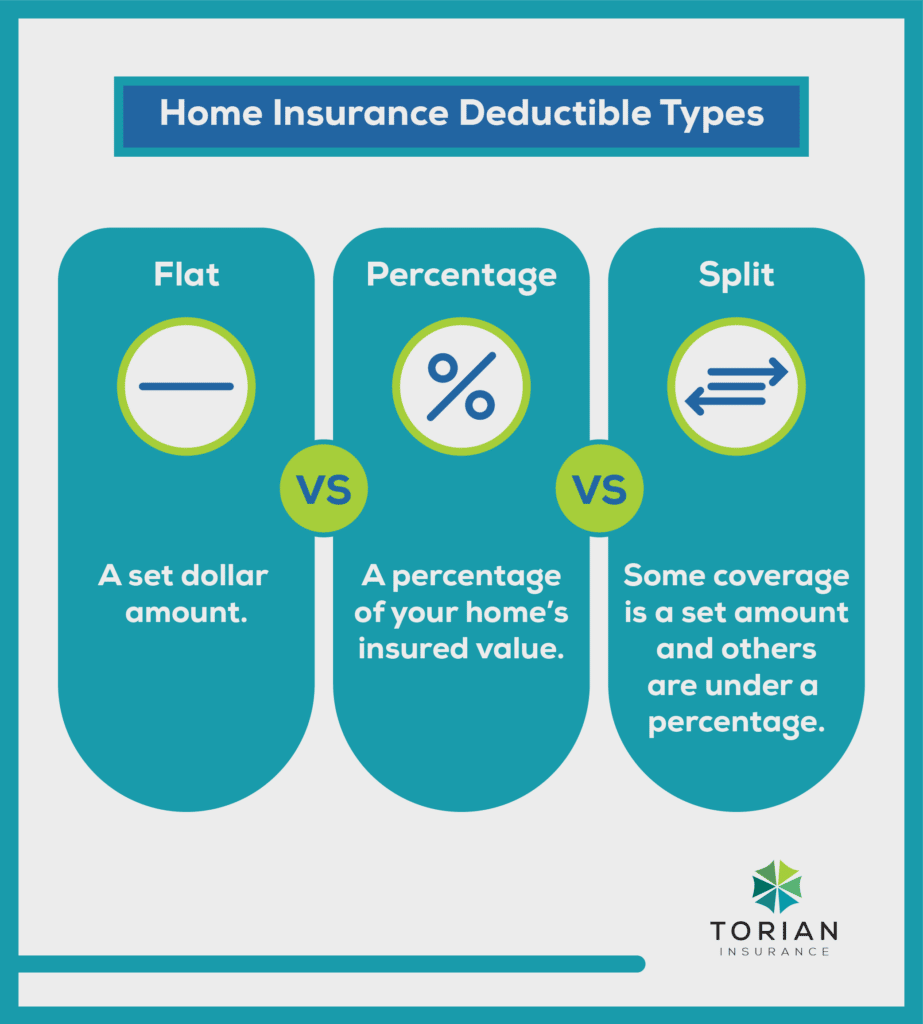

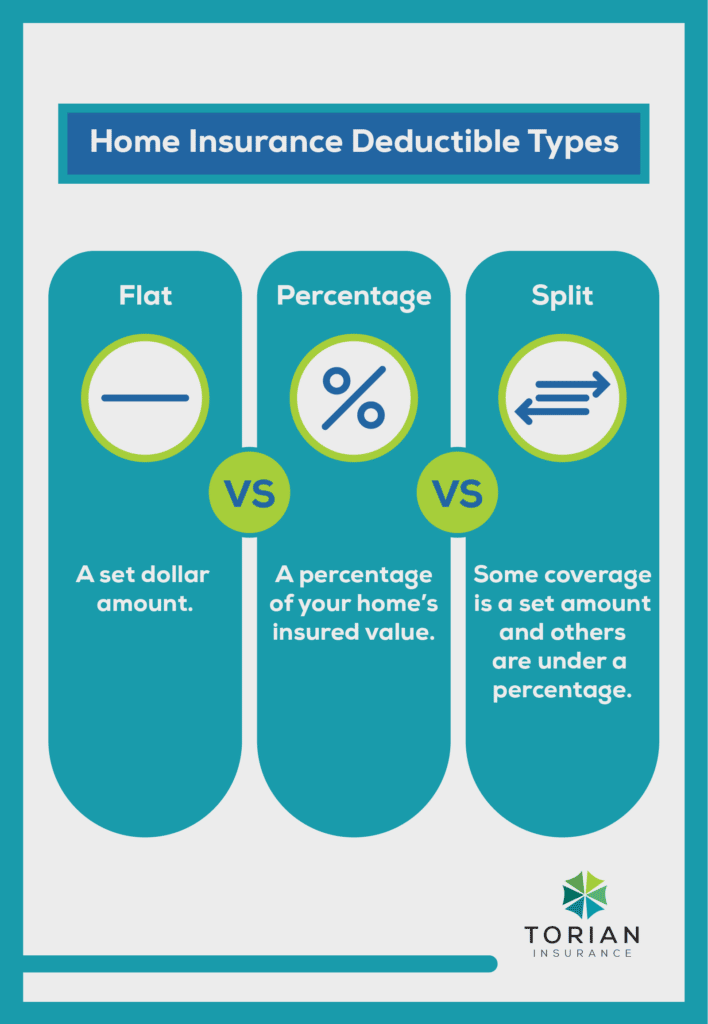

Types of Homeowners Insurance Deductibles

Homeowners also need to consider the type of deductible they will be paying. The two most common types are flat and percentage-based, but there’s also hybrid deductibles that combine both principles which might be more beneficial based on your unique circumstances.

Flat Deductibles

A flat deductible, also known as a “dollar-amount deductible”, is a set amount that you must pay out-of-pocket before your home insurance policy kicks in. For example, if you have a $500 deductible and your home sustains $5,000 in damage from a covered incident, you will pay the first $500 and your insurer will cover the remaining $4,500. This is the simplest type of deductible, but it can be expensive if your home suffers major damage.

Percentage Deductibles

A percentage deductible is based on a percentage of your home’s insured value. So, if your home is insured for $200,000 and you have a 2% deductible, you would owe $4,000 out of pocket before your coverage kicks in ($200,000 X 2% = $4,000). This type of deductible is usually cheaper than a flat deductible, but it can still be expensive if your home suffers major damage.

Split Deductibles

A less common type is a split deductible, sometimes called a “disaster deductible”, where the deductible is split with some coverage under a set dollar amount and some based on a percentage of your home’s insured value for specific types of damage. For example, you might have a 2% deductible for all damages except for wind and hail, in which case you would have a flat $1,000 deductible.

If you live in an area that is prone to natural disasters such as hurricanes, hail, earthquakes and floods—a split deductible may be a good option for you.

Choosing the Right Home Insurance Deductible for You

