Businesses are increasingly at risk of cyberattacks, but many don’t have the necessary insurance to protect themselves.

Cyber liability insurance can help businesses protect themselves from cyberattacks and recover from a data breach. A data breach can be incredibly costly for a business, both in terms of money and reputation. The average cost of a data breach for a small business is $84,000.

Cyber liability insurance can also protect a business from a fraudulent funds transfer, which can occur without any breach of company data.

In this article, we’ll go over everything you need to know about cyber liability insurance to decide if it’s the right fit for you.

Why do small businesses need cyber liability insurance?

Small businesses need cyber liability insurance to protect themselves from the financial consequences of a cyberattack. This type of insurance can help cover the cost of repairing damage to your company’s computer systems, replacing any lost or stolen data and reimbursement for a fraudulent funds transfer.

Cyber liability insurance is particularly important for small businesses, as they often lack the financial resources to recover from a cyberattack without insurance. In addition, small businesses are often targeted by cyber criminals, as they may have less robust security measures in place compared to larger organizations.

All businesses need cyber liability insurance, but if your small business handles sensitive information, such as customer data or credit card numbers, your business is a prime candidate for purchasing a cyber policy. A cyber policy can help to reimburse your business for the costs of repairing the damage caused by a cyberattack, as well as the costs of any legal fees that may arise as a result of the attack.

Cyber insurance is not required by law, but it is becoming increasingly common for businesses to purchase policies to protect themselves from the financial consequences of a cyberattack.

What does cyber liability coverage help pay for?

Cyber liability insurance can help your small business pay for costs associated with a cyberattack, such as:

- Repairs to your computer systems

- The cost of notifying customers that their data may have been compromised

- Legal fees if you need to sue to recover losses from a cyber attack

- Legal fees if you get sued for not properly protecting your sensitive data.

- Funds “stolen” through a fraudulent funds transfer

- The cost of hiring a forensic consultant to help investigate the cyber attack

- This type of insurance can also help pay for lost income if your business is forced to shut down following a cyber attack.

While the above list is not exhaustive, it gives you an idea of the types of expenses that can be covered by a cyber liability insurance policy.

If you don’t have cyber liability insurance, your small business could be on the hook for all of these costs – which can quickly add up.

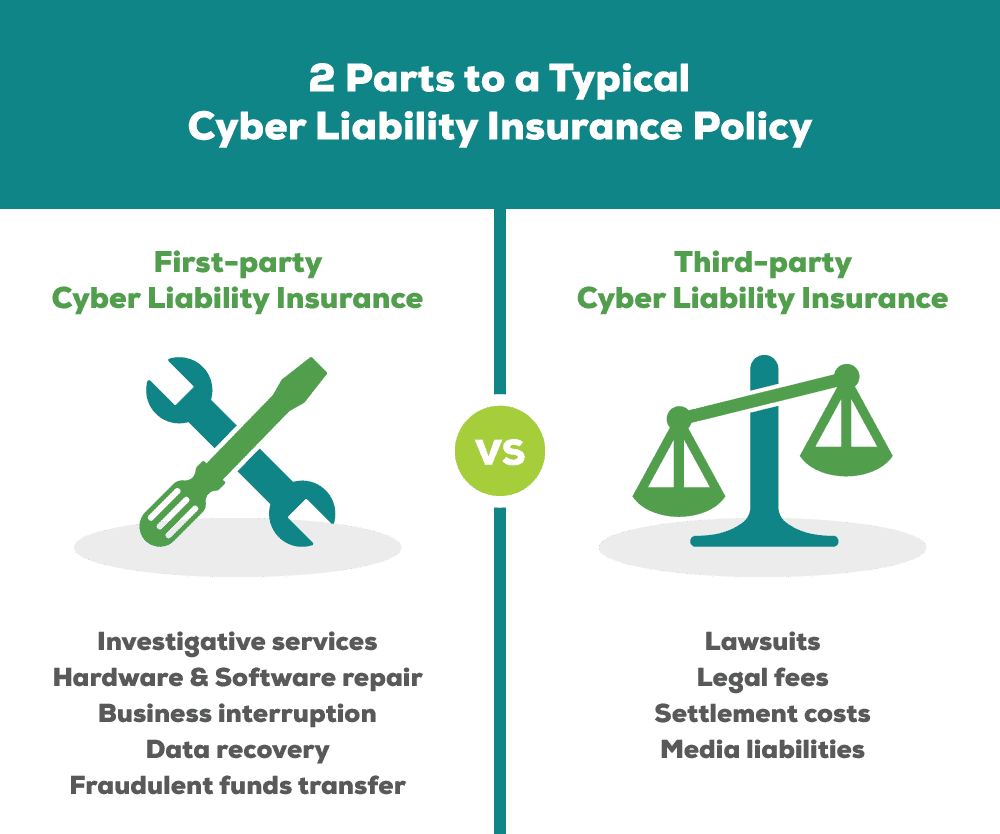

What coverage is built In?

