Indiana is a state that is known for its diverse landscape, from rolling hills and farmland to bustling cities and waterfront communities.

While this diversity makes Indiana a great place to live and work, it also means that the state is susceptible to a wide range of natural disasters, including floods.

Flooding is one of the most common and costly natural disasters in the United States, and can cause significant damage to homes, businesses, and infrastructure.

In this blog, we will explore the question of whether or not you really need flood insurance in Indiana and the surrounding area. We’ll look at the history of Indiana floods and how climate change can affect flood risk in the future. We will also dive into various factors that determine your risk level—including your properties location and its proximity to water.

Whether you are a homeowner, renter, or business owner in Indiana, understanding flood risk and the importance of flood insurance is essential for protecting your property and securing your financial future.

What is Flood Insurance?

Flood insurance is a type of insurance policy that provides coverage for property damage and loss caused by floods. It is important to understand that standard homeowner’s insurance policies do not cover damage caused by floods. Therefore, it is necessary to purchase a separate flood insurance policy to protect your home and belongings in the event of a flood.

Flood insurance policies are typically provided by the National Flood Insurance Program (NFIP), which is a federal government program that was established in 1968. The NFIP works with private insurance companies to provide flood insurance policies to homeowners, renters, and business owners.

What Does Flood Insurance Cover?

Flood insurance typically covers damage to your property and belongings caused by flooding.

This can include things like:

- Structural damage: This refers to damage to the physical structure of your home or property caused by flooding. This can include damage to the foundation, walls, roof, and other structural elements.

- Personal property damage: Coverage of personal belongings caused by flooding can include things like furniture, electronics, clothing, and other personal items.

- Cleanup and restoration: Flood insurance can also cover the cost of cleanup and restoration after a flood such as removal of debris, drying out your home, and repairing or replacing damaged items.

It is important to note that flood insurance policies have limitations and exclusions. For example, flood insurance typically does not cover damage caused by sewer backups, unless it is directly caused by a flood. It also does not cover damage to outdoor property such as decks, patios, and landscaping.

Always carefully review the terms and limitations of your flood insurance policy to understand what is covered and what is not. If you have any questions or concerns, be sure to speak with your insurance agent to clarify your coverage.

Are There Any Flood Zones That Require Flood Insurance in Indiana?

In Indiana, flood insurance is required for homes and businesses with government-backed mortgages in Special Flood Hazard Areas (SFHAs). These areas are high-risk flood zones that have been designated by the Federal Emergency Management Agency (FEMA). These areas are typically located near waterways such as rivers, lakes, and streams, and are at risk of flooding during heavy rains and storms.

If your home or commercial property is located in an SFHA and you have a mortgage on your property, you are required by law to purchase flood insurance. This is because lenders want to protect their investment in the property and ensure that it is covered in the event of a flood.

To determine if your property is located in a designated SFHA, you can use FEMA’s Flood Map Service Center. This online tool allows you to enter your property address and view a map of your area with flood zone information.

You can also contact your insurance agent or local government officials for more information on flood zones and insurance requirements in your area.

Do I Need Flood Insurance if I’m NOT in a Flood Zone?

Any lender will require the purchase of flood insurance when a property is located, in whole or in part, inside a recognized flood area. But what happens if your property is NOT in a flood zone?

Flood insurance is not always suggested for everyone, but a significant number of flooding events happen outside of recognized flood zones. In fact, more than 20% of flood insurance claims are from low-to moderate-risk flood zone areas. This is why insurance professionals often encourage their customers to consider adding on this coverage in conjunction with their homeowners insurance, commercial property insurance, or vacation rental policy.

Even if your property is not located in a designated SFHA, it is still a good idea to consider purchasing flood insurance if you live in a flood-prone area.

Floods can occur anywhere, and even a few inches of water can cause significant damage to your property and belongings.

How Much Does Flood Insurance Cost?

The short answer is—it depends. The cost of flood insurance depends on various factors such as the location of the property, the degree of flood risk, the age and construction of the property, the elevation of the property, and the amount of coverage needed.

However, according to the Money Geek, the average cost of flood insurance in Indiana is around $1,142 per year. Understand that this is just an average. The actual cost of flood insurance for your property may be higher or lower depending on your specific circumstances.

Flood insurance policies usually come with a 30 day or less waiting period before they become effective, so it is essential to purchase flood insurance before any flood warnings or alerts are issued. However, there are exceptions to this. For instance, on a new home purchase, policies can now be purchased to meet the requirements of the lender without having to wait 30 days.

In addition to the NFIP, there are also private flood insurance options available in Indiana. These policies may offer more comprehensive coverage and may be a better fit for those living in high-risk flood areas. Pricing will vary for companies that offer this coverage.

Overall, understanding flood insurance is crucial for protecting your property and belongings in the event of a flood.

A Brief History of Indiana Floods

Indiana has a long history of flooding, dating back to its early settlement. The state’s geography, which includes several major rivers and low-lying areas, has made it particularly susceptible to flooding throughout its history.

The Wabash River, for example, has had major floods occurring throughout history, including the devastating flood of 1913. In addition, the Ohio River, which forms the southern border of Indiana, also experienced significant flooding in the Great Flood of 1937.

Here is a timeline of some of the most significant floods in Indiana:

– In 1913, a series of severe storms caused major flooding throughout the state, resulting in the deaths of over 200 people and causing millions of dollars in damages.

– In 1937, the Ohio River experienced a major flood that affected several states, including Indiana. The flood caused widespread damage and forced thousands of people to evacuate their homes.