The right homeowners insurance deductible for you depends on a number of factors, including your budget and risk tolerance. So how do you decide what’s right for you? To get started, ask yourself the following questions.

1. How much can you afford to pay out-of-pocket in the event of a claim?

2. How much risk are you comfortable taking on?

3. What is the average cost of home repairs in your area?

4. Are you comfortable self-insuring for smaller home repairs, or do you want the peace of mind that comes with having coverage?

If you’re not comfortable taking on the financial risk of a higher deductible, consider opting for a lower one. However, keep in mind that opting for a lower deductible will likely result in higher premiums.

Whatever you decide, make sure the amount of coverage offered by your home insurance policy is enough to cover your losses. If your home is destroyed in a fire, for example, your home insurance policy should cover the cost of rebuilding or repairing your home.

You will want to choose a deductible that is high enough so that you won’t have to use your home insurance policy for minor losses, but low enough so that you’ll be covered in the event of a major loss.

Let Torian Insurance Help You with This Important Decision

If you’re in the market for homeowners insurance, it’s important to understand all of the different factors that go into choosing a policy. The best way to find the right homeowners insurance deductible for you is to speak with a professional.

At Torian Insurance, we know that every homeowner’s situation is different, so we offer a variety of options for deductibles as we are not limited to one specific insurance company with only their options to choose from. Let us help you navigate this process and find the homeowners insurance policy that fits your needs.