There are two parts to a typical cyber liability policy: first-party and third-party. In most cases, a policy will have both the first and third part coverage built in. At Torian Insurance, we don’t sell any policy that has just one or the other.

First-party cyber liability insurance – covers cyber risks at your company, such as data breaches, cyberattacks, and cyber extortion.

Third-party cyber insurance – covers lawsuits related to cyber risks that your company may have caused. For example, if you are a retailer and a customer’s credit card information is stolen from your website, the customer could sue you for damages.

Most small businesses need both types of coverage, but the amount of coverage you need depends on the size and type of your business, as well as the type of data you store and how vulnerable it is to attack. You should work with an insurance agent or broker who specializes in cyber liability insurance to make sure you are getting the right coverage for your business.

How much does cyber liability insurance cost?

The cost of cyber liability insurance varies depending on the size and type of business, the type of data and number of personal records the business holds, and the amount of coverage that is purchased. However, it is generally affordable for small businesses.

There are several factors that can affect the cost of cyber liability insurance cost. While some factors are within your control, others may be out of your hands. Here are four things that can impact your premiums:

- The size and type of business you run

- The number of employees you have

- Your history of data breaches or other cyber incidents

- Your use of technology

If you are thinking about getting cyber liability insurance, talk to your business insurance agent. They can help you understand the coverage and how much it would cost to insure your business.

How do cyberattacks happen?

Cyberattacks can happen in a number of ways, but the most common way is through phishing emails. Hackers will send out emails that look like they’re from a legitimate company, and they’ll ask for your personal information like your username and password. Sometimes they’ll even ask you to open an attachment or click on a link, and when you do, it will install malware on your computer.

Another way that cyberattacks can happen is through ransomware, which is also usually triggered through phishing emails. Ransomware is a type of malware that locks your computer or encrypts your files, and then demands a ransom be paid to unlock them.

Here are a few very costly examples of Ransomware attacks that have happened in recent years:

– WannaCry

On May 12, 2017, the WannaCry ransomware attack hit over 150 countries around the world. In total, it’s estimated that the WannaCry ransomware attack caused over $4 billion in damage.

– Petya

The Petya ransomware attack was a cyberattack that occurred on June 27, 2017. In total, it’s estimated that the Petya ransomware attack caused over $1 billion in damage.

– NotPetya

In June of 2017, a ransomware attack known as NotPetya hit businesses and governments around the world. In total, it’s estimated that the NotPetya ransomware attack caused over $10 billion in damage.

Lastly, hackers can also gain access to your computer or network by exploiting vulnerabilities in software or hardware. Once they’re in, they can steal sensitive data or even delete files.

What are some examples of data breaches and cyberattacks?

Small to mid-sized businesses tend to shy away from purchasing cyber liability insurance with the idea that cyber attacks only happen to big businesses. However, that couldn’t be further from the truth. With more and more businesses embracing digital practices, it is critical that nearly every business consider cyber liability insurance, especially because hackers often look at small businesses as easier targets than larger corporations.

As a small business you should discuss this type of protection with your insurance agent to determine which type and how much protection is necessary for your business. Here’s a look at some large corporations who have had large-scale data breaches. If these businesses are vulnerable to data breaches and cyber attacks—your small business is too.

– Target Corporation Data Breach

Target Corporation Data Breach was a cyberattack that occurred in late 2013, where hackers accessed the credit and debit card information of millions of Target customers. The attack exposed personal information such as names, addresses, phone numbers and email addresses, as well as encrypted credit card data. This was one of the largest data breaches in history, affecting up to 110 million people.

– The Home Depot Data Breach

In September 2014, Home Depot announced that they had suffered a data breach that affected 56 million customer payment cards. The hackers were able to gain access to the credit and debit card information of customers by installing malware on the self-checkout terminals in their stores. It is still unknown exactly how much damage was done.

– JPMorgan Chase Data Breach

JPMorgan Chase Data Breach was a cyberattack that occurred in late 2013, where hackers accessed the credit and debit card information of millions of JPMorgan Chase customers. The attack exposed personal information such as names, addresses, phone numbers and email addresses, as well as encrypted credit card data. This hack affected up to 110 million people.

– Sony Pictures Entertainment Hack

In November 2014, Sony Pictures Entertainment was hacked by a group calling themselves the “Guardians of Peace.” The hackers released the personal information of thousands of Sony employees, as well as confidential emails and documents from the company. They also threatened to release even more damaging information if Sony did not comply with their demands. This was a major breach of privacy, and it is still unknown who was behind the attack.

– Ashley Madison Hack

In August 2015, the dating website Ashley Madison was hacked by a group calling themselves the “Impact Team.” The hackers released the personal information of thousands of Ashley Madison employees, as well as confidential emails and documents from the company. It is still unknown who was behind the attack.

Does your business need cyber liability insurance?

Cyber liability insurance is an important tool for small businesses to protect themselves from the growing threat of cyberattacks. This type of policy can help cover the costs associated with a data breach or other type of cyberattack. If you’re interested in learning more about this coverage, please contact Torian Insurance. We would be happy to discuss your options and help you find the right policy for your business.