– In 1957, the Wabash River experienced a major flood that caused extensive damage to homes and businesses in Indiana and Illinois.

– In 2008, a series of severe storms caused major flooding throughout the state, resulting in several deaths and causing millions of dollars in damages.

– In 2018, heavy rains and flooding caused significant damage in several Indiana counties, prompting the governor to declare a state of emergency.

These are just a few examples of the many floods that have impacted Indiana throughout its history. While the state has made significant progress in mitigating flood risk through the construction of levees and other flood control measures, property owners need to remember that disaster can strike when least expected.

Impact of Climate Change on Flood Risk in Indiana

Climate change is having a significant impact on the frequency and severity of floods in Indiana. Rising global temperatures are causing more frequent and intense storms, which can lead to flash floods and river floods. In addition, warmer temperatures are causing more rapid snowmelt, which can also contribute to flooding.

The impact of climate change on flood risk in Indiana highlights the importance of taking action to reduce greenhouse gas emissions and mitigate the effects of climate change. This includes reducing our reliance on fossil fuels, transitioning to renewable energy sources, protecting natural areas, promoting green infrastructure solutions and implementing policies to reduce emissions from transportation and industry.

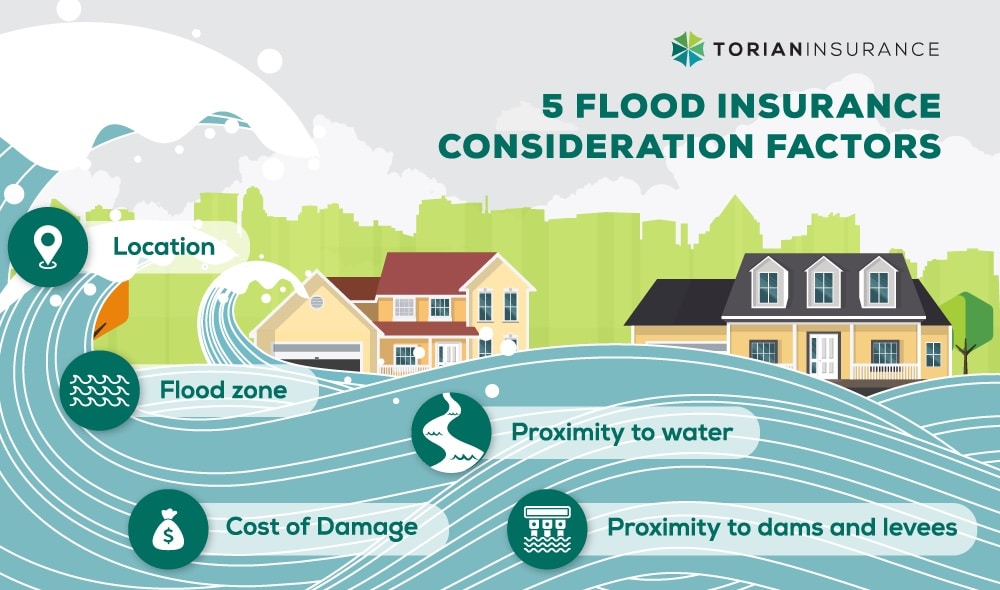

5 Factors to Consider When Deciding if You Need Flood Insurance

When deciding whether or not to purchase flood insurance, there are several factors to consider. Here are 5 of the main considerations to discuss with your insurance agent:

- Location: The location of your property is one of the most important factors to consider when deciding if you need flood insurance. If you live in an area that is prone to flooding, such as near a river or in a low-lying area, then flood insurance is highly recommended.

- Flood zone: It is important to know if your property is located in a high-risk flood zone. The Federal Emergency Management Agency (FEMA) has designated certain areas as Special Flood Hazard Areas (SFHAs), which are at high risk of flooding. If your property is located in an SFHA, then flood insurance is required by law if you have a mortgage on your property.

- Cost of damage: Consider the potential cost of flood damage to your property and belongings. Floods can cause significant damage to homes and personal property, and the cost of repairs and replacements can be very high. If the potential cost of damage is higher than the cost of flood insurance, then it may be worth purchasing a policy.

- Proximity to water: If your home, business or vacation property is located near a body of water such as a lake, river, or an ocean, it is at a higher risk of flooding. Even if you are not in a designated flood zone, water can rise quickly during heavy rains or storms and cause flooding.

- Proximity to dams and levees: Dams and levees are built to help control flooding, but they can also increase the risk of flooding if they fail. If your property is located downstream from a dam or levee, or if you are in an area that is protected by a levee, it is important to consider the potential risks of flooding.

Flood damage can be unexpected and devastating. If you live in an area that is at risk of flooding, it is important to seriously consider purchasing flood insurance.

Do You Need Flood Insurance? Torian Insurance Can Provide Guidance

The question of whether or not you need flood insurance in Indiana, or the surrounding states like Illinois or Kentucky, ultimately comes down to your individual circumstances and level of risk.

Floods can occur anywhere, and the cost of repairing or replacing your property and belongings can be significant. Whether you decide to purchase flood insurance or not, the most important thing is to be informed and prepared.

Understanding your flood risk, knowing your insurance options, and taking steps to protect your property can help to ensure that you and your family are safe and secure, no matter what Mother Nature may bring.

If you live in Evansville, Indiana or the surrounding area, contact Torian Insurance today to see if we can help with your insurance needs. Our team of experienced insurance professionals is dedicated to helping you find the right coverage with customized solutions to protect your home, business, and personal property.